Many people ask us whether Medigap and supplemental insurance are the same thing. The short answer is no-they’re different products that serve different purposes.

At Dave Silver Insurance, we’ve helped countless Medicare beneficiaries navigate these options. Understanding the distinction between them can save you thousands in out-of-pocket costs.

What Medigap Actually Covers

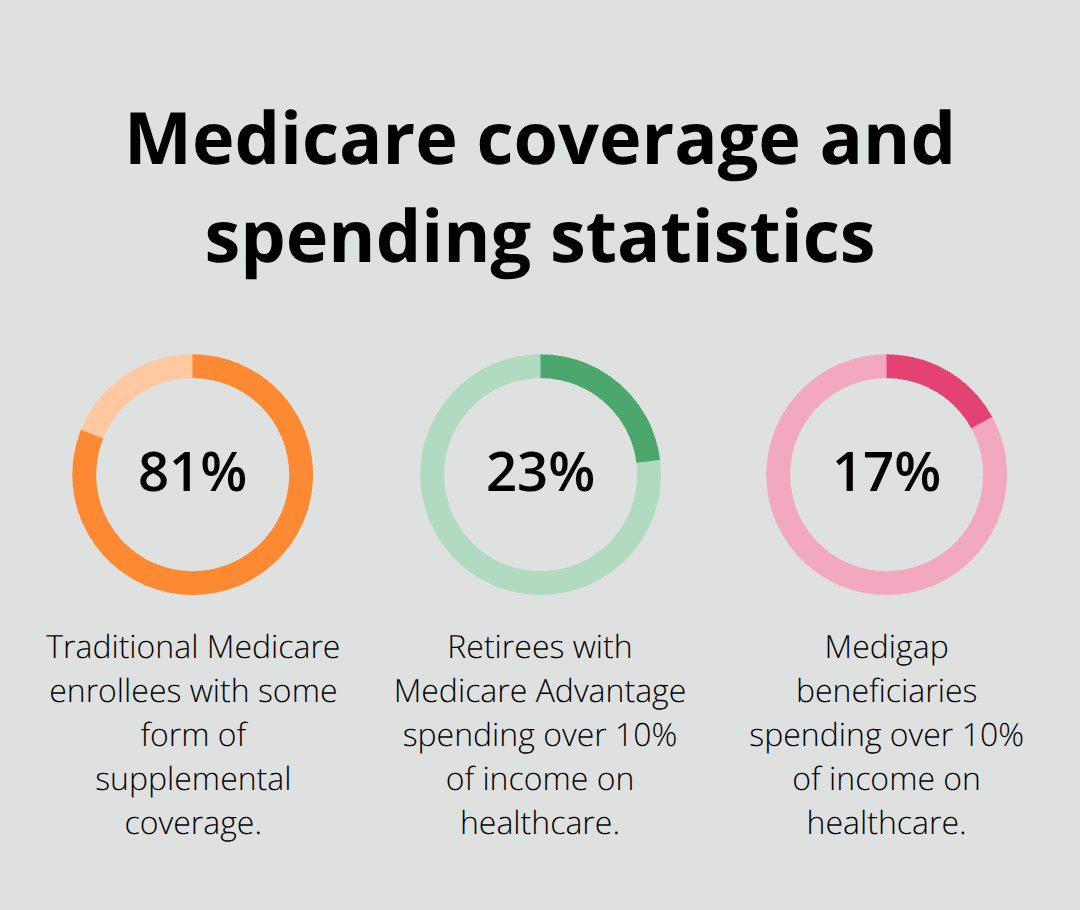

Medigap is Medicare Supplement Insurance sold by private insurers to fill the gaps that Original Medicare leaves behind. Original Medicare Part A and Part B cover basic hospital and doctor services, but they don’t cover everything. In 2025, you’ll pay a $1,676 deductible per benefit period for hospital stays under Part A, plus $257 for Part B services. After that, you’re responsible for 20% coinsurance on most doctor visits and outpatient care. If you stay in the hospital beyond 60 days, you’ll pay $419 per day for days 61–90, and $838 per day for lifetime reserve days. Medigap steps in to reimburse these out-of-pocket costs, making your healthcare expenses far more predictable. According to the National Academy of Social Insurance, about 81% of traditional Medicare enrollees carry some form of supplemental coverage because the financial risk of going without it is simply too high.

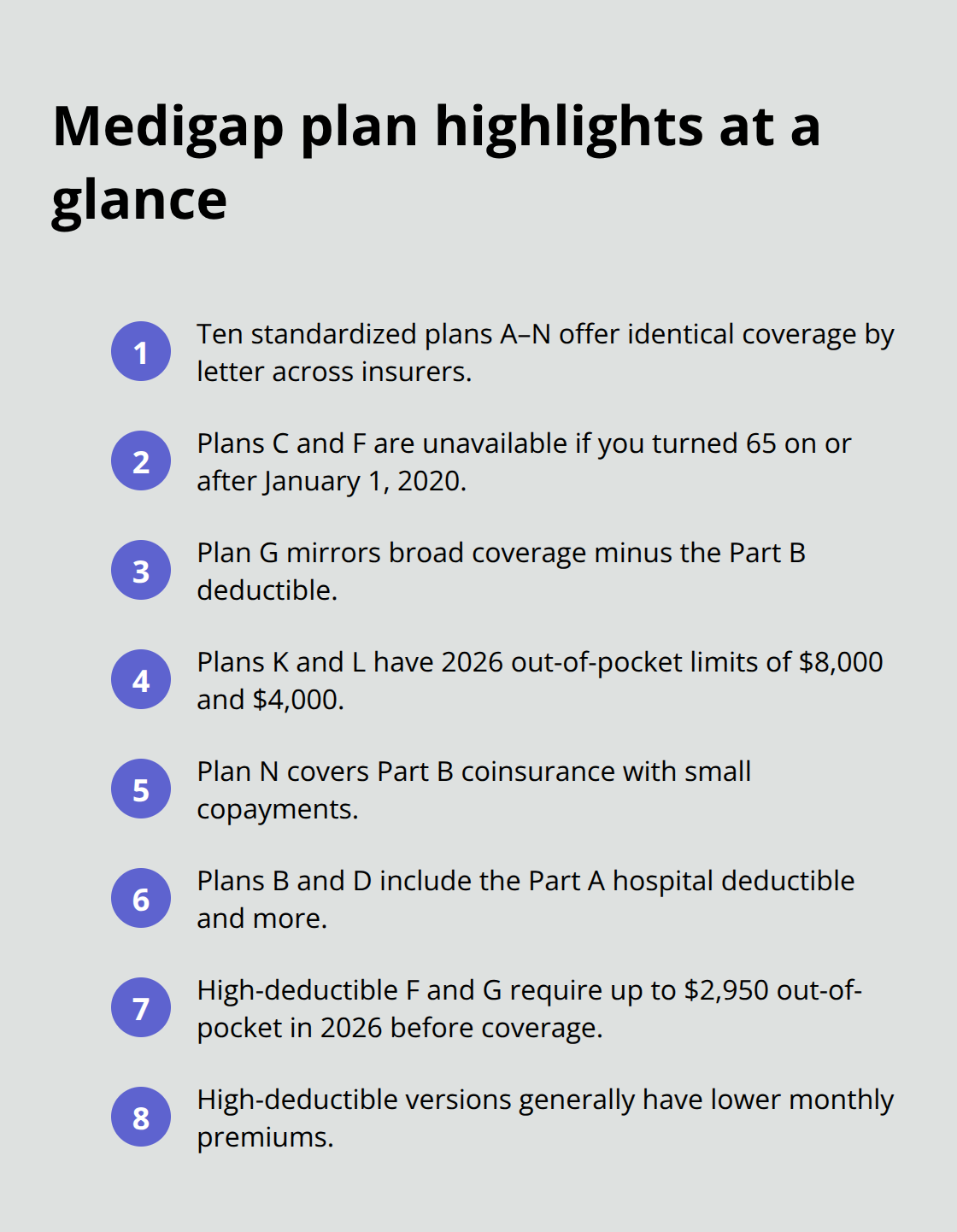

The 10 Standardized Plans You Need to Know

Ten standardized Medigap plans exist, labeled A through N, and plans with the same letter must offer identical coverage across all insurers. Plans C and F are no longer available to anyone who turned 65 on or after January 1, 2020, though Plan G serves as a modern alternative with the same broad coverage minus the Part B deductible. Plans K and L carry lower premiums but include an annual out-of-pocket limit of $8,000 and $4,000 respectively in 2026, after which the plan pays 100% of covered services for the rest of the year. Plan N offers another lower-cost option that covers Part B coinsurance with small copayments for certain office visits and emergency room trips. More comprehensive plans like B and D cover the Part A hospital deductible plus additional costs, which explains why their premiums run significantly higher.

High-deductible versions of Plans F and G exist in some states, requiring you to pay up to $2,950 out-of-pocket in 2026 before coverage begins, but these plans cost substantially less month to month.

How Medigap Connects to Your Medicare Benefits

Medigap works exclusively with Original Medicare Part A and Part B, not with Medicare Advantage. You cannot hold both a Medigap policy and a Medicare Advantage plan simultaneously. Once you enroll in Part A and Part B, you can purchase a Medigap policy from any private insurer offering coverage in your state. The policy pays its share of Medicare-approved charges after you meet applicable deductibles, covering items like Part A coinsurance for hospital stays, Part B coinsurance for doctor services, the first three pints of blood annually, and hospice care coinsurance. Some plans also cover skilled nursing facility coinsurance and Part A or Part B deductibles entirely. The best time to purchase is within a 6 month “Medigap Open Enrollment” period that starts the first month you have Medicare Part B and you’re 65 or older, when insurers must offer all plans without health underwriting and cannot charge higher premiums based on preexisting conditions. Outside this guaranteed issue window, health questions and potential denials become real risks. Medigap premiums vary dramatically by insurer and location, ranging from roughly $30–40 monthly for basic plans to $400 or more for comprehensive coverage, so comparing quotes across multiple carriers in your area is non-negotiable.

What Medigap Doesn’t Cover

Medigap policies do not include prescription drug coverage, which means you must enroll in a separate Medicare Part D plan to access medications. These policies also exclude long-term care, vision, dental, hearing aids, and eyeglasses-gaps that many beneficiaries overlook when selecting their coverage. Some plans do offer foreign travel emergency coverage (up to plan limits), which can prove valuable if you travel internationally. Understanding these limitations helps you identify what other coverage you might need alongside your Medigap policy. This distinction between what Medigap covers and what it doesn’t becomes especially important when you compare it to other types of supplemental insurance available in the marketplace.

What Supplemental Insurance Actually Means

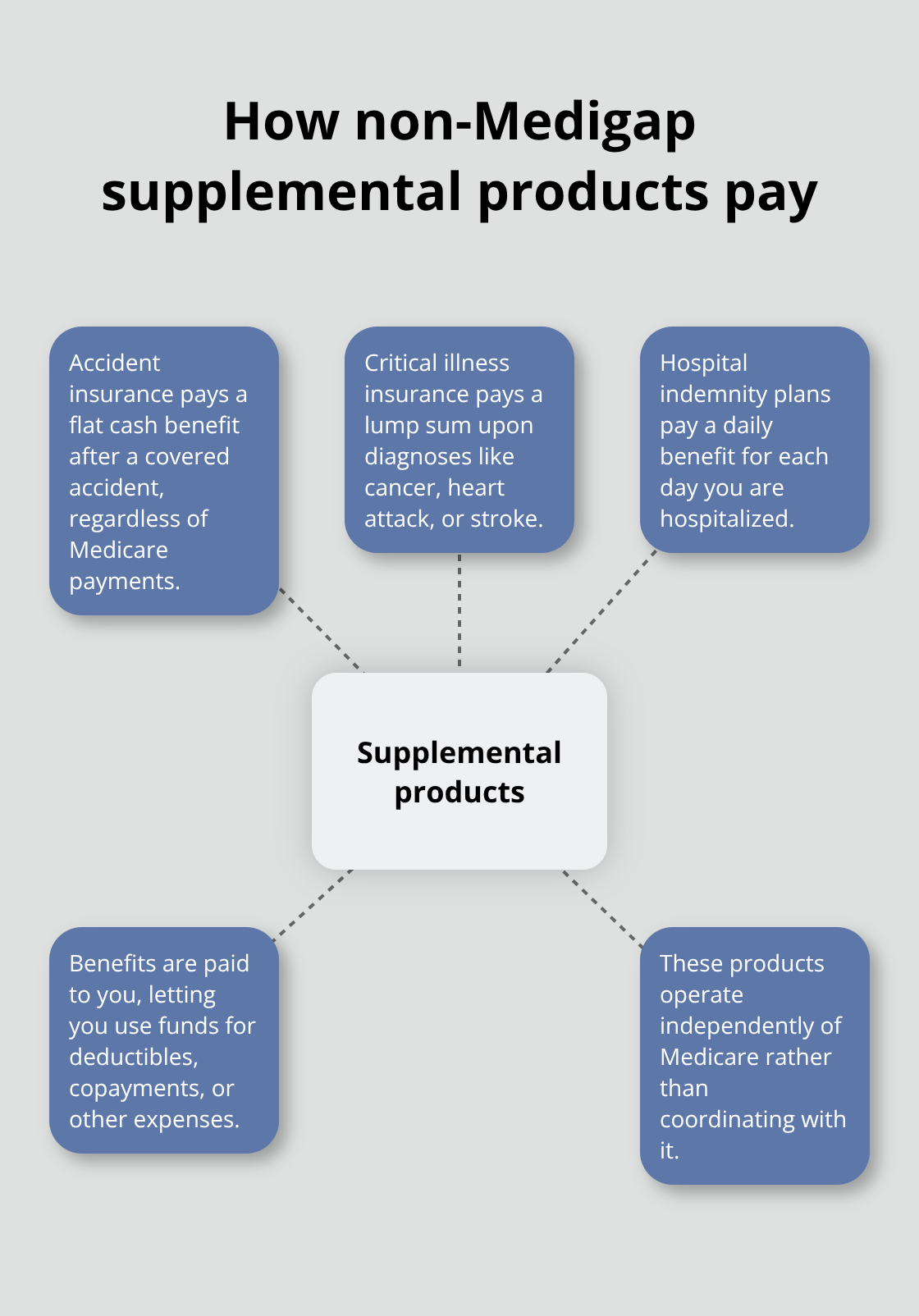

Supplemental insurance is a broad category of coverage designed to fill gaps left by primary insurance plans, and Medigap is actually one specific type within that larger universe. The term supplemental insurance encompasses any policy purchased to cover costs that your main insurance doesn’t pay, which could include accident insurance, critical illness coverage, hospital indemnity plans, or long-term care insurance. These products work differently than Medigap because they operate independently of Medicare rather than coordinating with it.

How Non-Medigap Supplemental Products Function

When you buy accident insurance, you receive a flat cash benefit if you suffer a covered accident, regardless of what Medicare pays. Critical illness insurance pays a lump sum if you’re diagnosed with conditions like cancer, heart attack, or stroke, giving you money to use however you need it. Hospital indemnity plans pay a daily benefit for each day you’re hospitalized, which you can use toward deductibles, copayments, or other expenses.

The key distinction is that these supplemental products don’t coordinate with Medicare the way Medigap does; they simply provide additional cash or benefits on top of whatever your primary coverage pays.

Why the Distinction Matters for Your Coverage Strategy

Medigap specifically reimburses Medicare’s cost-sharing amounts like deductibles and coinsurance, making your healthcare expenses predictable by design. Other supplemental products provide lump-sum payments or daily benefits that you control, which means they’re useful for expenses Medicare doesn’t address at all, such as home modifications during recovery, temporary lost income, or other non-medical costs. Many beneficiaries benefit from combining both types of coverage. You might carry a Medigap plan to handle Medicare’s deductibles and coinsurance while also holding a hospital indemnity plan that pays a daily benefit during inpatient stays, giving you extra cash to cover transportation, meal costs, or household help. This layered approach works because the supplemental products don’t interfere with Medigap-they simply add another financial cushion.

The Real Risk: Assuming Coverage Without Verification

The mistake we see repeatedly is when people assume that buying any supplemental coverage means they’re protected against all out-of-pocket costs. They’re not. Each product covers specific situations, and gaps remain if you don’t strategically combine them. Understanding what each type actually pays for, rather than what the marketing promises, is what separates informed beneficiaries from those who face unexpected bills. The differences between Medigap and other supplemental insurance become even more important when you examine how enrollment periods and eligibility requirements affect your ability to access these plans.

Where Medigap and Supplemental Coverage Truly Diverge

How Reimbursement Models Create Different Financial Outcomes

Medigap and other supplemental insurance products operate on fundamentally different financial mechanics, and this distinction directly impacts your out-of-pocket costs. Medigap reimburses specific percentages of Medicare’s cost-sharing amounts, meaning if you have a Plan G and incur a $419 daily hospital coinsurance charge for days 61–90, your Medigap policy covers that exact amount. Hospital indemnity insurance works differently: it pays you a flat daily benefit (typically $100–$300 per day) regardless of what you actually owe Medicare. If you stay hospitalized for five days and your policy pays $200 daily, you receive $1,000 total, whether your actual coinsurance was $419 or $838. This cash-based approach means supplemental products sometimes overpay your costs and sometimes underpay them, leaving gaps.

Critical illness insurance adds another layer of unpredictability by paying lump sums only for diagnosed conditions like cancer or stroke, not for routine hospitalizations or doctor visits. A Center for Retirement Research study found that 23% of retirees with Medicare Advantage spent more than 10% of their income on healthcare costs, compared with 17% of Medigap beneficiaries, demonstrating how predictable Medigap reimbursement protects your finances better than variable supplemental products.

Waiting Periods and Immediate Coverage

Non-Medigap supplemental plans impose waiting periods (typically 30–180 days) before benefits activate, whereas Medigap coverage begins immediately. This matters enormously: if you purchase hospital indemnity insurance in March and suffer a heart attack in April, you may receive nothing. The timing of your purchase directly determines whether you have protection when you need it most.

Enrollment Windows and Health Underwriting

Enrollment timing creates the sharpest practical difference between these products. Medigap’s 6-month guaranteed issue period allows you to purchase any plan without health questions or higher premiums regardless of preexisting conditions. Outside this window, insurers can deny your application or charge substantially more based on your health history. Other supplemental insurance products typically have no such guaranteed issue protection; insurers routinely underwrite applications and can reject you outright for conditions like diabetes, heart disease, or previous cancer.

Provider Network Freedom and Coverage Scope

Your provider network flexibility also diverges significantly. Medigap plans work with any doctor or hospital accepting Medicare, giving you complete freedom to see any specialist without referrals or authorization delays. Hospital indemnity and critical illness plans impose no network restrictions because they don’t coordinate with doctors at all, but accident insurance sometimes limits coverage to accidents occurring in specific circumstances. The real-world consequence: a Medigap beneficiary can switch doctors monthly without losing coverage, while someone relying solely on accident insurance has no ongoing coverage for routine care whatsoever.

Medigap stands out as your primary supplemental strategy because its guaranteed enrollment window, predictable reimbursement, and unlimited provider access create financial stability that other supplemental products cannot match. You can layer additional coverage on top, but Medigap should form your foundation.

Final Thoughts

The answer to whether Medigap and supplemental insurance are the same is straightforward: no, they’re not. Medigap reimburses Medicare’s cost-sharing amounts directly, while supplemental insurance encompasses a broader category including accident insurance, critical illness coverage, and hospital indemnity plans that operate independently of Medicare. This distinction shapes your financial protection in meaningful ways, with Medigap beneficiaries spending significantly less on healthcare than those relying on other supplemental products.

Medigap offers predictable reimbursement tied directly to Medicare’s deductibles and coinsurance, eliminating the guesswork about what you’ll actually pay out of pocket. A Center for Retirement Research study showed that 17% of Medigap beneficiaries spent more than 10% of their income on healthcare, compared with 23% of Medicare Advantage enrollees, demonstrating Medigap’s superior financial protection. The 6-month guaranteed issue period starting when you turn 65 and enroll in Part B represents your best opportunity to purchase without health underwriting, as insurers can deny your application or charge higher premiums based on preexisting conditions if you miss this window.

Many beneficiaries benefit from layering coverage strategically by combining a Medigap plan with hospital indemnity insurance to add extra cash during inpatient stays, or pairing Medigap with critical illness coverage for additional financial protection. We at Dave Silver Insurance help Medicare beneficiaries navigate these decisions with personalized guidance based on your unique health and financial situation. Contact us today to clarify your Medicare strategy and move forward with confidence-we’re accessible seven days a week to answer your questions.