Medicare late enrollment penalties can cost you hundreds of dollars annually if you miss key deadlines. These financial consequences affect millions of Americans who delay signing up for Medicare coverage.

We at Dave Silver Insurance see clients facing these penalties regularly, but most are completely avoidable with proper planning. Understanding Medicare late enrollment penalty exceptions can save you significant money and stress.

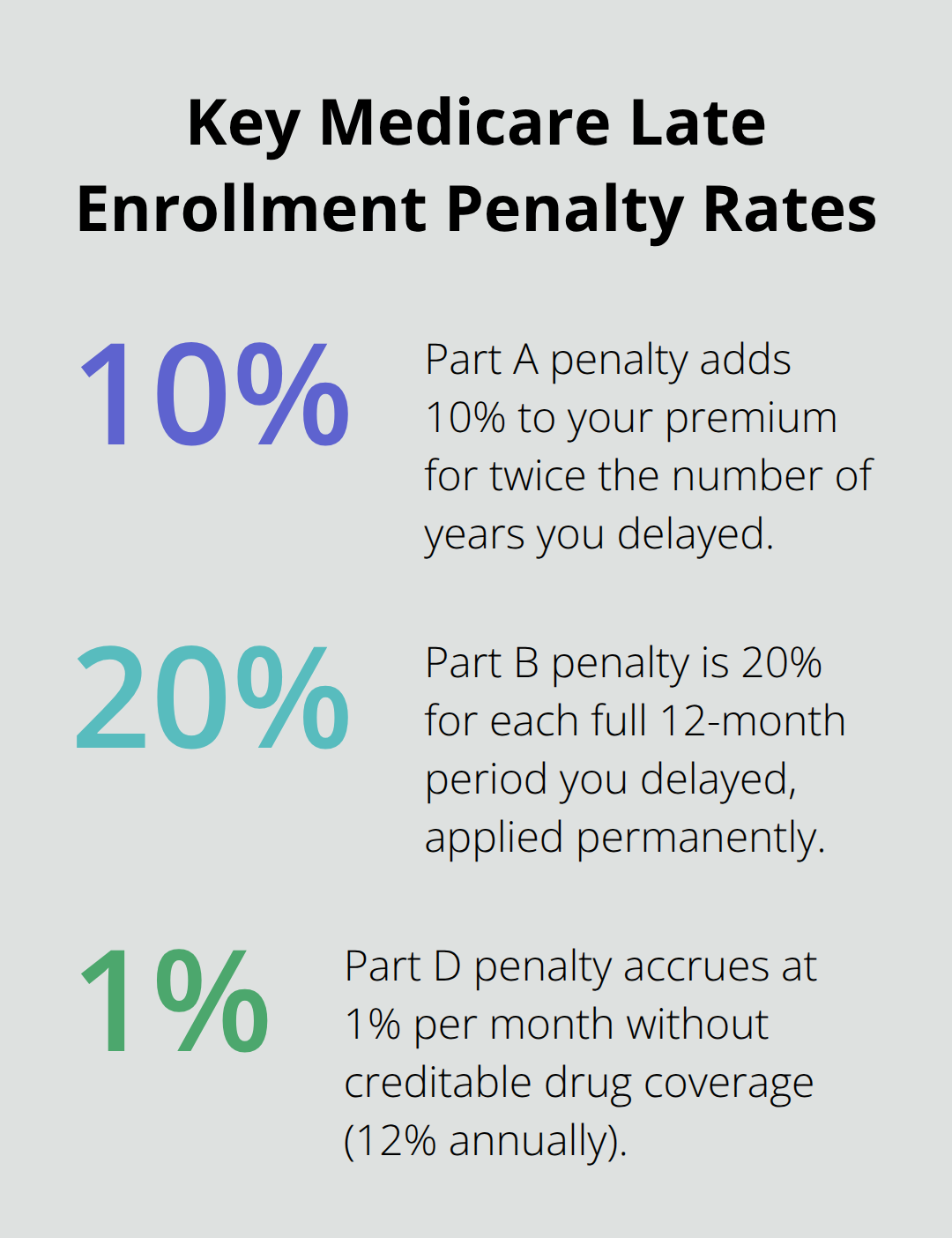

What Are Medicare Late Enrollment Penalties?

Medicare late enrollment penalties represent permanent monthly premium increases that activate when you enroll after your deadline passes. The Part A penalty adds 10% to your premium for twice the number of years you delayed enrollment, which means a two-year delay results in a 40% increase that lasts four years. Most people qualify for premium-free Part A, but those who don’t face this steep financial consequence. The Part B penalty operates at 20% for each full 12-month period that you could have signed up, applied permanently to your monthly premium.

Part B Penalty Calculations Create Lasting Impact

The 2025 standard Part B premium costs $185 monthly, but a single year of delayed enrollment pushes this to $222 monthly. Wait two years and your premium jumps to $259 monthly for life. The 2026 premium increases to approximately $202.90, which means a 20% penalty from one year of delay costs you $243.50 monthly.

These calculations apply regardless of income, though high earners face additional surcharges on top of penalties (making the total cost even higher for wealthy beneficiaries).

Part D Drug Coverage Penalties Accumulate Monthly

Part D penalties build at 1% of the national base beneficiary premium for each month without creditable drug coverage, which reaches 12% annually. The 2025 national base premium of $36.78 means each month of delay costs an additional 37 cents monthly forever. A 14-month gap results in a 14% penalty, which adds $5.15 to your monthly premium permanently. The 2026 base premium increases to $38.99 (making delays even more expensive). Unlike other Medicare penalties, Part D penalties follow you across all prescription drug plans for life.

How Penalties Stack Against Your Budget

These penalties compound your Medicare costs significantly over time. A beneficiary who delays Part B enrollment for one year pays an extra $37 monthly in 2025, totaling $444 annually in additional costs. Part D penalties may seem smaller initially, but they accumulate across decades of coverage. The combination of both penalties can easily add $100 or more to monthly healthcare expenses, which creates substantial financial strain during retirement years when income typically decreases.

Several exceptions exist that can help you avoid these costly penalties entirely.

Which Exceptions Actually Protect You From Penalties?

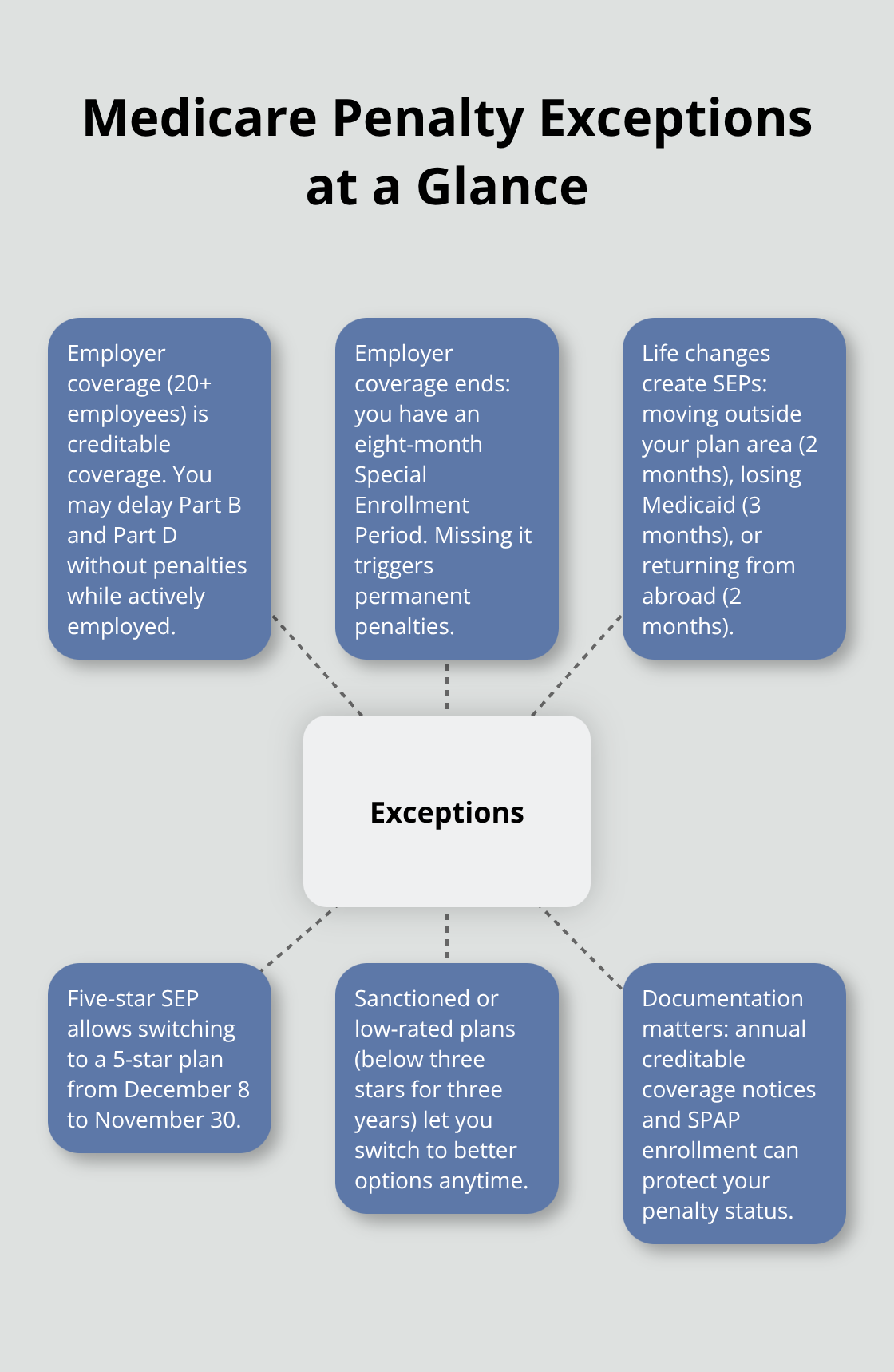

Employer Coverage Creates Your Safety Net

Working past 65 with employer health insurance from companies with 20 or more employees protects you completely from Medicare penalties. The Centers for Medicare & Medicaid Services recognizes this as creditable coverage, which means your employer plan meets Medicare standards for prescription drugs and medical benefits. You can delay Part B and Part D enrollment without financial consequences as long as your employment continues.

However, the moment your employer coverage ends, you have exactly eight months to enroll in Medicare through a Special Enrollment Period. Medicare enforces this eight-month window rigorously, and missing it triggers the same permanent penalties we discussed earlier. Document your employer coverage dates meticulously because Medicare requires proof of continuous creditable coverage when you eventually enroll.

Life Changes Open Penalty-Free Enrollment Windows

Moving outside your current Medicare plan’s service area gives you two months to switch plans or return to Original Medicare without penalties. Losing Medicaid eligibility provides a three-month window to change your Medicare coverage. Returning to the United States after living abroad opens a two-month enrollment period.

These Special Enrollment Periods have strict deadlines that Medicare enforces rigorously. Involuntary loss of coverage (such as when your employer drops health benefits) creates a two-month window to join Medicare plans. Many beneficiaries miss these opportunities because they assume Medicare enrollment follows calendar year patterns, but Special Enrollment Periods operate independently of annual open enrollment.

Medicare Plan Quality Ratings Affect Access

Five-star rated Medicare plans accept new enrollments between December 8 and November 30 through the 5-star Special Enrollment Period. This exception provides flexibility for beneficiaries who seek top-tier coverage outside normal enrollment windows. Special Needs Plans for individuals with chronic conditions allow enrollment changes throughout the year, though exiting these plans requires meeting specific conditions.

Medicare sanctions against poorly performing plans also trigger enrollment opportunities. Beneficiaries in plans rated below three stars for three consecutive years can switch anytime to better-performing options (which gives them escape routes from substandard coverage).

Documentation Requirements Protect Your Rights

The Medicare Modernization Act mandates that prescription drug plans notify beneficiaries about creditable coverage status annually before October 15. This helps you track whether your current coverage protects against future penalties. Integrated Dual Eligible Special Needs Plans coordinate Medicare and Medicaid benefits for qualifying individuals who meet specific income and health criteria.

State Pharmaceutical Assistance Program enrollment allows beneficiaries to join a Medicare drug plan within a year of enrollment. Understanding these documentation requirements becomes essential when you need to prove your penalty exemption status to Medicare administrators.

How Do You Prevent Medicare Penalties

Mark Your Calendar Three Months Before Your 65th Birthday

Your Initial Enrollment Period starts three months before your 65th birthday and ends three months after. Medicare.gov confirms this seven-month window represents your only chance to enroll without penalties unless you qualify for specific exceptions. Write these dates on your calendar immediately and set multiple reminders. The Social Security Administration automatically enrolls you in Part A if you receive Social Security benefits, but Part B and Part D require active enrollment decisions.

Medicare operates on strict deadlines that leave no room for confusion. Your birthday month determines everything: if you turn 65 on the 15th or later, your coverage starts the following month. Turn 65 before the 15th and coverage begins on your birthday month. Miss the final deadline by even one day and permanent penalties follow you for decades.

Collect Documentation From Every Health Plan

Request written confirmation of creditable coverage from all prescription drug plans, employer health insurance, and Medicare Advantage plans you maintain. The Centers for Medicare & Medicaid Services requires this documentation when you enroll to verify penalty exemptions. Save every annual creditable coverage notice your employer sends before October 15 each year (these letters become your proof against future penalties).

Employer HR departments must provide creditable coverage certificates within 30 days of your request according to Medicare regulations. Veterans Affairs benefits, TRICARE coverage, and state pharmaceutical assistance programs also qualify as creditable coverage when properly documented. Create a file with all coverage dates, policy numbers, and official letters because Medicare administrators scrutinize every gap when they calculate penalties.

Submit Applications During the First Month of Eligibility

Submit enrollment applications during your first eligible month to prevent any coverage gaps that trigger penalties. Medicare processes applications in 30 to 60 days, which means last-minute applications risk creating dangerous gaps in coverage. The Medicare.gov website processes applications faster than paper forms, but both methods require complete information to avoid delays that could result in penalty assessments. If you qualify for Special Enrollment Periods, your coverage will start the first day of the month after the plan gets your request to join.

Final Thoughts

Medicare late enrollment penalty exceptions protect millions of Americans from costly premium increases, but only when you understand and act on them properly. Track your Initial Enrollment Period dates, maintain creditable coverage documentation, and submit applications during your first eligible month. These three actions prevent the permanent financial consequences that follow missed deadlines.

Professional Medicare guidance becomes invaluable when you navigate complex enrollment rules and penalty exceptions. We at Dave Silver Insurance help clients avoid these costly mistakes through personalized recommendations based on individual health and financial needs. Our expertise covers Medicare Parts A, B, C, and D, plus Medigap Insurance options that reduce out-of-pocket expenses.

Start your Medicare planning three months before your 65th birthday or immediately if you face upcoming coverage changes. Schedule a consultation with Dave Silver Insurance to receive tailored advice that keeps you compliant with Medicare regulations while you maximize your benefits (our accessibility means you get expert guidance when you need it most). This prevents penalty mistakes that cost hundreds of dollars monthly for decades.