Medigap Plan G is one of the most popular supplemental insurance options for Medicare beneficiaries, and for good reason. It covers many of the costs that Original Medicare leaves you responsible for, including copayments, coinsurance, and deductibles.

At Dave Silver Insurance, we’ve helped thousands of people understand their Medigap plan G overview and find the right coverage for their needs. This guide walks you through exactly what Plan G covers, what it doesn’t, and how much you can expect to pay.

What Medigap Plan G Is and How It Works

Understanding Plan G Coverage

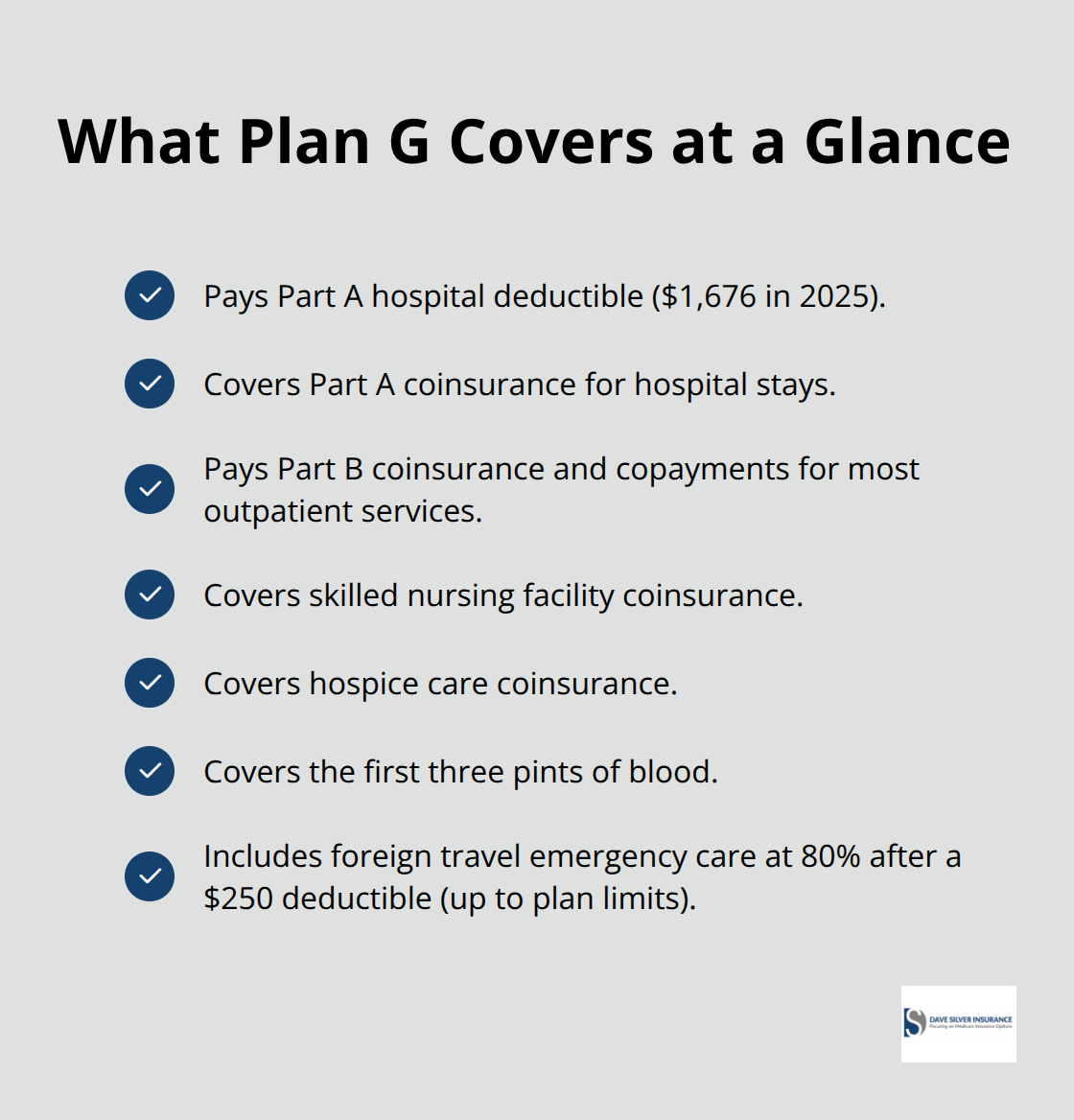

Medigap Plan G is a standardized supplemental insurance policy sold by private insurers that works alongside Original Medicare to cover costs Medicare doesn’t pay. According to Medicare.gov, Plan G covers the Part A hospital deductible ($1,676 in 2025), Part A coinsurance, Part B coinsurance or copayments for most services, skilled nursing facility coinsurance, hospice care coinsurance, and the first three pints of blood. The one significant gap is the Part B deductible, which is $283-you pay this out of pocket before Plan G starts covering anything. Plan G also includes foreign travel emergency coverage at 80 percent up to plan limits after a $250 deductible. Because all Plan G policies are standardized, the benefits are identical regardless of which insurance company sells it to you; the only difference between carriers is price and service quality.

How Plan G Coordinates with Original Medicare

When you have Plan G, Original Medicare remains your primary coverage. Medicare pays its portion (typically 80 percent for outpatient services after you meet your deductible), and Plan G pays the remaining 20 percent coinsurance or copayment. For hospital stays, Medicare covers your inpatient costs for up to 60 days, then charges you a daily copay from day 61 to 90, and another daily copay from day 91 to 150. Plan G covers all these copays, plus it extends coverage up to 365 additional hospital days after Medicare benefits end. This layering of coverage means you can see any provider nationwide that accepts Original Medicare-there are no network restrictions with Plan G.

You’ll pay a monthly premium to your Medigap insurer on top of your Medicare Part B premium, but once you meet the Part B deductible and any coinsurance requirements, Plan G handles the rest for covered services.

Your Enrollment Window and Guaranteed Coverage

Your Medigap Open Enrollment Period starts the month you turn 65 and enroll in Medicare Part B, lasting six months. Enroll during this window and insurers must accept you without health questions and cannot charge you more based on medical history. Miss this deadline and you face medical underwriting, potential denial, or higher premiums depending on your state. Some states like California and Maine offer year-to-year protections, but most don’t. Starting January 1, 2020, Plan G became the most comprehensive Medigap option available to new Medicare enrollees because Plan F-which covered the Part B deductible-closed to new applicants. If you already had Plan F before 2020, you can keep it, but switching to Plan G typically means lower monthly premiums with only the Part B deductible as your additional out-of-pocket responsibility. The timing of your enrollment matters significantly for your long-term costs, making the six-month Open Enrollment Period your best opportunity to secure affordable coverage. Understanding these eligibility rules helps you move forward with confidence as you explore what Plan G actually costs.

Coverage Details of Medigap Plan G

What Plan G Covers in Real Dollars

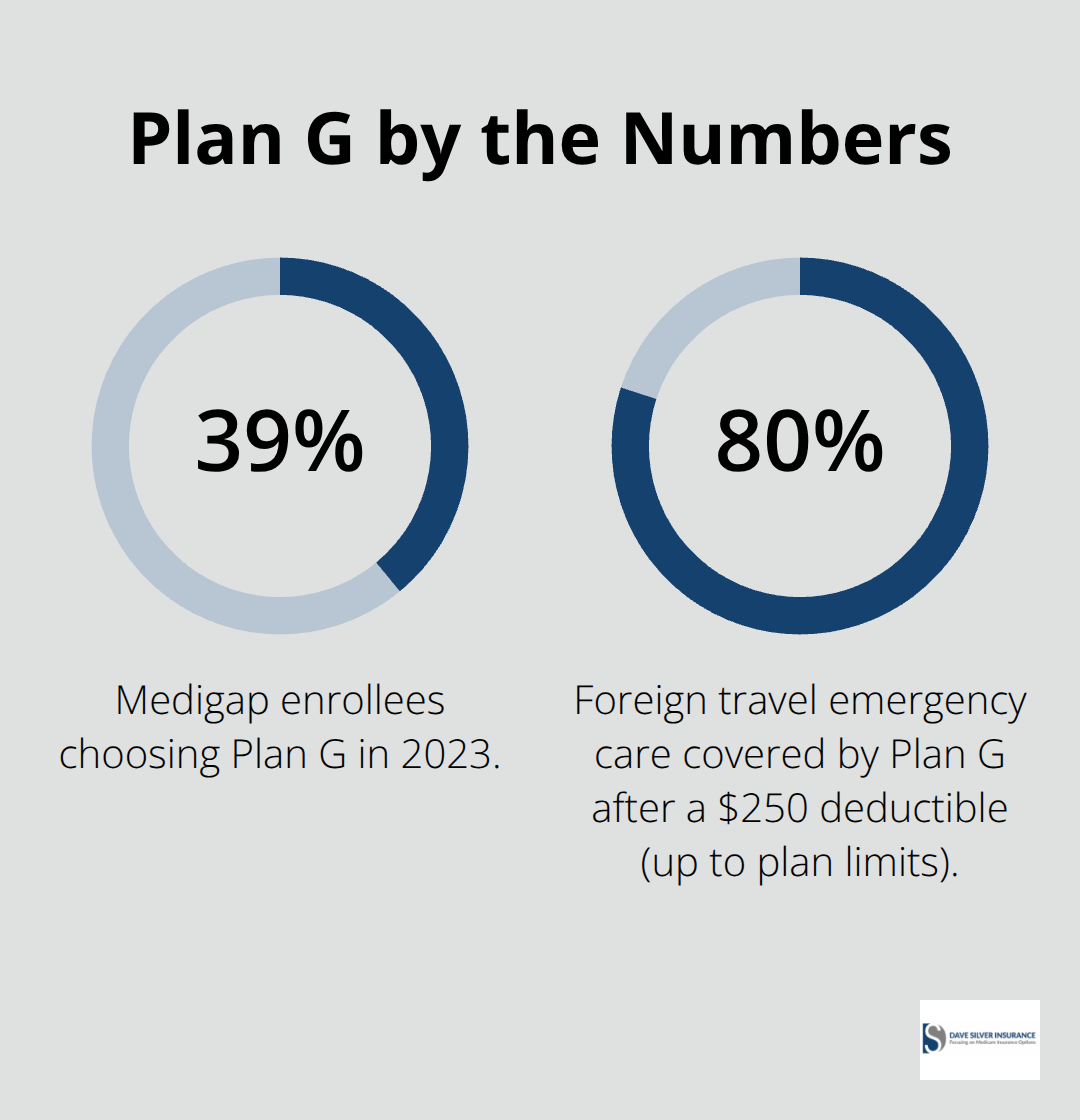

Plan G covers most of what Original Medicare leaves unpaid, but understanding the specifics matters because gaps exist. According to Medicare.gov, Plan G pays the Part A hospital deductible ($1,676 in 2025), all Part A coinsurance for hospital stays, Part B coinsurance and copayments for doctor visits and outpatient services, skilled nursing facility coinsurance, hospice care coinsurance, and the first three pints of blood needed during a hospital stay. For hospital coverage specifically, Plan G extends your stay beyond Medicare’s limits-it covers up to 365 additional hospital days after your Medicare benefits end, which protects you from catastrophic costs in serious illness scenarios. Foreign travel emergency care receives 80 percent coverage up to plan limits after you pay a $250 deductible, meaning a medical crisis while traveling internationally won’t drain your savings completely.

The Part B deductible represents the critical gap-you pay this out of pocket before Plan G coverage activates for any Part B services. Plan G also doesn’t cover routine dental, vision, or hearing care, and it doesn’t include prescription drug coverage, which requires a separate Part D plan enrollment.

How Plan G Stacks Against Other Options

Plan N costs less monthly but requires you to pay the Part B deductible plus potential copayments of $20 for doctor visits and $50 for emergency room visits, plus any excess charges providers bill above Medicare-approved amounts. Plans K and L cap your annual out-of-pocket costs at $8,000 and $4,000 respectively in 2026, which sounds protective but means higher monthly premiums and you absorb costs up to those limits. Plan A and Plan B offer minimal coverage compared to Plan G.

The High-Deductible Alternative

The high-deductible Plan G option carries a $2,950 deductible in 2026 before the plan pays anything, but monthly premiums drop dramatically-sometimes under $70 compared to $100–$200 for standard Plan G depending on your state and age. The tradeoff works only if you’re healthy and can afford the deductible when needed. For most people, standard Plan G provides the best balance: comprehensive coverage with manageable monthly costs and predictable out-of-pocket expenses beyond the Part B deductible and coinsurance.

Your actual costs depend on which version you select and where you live, which brings us to the premium variations that significantly impact your long-term healthcare budget.

What Plan G Costs and Where Your Money Goes

State-by-State Premium Variations

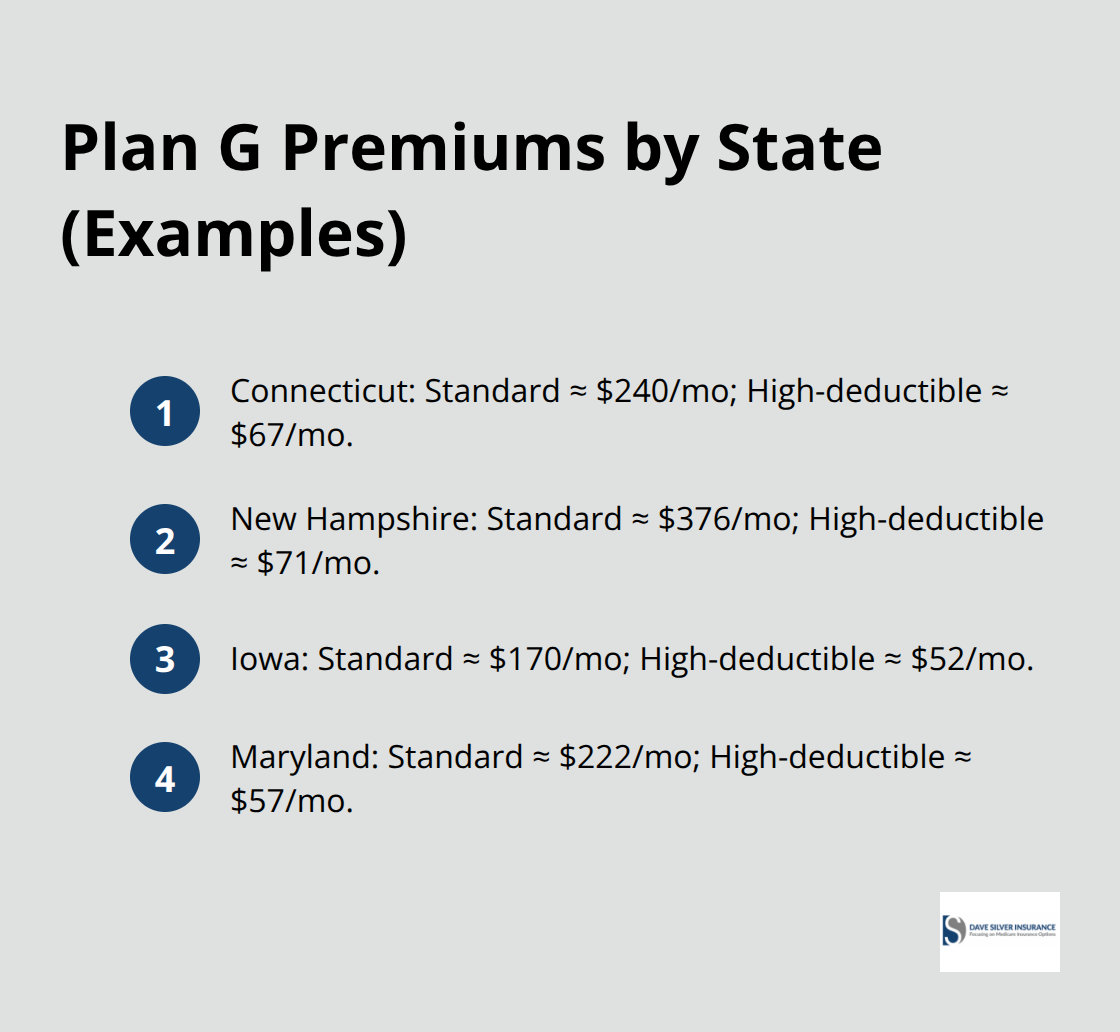

Plan G premiums vary dramatically by location, with monthly costs ranging from roughly $67 to $376 depending on your state and age. Connecticut residents pay around $240 monthly for standard Plan G, while New Hampshire premiums reach $376, according to 2025 data. Iowa offers the lowest-cost option at approximately $170 monthly, and Maryland sits in the middle at $222. These aren’t theoretical numbers-they represent what actual enrollees pay today.

The high-deductible Plan G alternative slashes premiums significantly: Connecticut drops to $67 monthly, Iowa to $52, Maryland to $57, and New Hampshire to $71.

When the High-Deductible Option Makes Sense

If you’re healthy and can absorb the $2,950 annual deductible before coverage activates, the savings compound over time. About 39 percent of people with standardized Medigap plans chose Plan G in 2023, making it the dominant choice among Medicare beneficiaries who want comprehensive coverage. The high-deductible version works best for those with predictable, manageable healthcare needs and sufficient savings to cover the deductible when medical expenses arise.

Factors That Control Your Premium

Your actual premium depends on factors insurers control and factors you control. Age matters-insurers rate plans based on your current age, so waiting to enroll costs more later. Tobacco use increases premiums substantially, while being married or female often qualifies you for discounts. Tobacco users pay significantly higher rates than non-smokers across all states and carriers.

Paying annually instead of monthly typically saves 5 to 10 percent, and setting up automatic bank transfers sometimes yields another small reduction. Location determines everything because state regulations and local competition shape pricing; a Plan G policy in one zip code costs differently than the same policy miles away.

How to Shop for the Best Price

The critical action: contact multiple insurers for quotes on the identical Plan G plan letter in your area. Since Medigap policies are standardized, the only legitimate difference between carriers is price. Gather quotes from at least three companies, then check each insurer’s rate history over the past decade-some raise premiums aggressively while others stay stable. Your state insurance department publishes complaint data against insurers; review it before committing.

If you qualify for guaranteed issue rights or enrolled during your Medigap Open Enrollment Period, insurers cannot deny you or charge more based on health status, which means price shopping becomes your sole negotiating tool. This protection makes your enrollment window the ideal time to lock in competitive rates before underwriting restrictions apply.

Final Thoughts

Plan G stands out as the most comprehensive Medigap option for new Medicare enrollees, covering nearly all costs that Original Medicare leaves unpaid except the Part B deductible. Your Medigap plan G overview should focus on three realities: standard Plan G offers predictable out-of-pocket expenses with monthly premiums ranging from $67 to $376 depending on your state, the high-deductible version cuts premiums dramatically if you’re healthy and can absorb the $2,950 annual deductible, and enrollment timing determines whether insurers can deny you or charge more based on health status.

Gather quotes from at least three insurers for the identical Plan G plan letter in your area, then review each company’s rate history over the past decade to identify which carriers maintain stable premiums versus aggressive increases. Check your state insurance department’s complaint data before selecting a carrier. If you’re currently on Plan F and considering a switch, calculate whether the lower Plan G premiums offset paying the Part B deductible yourself.

We at Dave Silver Insurance help people navigate these exact decisions every day. Contact Dave Silver Insurance to receive personalized guidance on your Medicare coverage and find the plan that matches your life, not the other way around.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation