Medicare covers a lot, but it doesn’t cover everything. That’s where Medigap comes in-it fills the gaps that Original Medicare leaves behind, like copayments, coinsurance, and deductibles.

We at Dave Silver Insurance created this Medigap coverage guide to help you understand your options and pick the right plan for your situation. The right supplement can save you thousands of dollars each year.

What Medigap Actually Covers

The Real Costs Medicare Leaves Behind

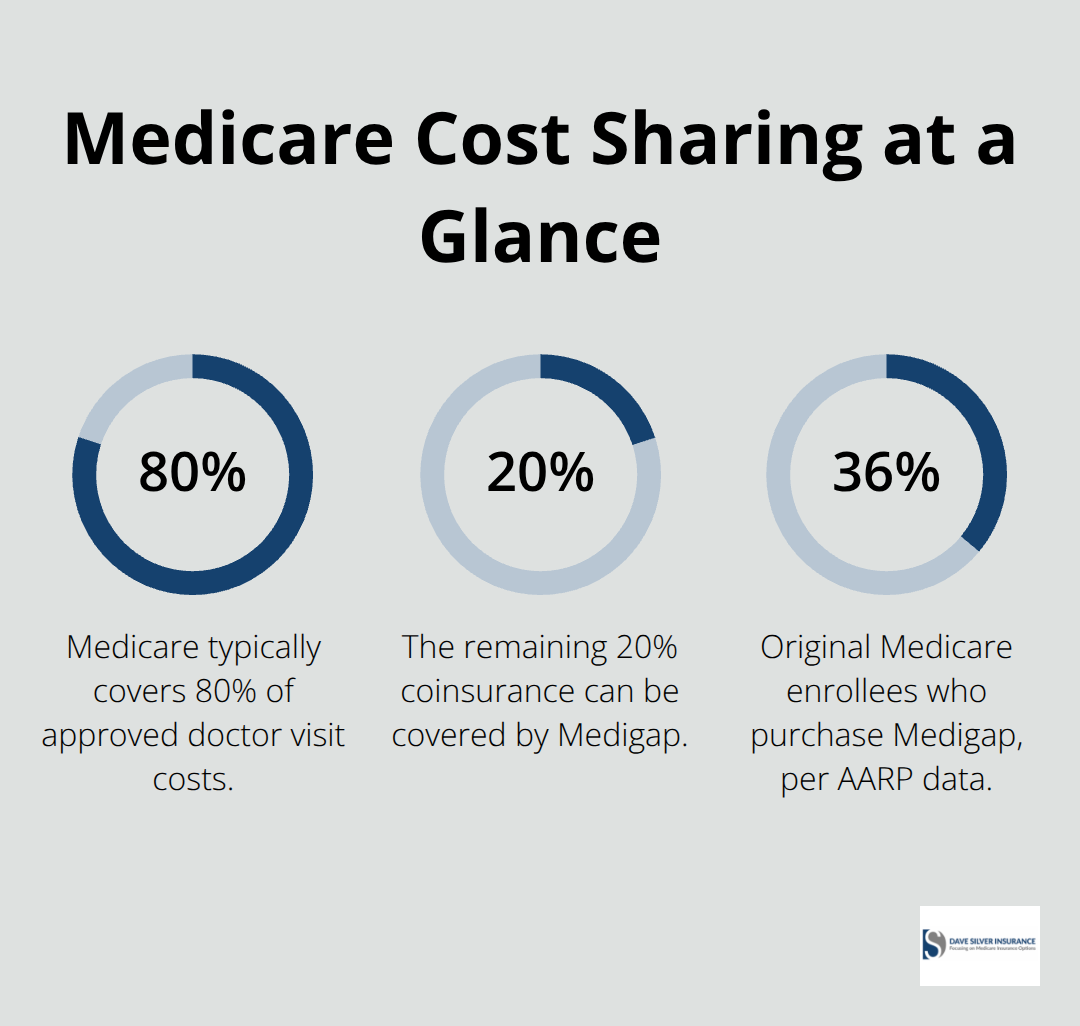

Medigap is a private insurance policy that pays for costs Original Medicare leaves behind. When Medicare covers 80% of your doctor visit, Medigap picks up that remaining 20% coinsurance. When you hit a deductible, Medigap covers it. These aren’t theoretical gaps-they’re real expenses that add up fast.

In 2026, the Part B deductible alone is $283, and hospital stays carry a $1,600 deductible per admission. About 36% of Original Medicare enrollees purchase Medigap coverage, according to AARP data, because the math is straightforward: without it, you pay those gaps yourself. The policy works only with Original Medicare Parts A and B, not with Medicare Advantage, and you need both parts before any insurer will sell you a Medigap plan. You pay a monthly premium to a private insurer in addition to your standard Part B premium of $202.90, but that investment typically saves thousands in out-of-pocket costs annually, especially if you see doctors regularly or face unexpected hospitalizations.

How the 10 Standardized Plans Differ

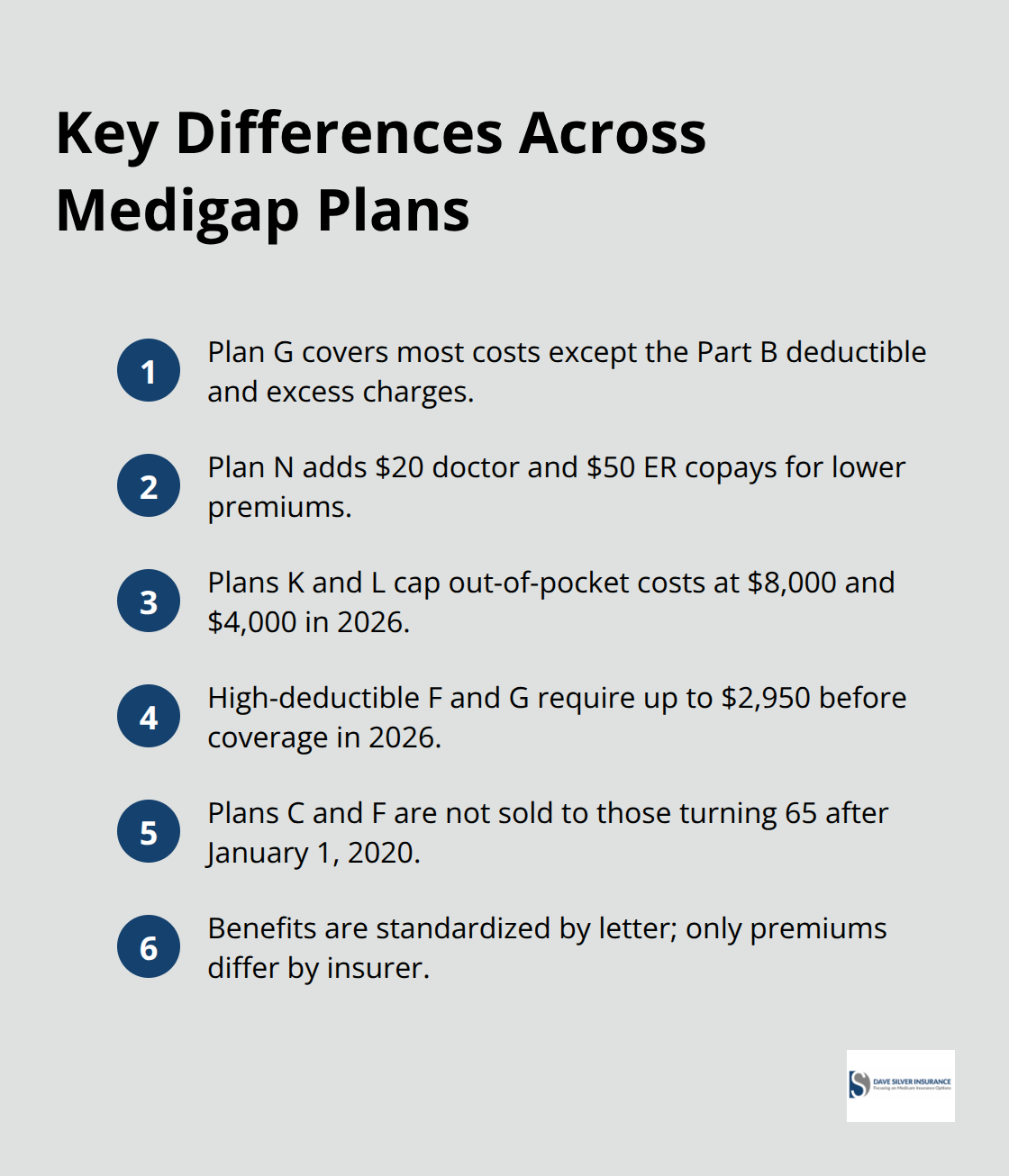

Ten federally approved plans exist-A, B, D, G, K, L, M, and N-and the coverage is standardized by letter across all insurers nationwide. Plan G stands out as the strongest value right now because it covers most Medicare cost-sharing except the Part B deductible and excess charges. Plan N offers lower premiums with $20 copays for doctor visits and a $50 emergency room copay, making it practical for people who want predictable costs. Plans K and L cap your annual out-of-pocket expenses at $8,000 and $4,000 respectively in 2026, meaning once you hit that limit, the plan pays 100% of covered costs for the rest of the year-useful if you want lower premiums but can handle hitting a ceiling. High-deductible versions of Plan F and G exist in some states, requiring you to pay up to $2,950 in 2026 before coverage kicks in, which only makes sense if you rarely use healthcare services.

Plans C and F are no longer sold to people who turned 65 after January 1, 2020, though existing policyholders can keep them. The standardization means you can switch between insurers offering the same plan letter without losing benefits-only your premium changes.

Cost Predictability With Medigap Versus Medicare Advantage

Medicare Advantage plans bundle coverage into one policy and often charge lower or zero premiums, but they use networks, require referrals, and include copays that vary by service. Medigap works differently: once you pay your premium, you know exactly what you’ll owe at the doctor because the plan letter defines your coverage nationwide. Medicare Advantage carriers can change networks and increase copays yearly, leaving you scrambling to adjust. With Medigap, you can switch to a different Medigap policy. When you get your new Medigap policy, you have 30 days to decide if you want to keep it. If you manage chronic conditions like diabetes or heart disease, the certainty of Medigap coverage matters far more than chasing low premiums on an Advantage plan that might restrict your doctors next year. You cannot hold both Medigap and Medicare Advantage simultaneously, so the choice is real and permanent until you switch back to Original Medicare. Understanding which plan fits your health needs and budget sets the stage for the next critical decision: timing your enrollment correctly.

Which Medigap Plan Matches Your Health and Budget

Plan G: The Market Leader

Plan G dominates the market for good reason. It covers Part A coinsurance, Part B coinsurance, Part B excess charges, skilled nursing facility coinsurance, and foreign travel emergencies. You remain responsible only for the Part B deductible of $283 in 2026 and any excess charges your doctor charges beyond Medicare’s approved amount. Most people with chronic conditions or regular specialist visits find Plan G delivers the coverage certainty they need.

Plan N: Lower Premiums With Predictable Copays

Plan N costs less monthly but introduces copays: $20 per doctor visit and $50 for emergency room visits. This sounds manageable until you see a specialist three times monthly and suddenly owe $240 in copays alone. Plan N works best for people who visit doctors infrequently or want to trade lower premiums for modest out-of-pocket costs per visit.

Plans K and L: Capped Out-of-Pocket Costs

Plans K and L appeal to people confident they won’t need much care. Plan K caps your annual out-of-pocket costs at $8,000 in 2026, and Plan L caps them at $4,000. You shoulder 50% or 75% of costs until hitting those limits, meaning a $1,600 hospital admission deductible might cost you $800 out-of-pocket first. These plans work for younger, healthier enrollees willing to accept higher initial costs for lower premiums.

High-Deductible and Minimal Coverage Options

High-deductible Plan F and G require you to pay $2,950 in 2026 before any coverage kicks in, making sense only if you’re healthy and want the lowest premium. Plan A and B offer minimal coverage and don’t cover the Part A hospital deductible, which runs $1,600 per admission in 2026-a single hospitalization wipes out any monthly premium savings. For anyone managing chronic illness like diabetes or requiring regular specialist care, Plans D, G, or N deliver predictability. For healthy people under 70 with no regular medications or doctor visits, Plan K or high-deductible G might work, but the moment a health crisis hits, you’ll wish you’d chosen broader coverage.

Making Your Selection: The Math That Matters

Premium prices for identical plan letters vary wildly by insurer and location-two companies selling Plan G in the same state might charge $150 and $220 monthly, so comparing quotes across at least three insurers before enrolling saves hundreds annually. State Health Insurance Assistance Program counselors at shiphelp.org provide free, unbiased plan comparisons tailored to your specific medications and doctors, and they’re especially accessible from October through December when most people enroll.

Your choice hinges on two practical calculations: add up your expected annual doctor visits, specialist appointments, and hospital days, then multiply by the copays or coinsurance each plan charges, and compare that total to the monthly premium difference. If Plan G costs $50 more monthly than Plan N but saves you $600 annually in coinsurance and copays, the math favors Plan G. If you take five medications monthly and no doctor visits, Plan N’s lower premium outweighs the copay risk.

Switching plans after enrollment remains possible, but only during specific windows. If you joined a Medicare Advantage plan first and want Medigap later, you have a 12-month trial period to switch back to Original Medicare and buy Medigap without health-based denial. Once enrolled in Medigap, automatic renewal happens yearly as long as you pay premiums, giving you stability that Medicare Advantage networks cannot match. The real mistake people make is selecting based on monthly premium alone and ignoring what they’ll actually owe when they need care; a $40 monthly savings on premium evaporates the moment you face a $2,000 hospital stay that a better plan would have covered. With your plan selection made, the next critical step involves understanding when you can actually enroll and what protections the law provides during that window.

Enrollment Rules and Timing for Medigap Coverage

Your Golden Six-Month Window

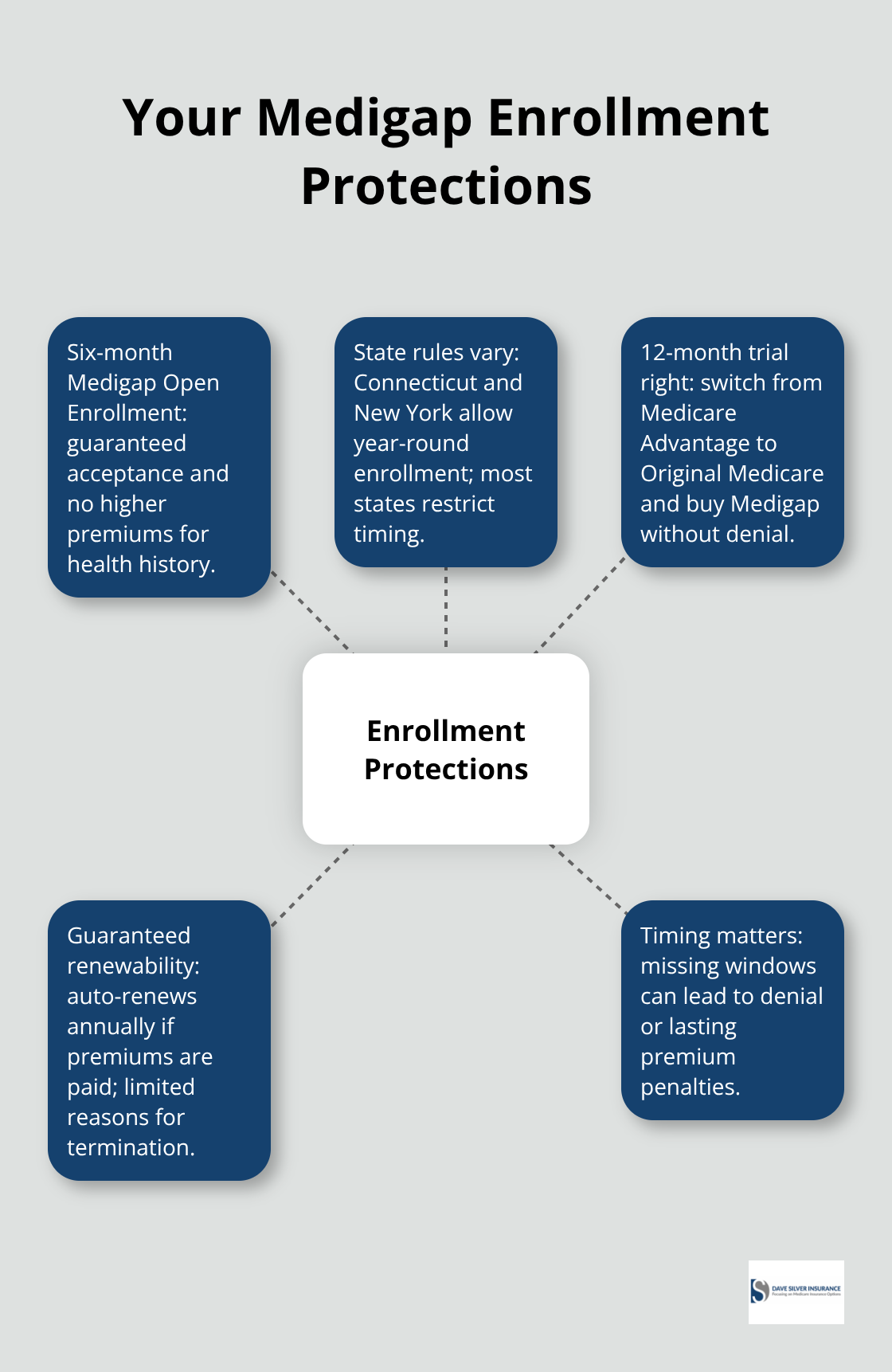

The six-month window after you first enroll in Medicare Part B is your golden opportunity, and this timing matters more than most people realize. During this Medigap Open Enrollment Period, insurers must sell you any plan available in your state regardless of your health history, and they cannot charge higher premiums because of preexisting conditions. Miss this window and the rules change dramatically. Outside the enrollment period, some states like Connecticut and New York allow you to buy Medigap anytime without denial, but most states impose strict limits on when you can enroll or switch plans. If you wait six months after turning 65 and enrolling in Part B, you may face denial or premium penalties that persist for years.

State Rules That Determine Your Access

The specific deadlines depend on your state, which is why you should check your State Health Insurance Assistance Program guidelines at shiphelp.org within 30 days of Part B enrollment. Federal law guarantees your right to enroll during the open period, but state rules vary on what happens afterward, making early action essential rather than optional. Connecticut and New York stand out as exceptions that allow enrollment outside standard windows, but most other states enforce strict deadlines that can lock you out of coverage or force you to accept higher premiums.

The 12-Month Trial Period for Medicare Advantage Switchers

If you switched from Medicare Advantage to Original Medicare, federal law gives you a second chance through the 12-month trial period. This means if you joined a Medicare Advantage plan at age 65, then decided within the first year that you want Medigap instead, you can disenroll from the Advantage plan and buy Medigap without health-based denial or waiting periods. This protection exists specifically because Medicare Advantage networks change yearly and copays increase, trapping people who discover too late that their doctors left the plan. Once you enroll in Medigap outside the initial six-month window and without the trial period protection, insurers can deny you for preexisting conditions or charge substantially higher premiums depending on your state’s rules.

Automatic Renewal and Long-Term Stability

The automatic renewal clause protects you going forward: once you hold a Medigap policy, it renews automatically each year as long as you pay premiums on time, meaning your coverage remains stable even if your health declines. Insurers can only drop you for nonpayment, misrepresentation on your application, or bankruptcy, not because you filed claims or your health worsened. This stability contrasts sharply with Medicare Advantage, where networks shrink and benefits shift annually, forcing annual reevaluation.

Understanding these enrollment windows and protections transforms Medigap from a confusing bureaucratic maze into a straightforward process where timing and state rules determine your access and costs.

Final Thoughts

Medigap fills the gaps that Original Medicare leaves behind, and selecting the right plan transforms your healthcare costs from unpredictable to manageable. The math is straightforward-compare what you’ll actually pay across premiums, deductibles, and copays rather than fixating on monthly premium alone, because a $40 monthly savings evaporates the moment you face a $1,600 hospital deductible that a better plan would have covered. Plan G delivers comprehensive coverage for people managing chronic conditions, Plan N provides lower premiums with modest copays, and Plans K and L cap your annual out-of-pocket expenses for budget-conscious enrollees.

Your enrollment timing determines everything. The six-month window after you first enroll in Medicare Part B is your golden opportunity to buy any plan without health-based denial or premium penalties. If you switched from Medicare Advantage to Original Medicare within the first year, federal law gives you a 12-month trial period to buy Medigap without restrictions, and once enrolled, automatic renewal protects you going forward as long as you pay premiums.

We at Dave Silver Insurance help people navigate these decisions with personalized guidance tailored to your specific health needs and budget. Schedule a consultation with us to receive individualized recommendations backed by expertise and compliance with Medicare regulations, and our team answers your questions about Medigap coverage guide options, enrollment deadlines, and plan selection seven days a week.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation