Veterans often juggle two separate healthcare systems, and most don’t realize how much money they’re leaving on the table. Medicare for veterans benefits works differently than standard Medicare, and the coordination rules are confusing enough that many eligible veterans miss out on significant savings.

At Dave Silver Insurance, we’ve seen firsthand how the right strategy can cut your out-of-pocket costs in half. This guide walks you through the real decisions that matter.

When Should You Enroll in Medicare as a Veteran

Enrollment Timing Determines Your Long-Term Costs

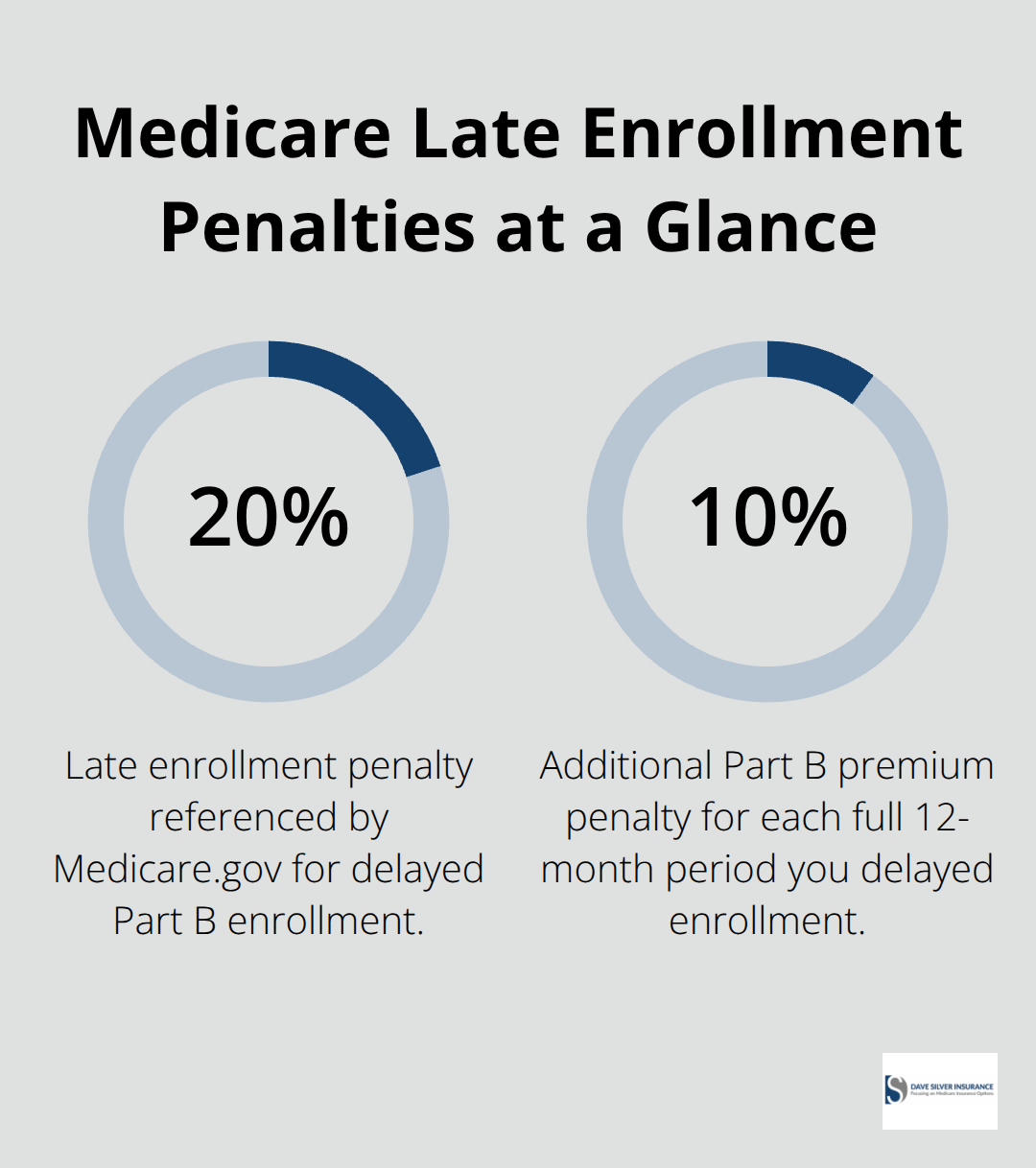

Veterans become eligible for Medicare at age 65, just like everyone else, though some qualify earlier due to specific disabilities such as end-stage renal disease or ALS. The timing of your enrollment matters far more than most veterans realize because missing your Initial Enrollment Period without creditable coverage triggers permanent penalties that compound every year. Your Initial Enrollment Period spans about seven months centered on your 65th birthday-three months before, the month you turn 65, and three months after. If you miss this window and don’t have creditable employer coverage or VA prescription drug coverage that counts as creditable, you’ll pay a 10% penalty on your Part B premium for every 12 months you delayed, a cost that sticks with you for life. The General Enrollment Period runs January 1 through March 31 each year, with coverage starting July 1, but this option still carries those permanent penalties. You should enroll during your Initial Enrollment Period even if you plan to rely primarily on VA care, because Medicare gives you access to non-VA providers when VA wait times are long or when you need specialists outside the VA network.

Using Both Systems Simultaneously Maximizes Your Coverage

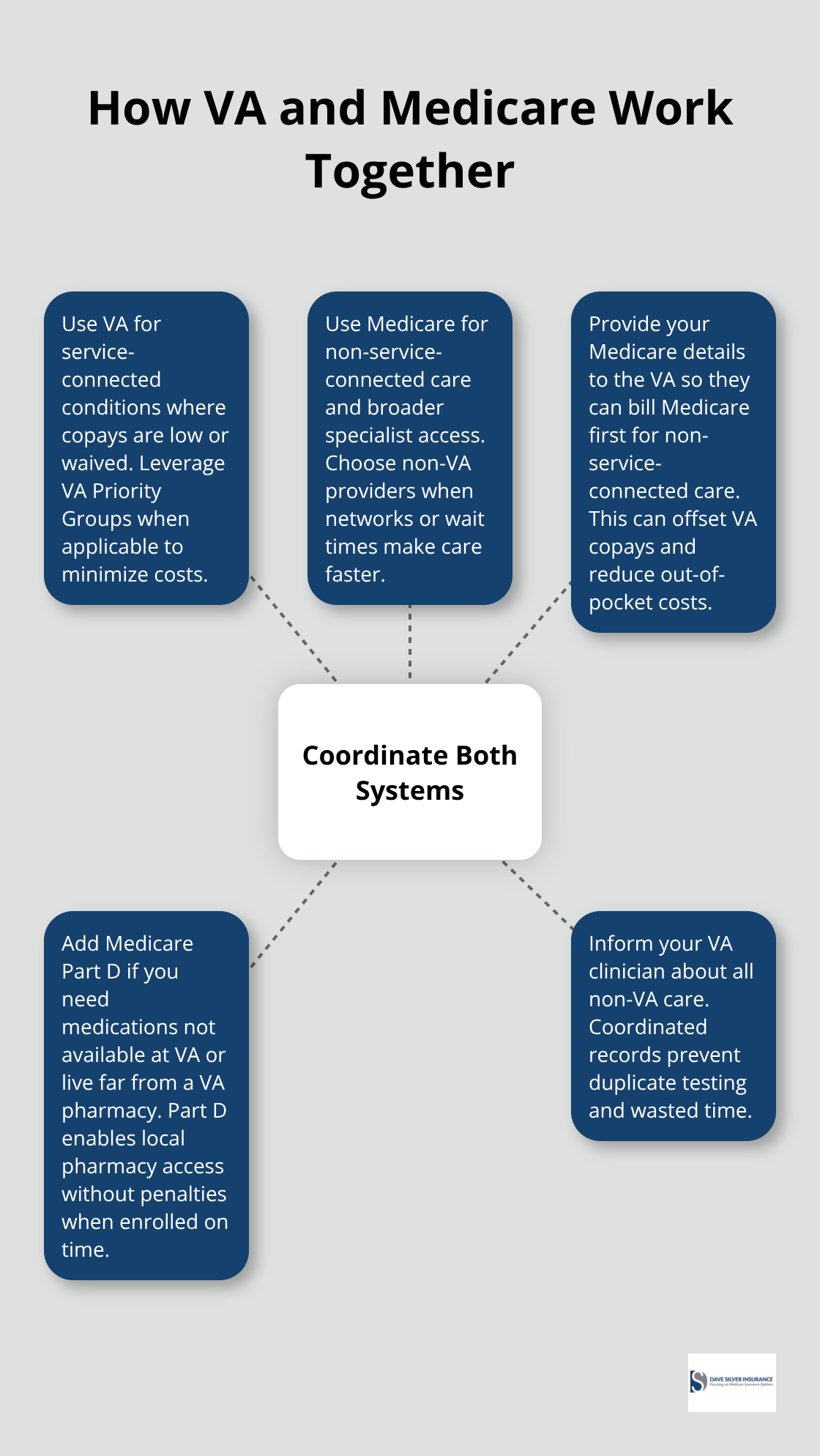

Most veterans incorrectly assume they must choose between VA benefits and Medicare, but federal policy allows you to use both simultaneously and coordinate them for maximum coverage. When you have both systems active, you select which benefits to use at each visit-you might use VA for service-connected conditions where copays are low or free, then use Medicare for non-service-connected care or when a non-VA specialist is more accessible. VA can bill your private insurance for non-service-connected care, which means providing your Medicare information to the VA can offset copays when Medicare pays first.

If you have a 100% VA disability rating, you fall into VA Priority Group 1, which covers most inpatient and outpatient services with minimal cost, yet Medicare still fills critical gaps for dental, vision, and prescription drugs that VA coverage limits by priority group. For prescription medications specifically, VA drug coverage has no premiums and no or limited copayments, but if you need medications unavailable at VA facilities or live far from a VA pharmacy, Medicare Part D lets you use local pharmacies without penalties as long as you enrolled when first eligible or within 63 days of losing creditable VA coverage. Inform your VA clinician whenever you receive care outside the system so they can coordinate your care and prevent duplicative testing that wastes money and time.

Verify Your Actual Eligibility Status Before Making Decisions

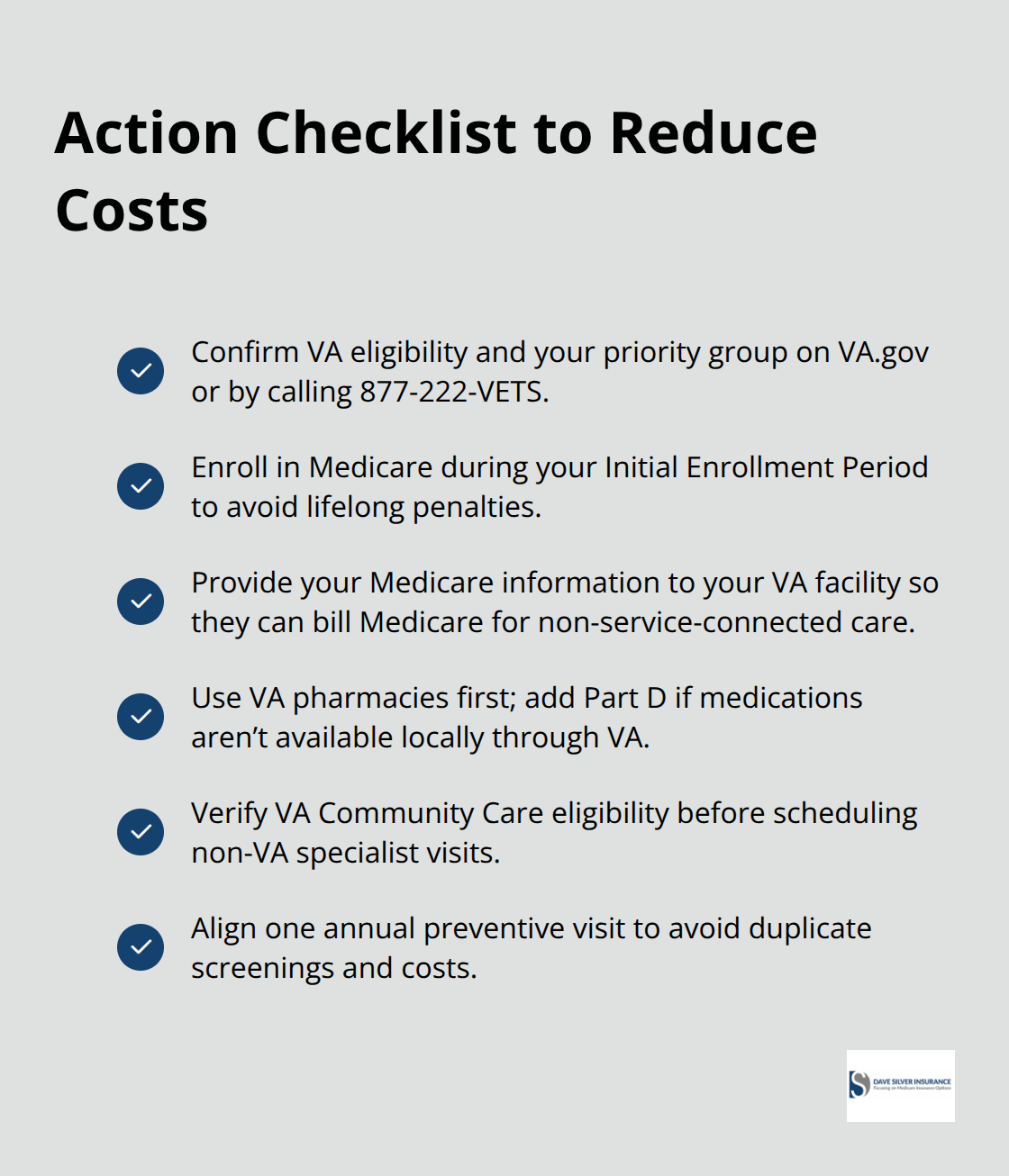

Your eligibility for specific VA benefits depends on your discharge status, service-connected disabilities, and priority group assignment, not simply on having served. You must obtain your discharge papers and verify your status through VA.gov or by calling the VA benefits line at 877-222-VETS to confirm which benefits you qualify for and your assigned priority group. Many veterans overestimate their VA coverage because they don’t understand that some benefits depend on priority group-dental and vision coverage, for example, varies significantly based on your rating percentage and priority assignment. Once you know your VA priority group, compare what that group actually covers against what Medicare would cover for the same services, then make enrollment decisions based on which system gives you better access and lower out-of-pocket costs for your specific health needs. If you have TRICARE as a military retiree, Medicare enrollment becomes mandatory to keep TRICARE for Life active, which coordinates with Medicare as a wraparound that covers the remainder after Medicare pays. Assuming you don’t need Medicare because you have VA benefits leaves you vulnerable to coverage gaps and locks you into higher penalties if you later change your mind.

Next Steps: Choosing the Right Medicare Plan for Your Situation

With your eligibility confirmed and enrollment timing locked in, the real work begins-selecting which Medicare plan type actually fits your health profile and financial situation.

Picking the Right Medicare Plan When You Have VA Benefits

Medicare Advantage vs. Medigap: Which Fits Your Situation

Medicare Advantage (Part C) bundles Parts A, B, and often D into a single plan with lower premiums-many offer $0 monthly costs-but it restricts you to in-network providers and typically includes copays for specialist visits and prescriptions. Medigap (supplemental insurance) works alongside Original Medicare to cover cost-sharing like deductibles and copays, giving you access to any Medicare-approved provider nationwide without networks or prior authorization. For veterans relying heavily on VA care, Medigap often makes more financial sense because it preserves maximum flexibility to use both VA and non-VA providers without coordination hassles.

However, if you live far from a VA facility or need specialists quickly, a Medicare Advantage plan with a strong local network might reduce your out-of-pocket costs despite the copay structure. Some plans marketed to veterans, like Humana Honor plans, include $0 copays for in-network mental health visits and routine dental with no-cost semiannual cleanings-benefits that offset higher deductibles if you use them regularly.

Making Your Plan Selection Decision

The critical decision comes down to your VA coverage level and access to VA facilities. If your VA priority group covers most of your care with minimal cost, add Medigap to fill gaps in dental, vision, and prescription drugs. If VA access is limited in your area or you prefer non-VA providers, Medicare Advantage with a robust network near you may save money despite the copays.

Providing Your Medicare Information to the VA

Give your VA facility your Medicare information so they can bill your insurance for non-service-connected care, offsetting VA copays when Medicare pays and potentially counting toward your annual deductible. This single action reduces your out-of-pocket expenses without requiring you to change providers or coverage types.

Coordinating Your Prescription Drug Coverage

Use VA pharmacies first for prescriptions because VA drug coverage is creditable under Medicare rules, meaning you can delay Medicare Part D enrollment without penalty if you rely primarily on VA medications. However, if you need medications unavailable at VA or live far from a VA pharmacy, Part D lets you access local pharmacies without late-enrollment penalties as long as you enrolled within 63 days of losing creditable coverage. Tell your VA clinician whenever you receive non-VA care so they coordinate treatment and avoid duplicate testing.

Maximizing Preventive Care and Reducing Duplicate Costs

Schedule one annual preventive checkup through your primary care provider-Medicare covers preventive services in full after the deductible, and aligning this visit between VA and Medicare prevents redundant screening and counts toward both systems’ requirements. If you have a Health Savings Account or Health Reimbursement Arrangement linked to a high-deductible health plan, you can use those funds to pay VA copays for non-service-connected care, a strategy many veterans miss entirely. For non-VA specialists, confirm whether your Medicare plan requires preauthorization and whether VA Community Care covers the visit if your VA facility has long wait times or lacks the specialty-VA Community Care covers certain non-VA visits when eligibility criteria like extended waits are met, so verifying this before scheduling saves surprise bills.

With your plan selected and coordination strategies in place, the next challenge emerges: most veterans still make costly mistakes during enrollment and throughout their coverage years that erode the savings these strategies create.

What’s Costing You Money With Medicare and VA Benefits

Permanent Penalties From Missing Enrollment Deadlines

Delaying Medicare Part B enrollment outside your Initial Enrollment Period without creditable employer coverage triggers a 20% late enrollment penalty (10% for each full 12-month period that you could have signed up), and this penalty compounds annually for the rest of your life. Veterans often rationalize skipping Medicare because they have VA coverage, but this assumption costs them thousands. If you’re a military retiree with TRICARE, Medicare enrollment isn’t optional-you must enroll in Parts A and B to keep TRICARE for Life active as a wraparound.

The 2026 Medicare Part D out-of-pocket cap rises to $2,100 according to Medicare.gov, meaning your prescription drug costs are capped, yet many veterans never enroll in Part D because they assume VA pharmacy coverage is sufficient. This leaves them vulnerable when they need medications the VA doesn’t stock or when they live too far from a VA facility.

Missing the General Enrollment Period (January 1 through March 31) means your coverage won’t start until July 1 of that year, creating a dangerous gap where you have no drug coverage for months. Dropping Part B and trying to reinstate it later typically requires waiting until January of the following year, and reinstatement may involve additional penalties that stack on top of your original delayed-enrollment penalty. Veterans in Priority Group 1 with a 100% VA disability rating often skip Medicare entirely, believing their VA benefits cover everything, but VA explicitly limits dental and vision benefits by priority group-Medicare fills these gaps that VA won’t.

Failing to Coordinate Care Across Both Systems

The second major mistake is failing to coordinate your VA and Medicare benefits at the point of service. When you receive non-VA care, you must tell your VA clinician so they can coordinate your records and prevent duplicate testing, yet most veterans never mention outside care to their VA providers. The VA can bill your private Medicare insurance for non-service-connected care, but this only works if you actually provide your Medicare information to the VA-many veterans never do, missing the chance to offset copays.

If you enroll in a Medicare Advantage plan without understanding your VA access, you may end up paying copays for specialists when VA Community Care would have covered the visit at no cost if you met eligibility criteria like long wait times. The VA Community Care program covers certain non-VA visits when specific conditions are met, but most veterans don’t know this program exists or how to verify eligibility before scheduling.

Missing Tax-Advantaged Savings Strategies

Using a Health Savings Account or Health Reimbursement Arrangement to pay VA copays for non-service-connected care is a strategy most veterans miss entirely, yet if you have an HDHP-linked HSA, you can reimburse yourself for VA copays tax-free. Scheduling your annual preventive checkup through both VA and Medicare separately means you’re paying twice for screening and testing that counts toward both systems-one coordinated visit prevents duplicate costs and fulfills requirements for both programs.

Overpaying With Veteran-Targeted Medicare Advantage Plans

Medicare Advantage plans marketed specifically to veterans with terms like Honor or Patriot can create duplicate spending if most of your care comes from the VA, since the government pays these plans a monthly rate regardless of whether you actually use their network. The solution requires verifying which services and locations your Medicare plan covers, then confirming whether VA Community Care will cover non-VA visits before you schedule them, but this coordination step intimidates most veterans into inaction.

Final Thoughts

The path forward with Medicare for veterans benefits requires one critical shift in mindset: stop treating VA and Medicare as competing systems and start using them as complementary tools. Veterans who coordinate both programs strategically cut their out-of-pocket costs significantly compared to those relying on a single system. Your enrollment timing, plan selection, and ongoing coordination decisions determine whether you save thousands annually or leave money on the table through missed deadlines and duplicate services.

Start by confirming your VA eligibility and priority group through VA.gov or 877-222-VETS, then enroll in Medicare during your Initial Enrollment Period regardless of your VA coverage level. Provide your Medicare information to your VA facility so they can bill for non-service-connected care and offset your copays. If you have a strong VA network nearby and comprehensive coverage through your priority group, add Medigap to fill gaps in dental, vision, and prescription drugs, or choose a Medicare Advantage plan with a robust local network if VA access is limited in your area.

We at Dave Silver Insurance have spent over 17 years helping veterans navigate Medicare enrollment and optimize their coverage through personalized guidance on Medicare Parts A, B, C, and D, plus Medigap options tailored to your specific health and financial situation. Contact Dave Silver Insurance to get clarity on your Medicare for veterans benefits and confidence in your healthcare strategy-our team is accessible seven days a week to answer your questions and ensure you make enrollment decisions that fit your life.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation

https://shorturl.fm/8Uqu9