Medicare eligibility guidance can feel overwhelming when you’re approaching 65 or facing a major life change. The rules around who qualifies, what each part covers, and when to enroll matter more than most people realize.

At Dave Silver Insurance, we’ve helped countless people navigate these decisions and avoid costly mistakes. This guide walks you through the essentials so you can make informed choices about your coverage.

Who Qualifies for Medicare

Most people think Medicare starts at 65, and for the majority, that’s correct. But the actual rules are more flexible than you’d expect. You qualify for Medicare at 65 regardless of your work history, as long as you’re a U.S. citizen or permanent resident who has lived in the country for at least five consecutive years. However, age alone doesn’t determine your entire eligibility picture. The Social Security Administration and Centers for Medicare & Medicaid Services recognize three distinct pathways into Medicare before 65, and understanding which one applies to you changes everything about your timeline and enrollment strategy.

Three Pathways to Medicare Before 65

If you’ve been receiving Social Security Disability benefits for 24 months, you automatically qualify for Medicare Parts A and B without waiting until 65. This matters because many people don’t realize they qualify years earlier than expected. Two conditions skip this waiting period entirely: End-Stage Renal Disease (ESRD) and ALS. If you have permanent kidney failure that requires dialysis or a transplant, you can access Medicare within three months of starting dialysis or the month of your transplant. ALS eligibility begins the first month you qualify for disability benefits, with no waiting period at all. These aren’t theoretical distinctions-they determine whether you have coverage immediately or face months without insurance while waiting.

Disability and Extended Work Benefits

The 24-month waiting period for disability-based Medicare eligibility applies only to Social Security or Railroad Retirement Board disability beneficiaries. Once you hit that mark, you’re automatically enrolled in both Part A and Part B unless you actively decline Part B. The practical implication is significant: if you work while disabled and earn above the substantial gainful activity limit, you may lose your cash disability benefit but retain Medicare coverage during your Extended Period of Eligibility, which lasts up to 93 months after your Trial Work Period ends. This structure allows working-age people with disabilities to maintain health insurance even when their disability benefits pause.

ESRD and ALS beneficiaries face a completely different timeline. ESRD eligibility requires either regular dialysis or a functioning kidney transplant, and your Part A coverage begins three months after dialysis starts or during the month of transplant. ALS has the most favorable rules: you need only be entitled to disability benefits in your first month of eligibility, with coverage starting immediately. The distinction matters because delaying dialysis awareness or waiting to apply for disability could cost you months of uninsured medical expenses.

Residency and Citizenship Requirements

U.S. citizenship or lawful permanent residency is non-negotiable for Medicare eligibility at any age. Permanent residents must have lived continuously in the United States for at least five years. If you’re a permanent resident who hasn’t met this requirement, you won’t qualify at 65. If you live outside the United States, you can still maintain Medicare Parts A and B, but coverage for services outside U.S. territories is extremely limited. Most beneficiaries abroad find Medicare nearly worthless for routine care.

Puerto Rico residents follow different rules: they’re automatically enrolled in Part A but must actively enroll in Part B, unlike residents of the 50 states who are typically enrolled in both unless they decline. These aren’t edge cases-thousands of beneficiaries face coverage gaps annually because they misunderstood residency rules or didn’t complete required enrollment steps for their specific situation. Understanding where you live and what that means for your enrollment determines whether you have seamless coverage or unexpected gaps when you need care most.

What Each Medicare Part Actually Covers

Medicare’s four-part structure exists for a reason: hospital stays, doctor visits, and prescription drugs require different types of coverage. Understanding what Part A and Part B pay for prevents you from discovering coverage gaps when you’re already in the hospital or at the pharmacy.

Part A and Part B: The Foundation

Part A covers inpatient hospital stays, skilled nursing facility care after hospitalization, home health services, and hospice care. Most people pay nothing for Part A premiums if they worked and paid Medicare taxes for at least 10 years, according to the U.S. Department of Health and Human Services. Part B covers physician services, outpatient hospital care, diagnostic tests, and preventive services. Unlike Part A, Part B always requires a monthly premium even if you never use the services. The 2026 Part B standard premium is approximately $177.90 monthly, though your actual cost depends on your income level. Higher earners pay surcharges that can nearly double this amount. The Centers for Medicare & Medicaid Services adjusts both premiums annually, so what you pay this year will likely change next year.

The Real Cost of Original Medicare

The real problem emerges when people confuse what Parts A and B cover with what they actually cost. Part A has a $1,736 deductible per hospital stay in 2026, meaning you pay this amount before Part A coverage kicks in. After that, you’re responsible for copayments ranging from $419 to $838 daily depending on the length of your stay. Part B requires you to pay 20 percent of most services after meeting a $240 annual deductible. These out-of-pocket costs devastate unprepared retirees.

Medicare Advantage: Network Restrictions for Cost Control

Medicare Advantage plans, also called Part C, bundle Parts A, B, and D into a single private insurance policy with monthly premiums that vary by plan and can change annually. These plans appeal to people who want predictable costs and don’t mind using network doctors. Medicare Advantage plans typically cap your annual out-of-pocket spending, meaning once you hit that limit, the plan covers remaining eligible services. The tradeoff is restricted provider networks and prior authorization requirements for many services.

Medigap: Flexibility with Higher Premiums

Medigap policies work differently: they’re supplemental insurance sold by private carriers that pay your deductibles, copayments, and coinsurance on Original Medicare. If you choose Original Medicare plus Medigap, you’ll have broader provider choice and no prior authorizations, but you’ll manage two separate insurance policies and pay premiums for both Part B and your Medigap plan. Plan F, the most comprehensive Medigap option, covers virtually all out-of-pocket costs under Original Medicare, though it costs significantly more than basic plans.

Making Your Choice

The fundamental choice boils down to network flexibility versus cost predictability. Medicare Advantage restricts your doctors but caps expenses. Original Medicare with Medigap gives you provider freedom but requires higher premiums to cover the supplemental policy. Your decision here shapes not only your monthly costs but also which doctors you can see and how much you’ll pay when you need care. The next section examines the mistakes that lead people to choose the wrong path.

Common Mistakes People Make When Enrolling in Medicare

Late Enrollment Penalties That Last Forever

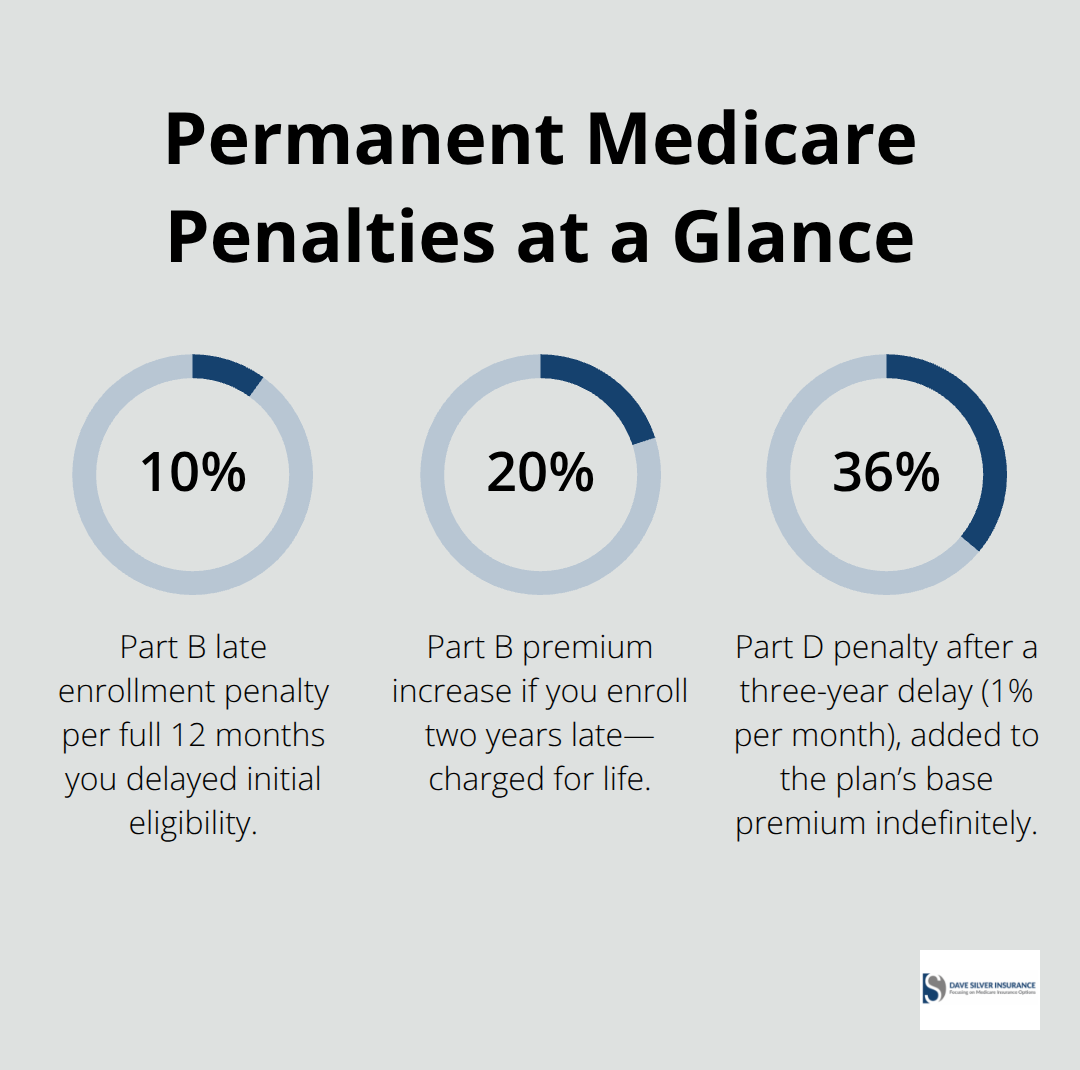

Late enrollment penalties haunt beneficiaries for life. The Social Security Administration and Centers for Medicare & Medicaid Services impose a permanent 10 percent surcharge on your Part B premium for each full 12-month period you could have enrolled but didn’t. If you miss your Initial Enrollment Period by two years, you’ll pay 20 percent more than the standard premium forever. A person who delays Part B enrollment at 65 and enrolls at 67 will pay approximately $35.58 extra monthly for the rest of their life on a standard 2026 premium of $177.90.

That adds up to roughly $4,270 in unnecessary costs over a decade.

The enrollment window is ruthlessly short: seven months centered on your 65th birthday (three months before and three months after). Miss it without qualifying for a Special Enrollment Period, and you’ve locked in permanent financial damage. Disability beneficiaries face identical penalties if they fail to enroll in Part B during their initial eligibility window.

The only escape routes are narrow. You must have had employer group health coverage that continued past 65, or qualify for one of the exceptional circumstances like TRICARE eligibility, incarceration release, or Medicaid termination. These exceptions exist, but beneficiaries rarely realize they apply until after they’ve already incurred penalties.

Part D drug coverage carries the same permanent penalty structure. Missing enrollment when first eligible costs you 1 percent of the national average plan premium for each month of delay. Someone who waits three years pays 36 percent more monthly for prescription coverage indefinitely. The Centers for Medicare & Medicaid Services calculates this penalty at approximately $13.20 monthly in 2026 for a standard three-year delay, compounding annually as the national average premium increases.

Skipping Annual Plan Comparisons

Comparing plans before enrollment separates smart beneficiaries from those who accept whatever default option appears on their screen. Medicare Advantage premiums and out-of-pocket maximums change annually, sometimes dramatically. A plan that cost $89 monthly with a $5,000 out-of-pocket maximum this year might jump to $145 monthly with a $7,500 maximum next year. The Centers for Medicare & Medicaid Services reports that beneficiaries who fail to review annual plan changes leave thousands in potential savings untouched.

Your current plan may no longer include your doctor’s office or your preferred pharmacy. Networks shrink, drug formularies shift, and prior authorization requirements expand. Beneficiaries who assume their plan remains constant waste hours fighting denials and switching plans mid-year when they discover their specialist dropped from the network.

Medigap policies deserve identical scrutiny. Plan F costs vary by hundreds of dollars monthly depending on the insurance carrier, even though all Plan F policies cover identical benefits. A 65-year-old paying $250 monthly for Plan F could find identical coverage for $165 elsewhere. Original Medicare beneficiaries who skip this comparison pay roughly $1,020 annually in excess premiums.

Part D drug plans require annual review because formularies change constantly. Your blood pressure medication might shift from Tier 1 to Tier 3, tripling your copayment overnight. A drug that cost $15 monthly could suddenly require prior authorization or jump to $65. Spending 30 minutes annually comparing three options typically saves $500 to $1,500 yearly across all four parts of Medicare combined.

Neglecting Supplemental and Drug Coverage

Overlooking Medigap and Part D coverage creates the most dangerous gaps. Many Original Medicare beneficiaries skip Medigap, thinking they’ll manage Part B’s 20 percent coinsurance themselves. A single hospitalization with complications can generate $15,000 to $40,000 in Part A copayments and deductibles that Medigap would cover completely. A serious diagnosis requiring chemotherapy or specialized drugs can cost $8,000 to $20,000 annually in Part D copayments without supplemental coverage.

Beneficiaries without Part D coverage face an impossible choice: pay full pharmacy prices or skip doses. Part D enrollment deadlines run parallel to Part A and B deadlines, yet many people enroll in Original Medicare and forget about prescription coverage entirely. The permanent penalty applies identically-miss the deadline, and you’ll pay surcharges forever. Someone with chronic conditions requiring five medications faces potentially $3,000 to $8,000 annually in preventable drug costs from this single oversight.

Final Thoughts

Medicare eligibility guidance shapes your financial reality for decades, which is why your enrollment decisions matter far more than most people realize. Your path into Medicare depends on age, disability status, ESRD, or ALS-not on your work history or income level. Missing your Initial Enrollment Period by even one month triggers permanent penalties that follow you forever, and skipping annual plan comparisons costs you thousands in preventable overpayments.

Determining which Medicare path applies to your situation changes everything about your timeline and strategy. Are you approaching 65 with employer coverage that extends past your birthday? Do you have a disability that qualifies you for early Medicare? Your answer determines whether you enroll now or wait, and whether you face penalties or avoid them entirely. Generic guidance won’t account for your unique circumstances, which is why personalized review prevents costly mistakes.

We at Dave Silver Insurance simplify this complexity with expertise that guides people through Medicare enrollment decisions. Contact Dave Silver Insurance to review your health needs, financial situation, and coverage preferences so you can move forward with confidence in your healthcare decisions.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation