Medicare Part A is the foundation of your coverage, but understanding what it actually covers-and what it costs-can be confusing.

We at Dave Silver Insurance help thousands of people navigate their Medicare Part A overview each year. This guide walks you through eligibility requirements, coverage details, and real costs so you can make informed decisions about your healthcare.

Who Qualifies for Medicare Part A

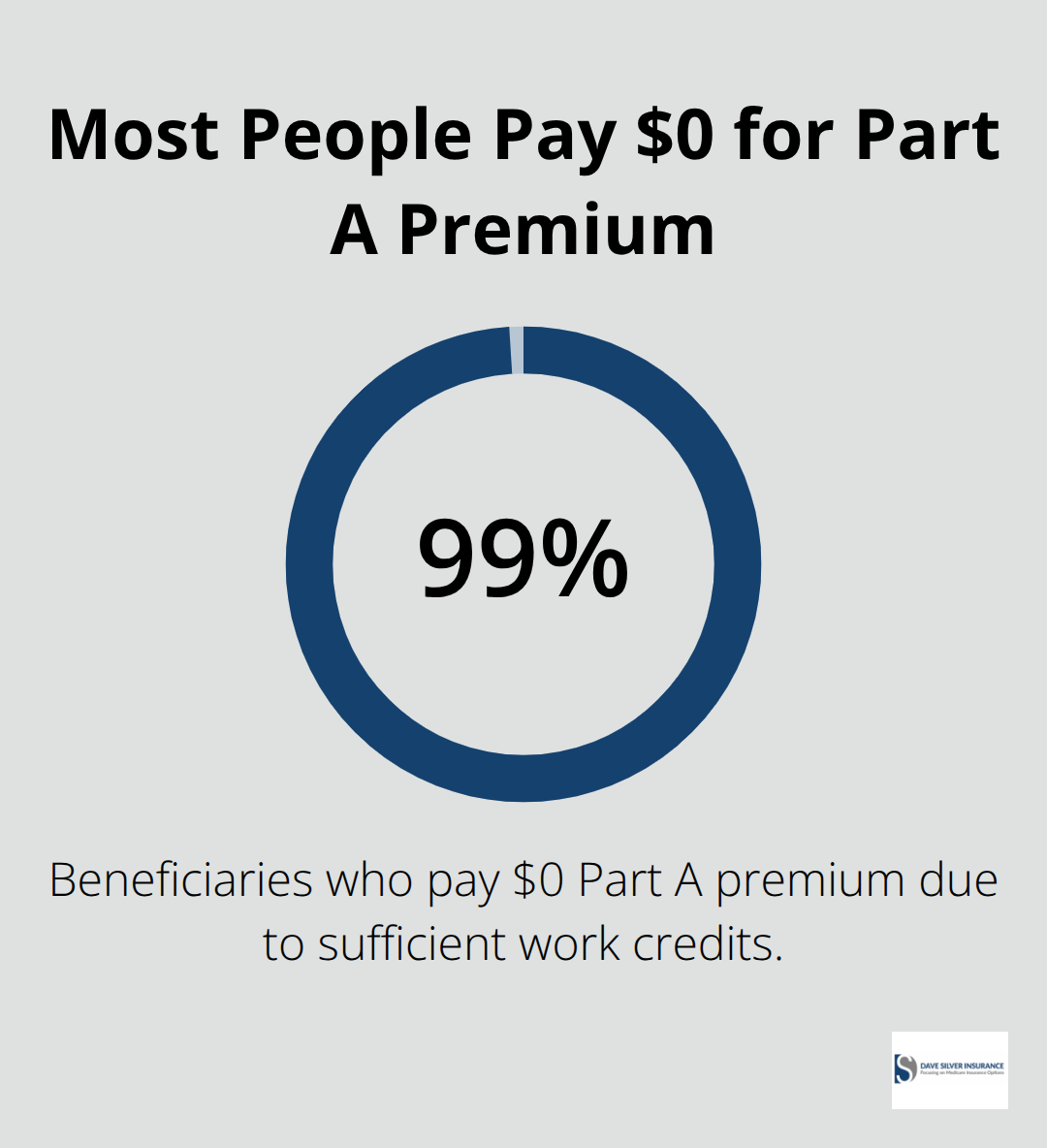

You qualify for Medicare Part A if you’re 65 or older and have earned at least 40 Social Security credits, which you earn when you work and pay Social Security taxes. About 99% of beneficiaries don’t pay a Part A premium because they meet this work history requirement.

If you’ve already started receiving Social Security or Railroad Retirement Board benefits before turning 65, you’re automatically enrolled in Part A at 65 with no action needed on your part. However, if you haven’t claimed Social Security yet, you must actively file with the Social Security Administration to enroll in Part A. The enrollment window matters significantly: if you enroll within 6 months of turning 65, your coverage begins the month you turn 65, but if you miss this Initial Enrollment Period, your coverage starts the month after you apply, and you’ll face a Late Enrollment Penalty of up to 10% per year for the rest of your life.

Work History and Quarters of Coverage

The 40 credits requirement isn’t as strict as it sounds. You don’t need them earned consecutively-they just need to be earned during your working years through FICA payroll taxes. One quarter requires $1,550 in wages in 2024, and you can earn up to four quarters per year. If you fall short of 40 credits, you can still purchase Part A at $311 per month in 2026 if you’re 65 or older. Those with fewer than 30 credits can buy full Part A coverage at $565 monthly. This option exists specifically for people who didn’t work long enough in the United States to qualify for premium-free coverage.

Qualifying Through Disability and Medical Conditions

Disability opens earlier eligibility before age 65. After you receive Social Security or Railroad Retirement Board disability benefits for 24 months, you automatically qualify for Part A. ALS patients receive special treatment-they qualify for Part A the first month their disability benefits begin with no waiting period. End-Stage Renal Disease creates another pathway: Part A coverage begins the third month after you start regular dialysis, or during the month of transplant. If you undergo dialysis training or hospitalization before transplant, your start date can shift up to two months earlier. These medical pathways ensure people facing serious conditions don’t wait unnecessarily for hospital coverage.

Taking Action Before Your Coverage Starts

The Social Security Administration handles all Part A enrollment applications and eligibility determinations. If you’re nearing 65 or your disability status changes, contact the Social Security Administration early to understand which enrollment period applies to you and avoid penalties. For ESRD or ALS scenarios, review the specific start dates and exceptions to maximize coverage and minimize gaps. The enrollment process uses multiple CMS forms, and SSA staff can walk you through the correct paperwork for your situation.

Understanding your eligibility path sets the stage for knowing what Part A actually covers and what you’ll pay out of pocket.

What Medicare Part A Actually Covers

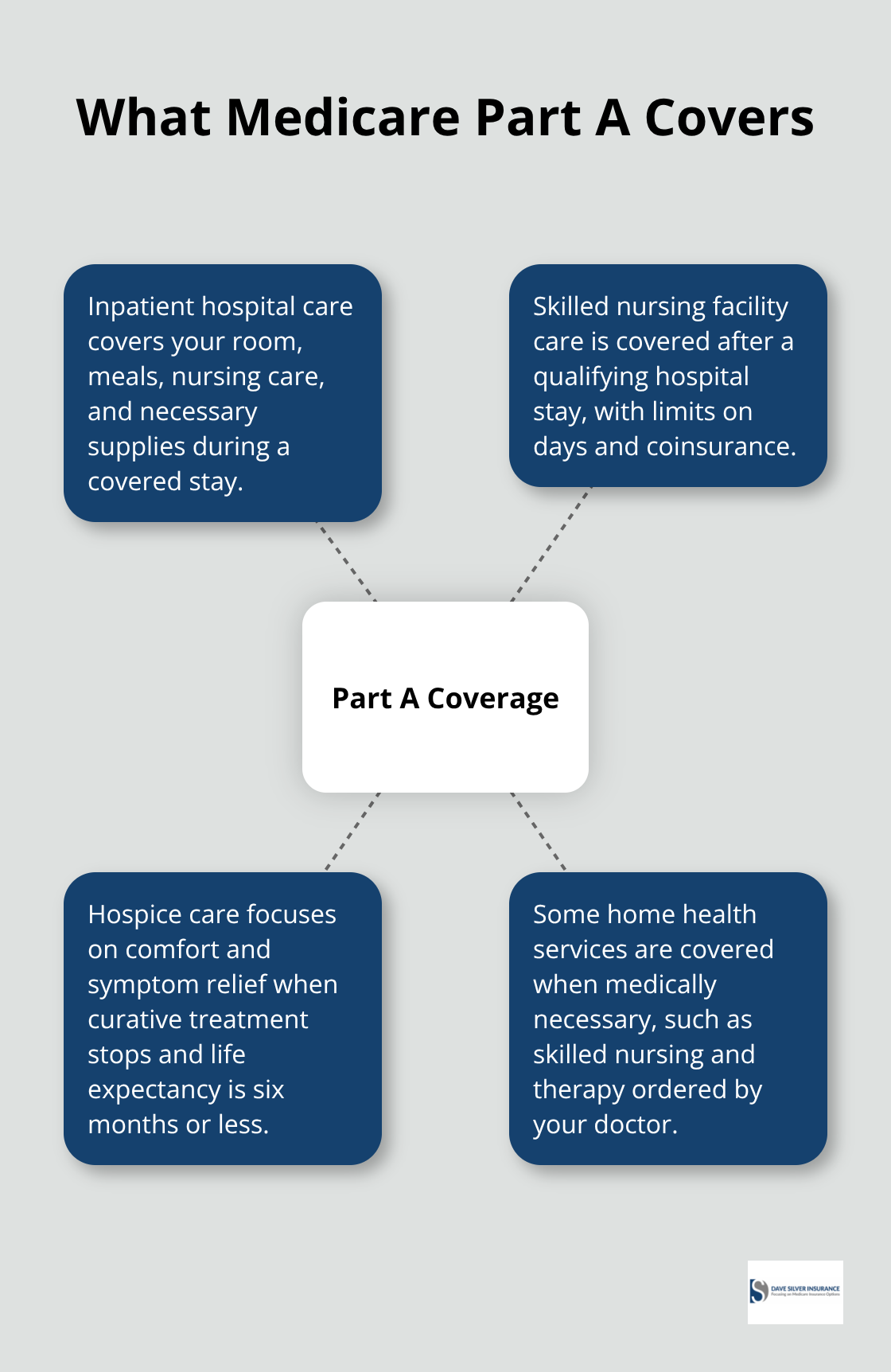

Medicare Part A covers inpatient hospital care, skilled nursing facility services, hospice care, and some home health services. The Centers for Medicare & Medicaid Services publishes detailed utilization data showing how beneficiaries use these services, and the numbers reveal what Part A actually pays for in real healthcare scenarios.

Hospital Inpatient Care

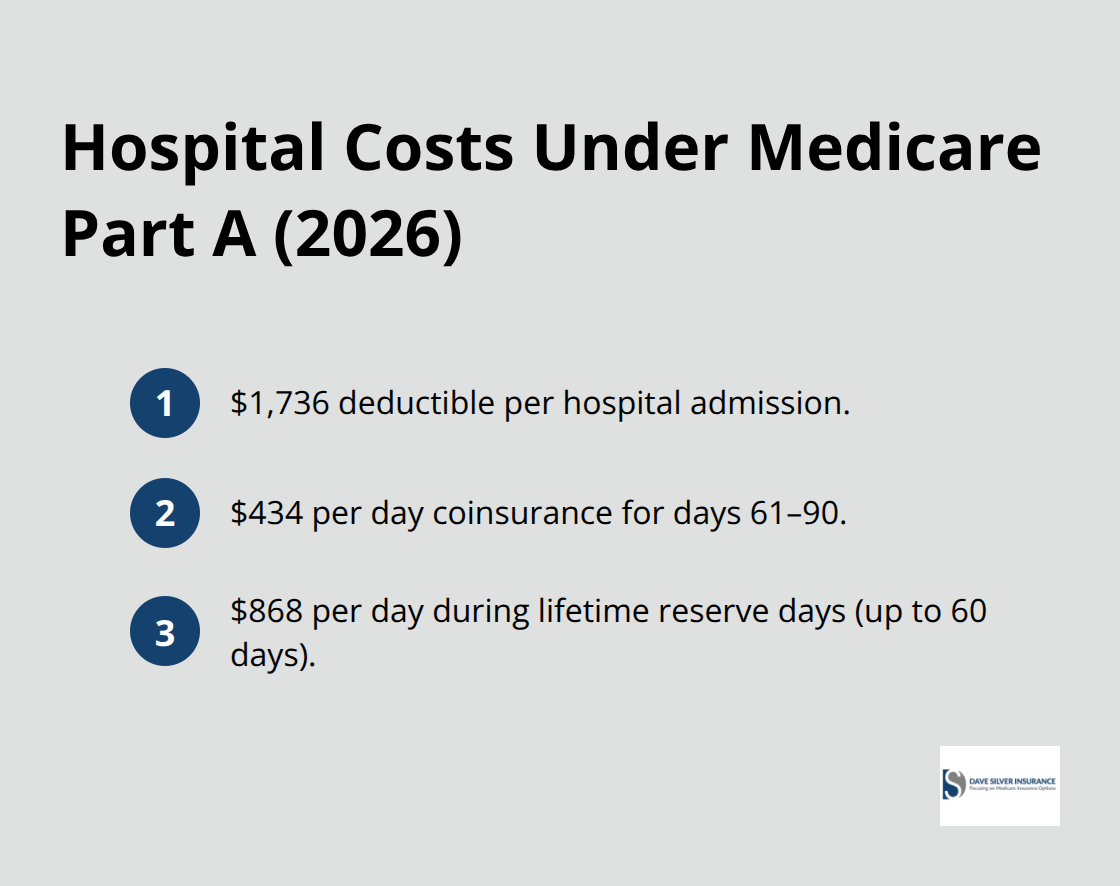

If a hospital admits you, Part A covers your bed, meals, nursing care, and basic medical supplies during your stay. You pay a $1,736 deductible per admission in 2026, then Part A covers everything for days one through 60. Days 61 through 90 cost you $434 daily, and if your hospitalization extends beyond 90 days, you have 60 lifetime reserve days available at $868 per day. Most people never exhaust these reserve days, but they exist for those facing extended hospitalizations from serious illnesses or injuries.

Skilled Nursing Facility Care

Skilled nursing facilities represent a significant portion of Part A utilization, though many people misunderstand when they qualify. Part A covers SNF care only after a hospital stay of at least three consecutive days, and only if you’re admitted to the facility within 30 days of hospital discharge. The facility must be Medicare-certified, and Part A pays the full cost for days one through 20, then you pay $217 daily for days 21 through 100 in 2026. After day 100, you’re responsible for all costs.

Hospice and Home Health Services

Hospice care under Part A covers pain management, symptom relief, and comfort-focused services when you’ve chosen to stop curative treatment and have a life expectancy of six months or less. Part A also covers some home health services when your doctor orders them, specifically skilled nursing visits, physical therapy, and occupational therapy, but not custodial care or general housekeeping. The key distinction is that Part A only covers medically necessary skilled care at home, not assistance with daily living activities (such as bathing or meal preparation). Understanding these coverage boundaries prevents costly surprises when you need care.

Now that you know what Part A covers, the real question becomes what these services actually cost you out of pocket.

What You Actually Pay for Part A

Hospital Deductibles and Daily Costs

The $1,736 hospital deductible in 2026 applies per admission, then Part A covers your inpatient hospital stay completely through day 60. After that, coinsurance kicks in at $434 daily for days 61 through 90. If your hospitalization extends into your 60 lifetime reserve days, you’ll pay $868 per day. Most people never use reserve days, but someone recovering from a stroke or major surgery that requires three months of hospitalization absolutely will face these costs.

Skilled Nursing Facility Expenses

Skilled nursing facility care follows a different cost structure than hospital stays. Part A covers days one through 20 completely after a qualifying hospital stay, then you pay $217 daily for days 21 through 100 in 2026. The trap many people miss is that you must have spent at least three consecutive days in the hospital to qualify for SNF coverage at all, and you must enter the facility within 30 days of discharge. Those 21 to 100 days add up quickly-someone spending 80 days in a facility pays $12,920 in coinsurance alone.

Hospice and Home Health Coverage

Hospice and home health services work differently because Part A typically covers them at no cost to you beyond your Part B premium, assuming your doctor orders them and they’re medically necessary rather than custodial. This distinction matters significantly when you’re facing end-of-life care or recovery at home.

Predicting Your Annual Out-of-Pocket Costs

Your total Part A costs depend heavily on how much inpatient care you actually need, which makes annual predictions almost impossible. Someone who stays healthy might pay only the $1,736 deductible once a year or not at all, while someone managing heart disease or recovering from surgery could face multiple hospital stays, SNF stays, and substantial coinsurance bills.

The Centers for Medicare & Medicaid Services publishes utilization data showing that skilled nursing facility care represents a major portion of Part A spending, yet most people dramatically underestimate how expensive those 21 to 100 days become when coinsurance applies. If you face a diagnosis like cancer, heart disease, or joint replacement, planning for potential SNF costs makes sense.

Final Thoughts

Medicare Part A overview fundamentals rest on three core realities: eligibility, coverage scope, and out-of-pocket costs. About 99% of people 65 and older qualify for premium-free Part A through their work history, while those who fall short can purchase coverage for $311 to $565 monthly. Disability and serious medical conditions like ALS or End-Stage Renal Disease create earlier pathways to coverage, protecting people facing health crises from unnecessary delays.

Your actual costs depend entirely on the inpatient care you need. A $1,736 deductible per hospital admission in 2026 affects most people minimally, but skilled nursing facility coinsurance at $217 daily for days 21 through 100 escalates quickly during extended recovery. The enrollment window matters more than most people realize-missing your Initial Enrollment Period at 65 triggers a Late Enrollment Penalty of up to 10% annually for the rest of your life.

We at Dave Silver Insurance help people navigate these decisions with personalized guidance tailored to your specific health and financial situation. Contact Dave Silver Insurance to clarify your options and confirm you’re enrolled correctly for your healthcare needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation