Medicare covers a lot, but dental care isn’t one of them. Most seniors face significant out-of-pocket costs for basic procedures like cleanings, fillings, and root canals.

Supplemental dental insurance for seniors on Medicare fills these gaps and protects your wallet. We at Dave Silver Insurance help seniors understand their options so they can make informed decisions about their dental coverage.

What Dental Services Does Medicare Actually Cover?

Original Medicare Part A and Part B do not cover routine dental care. Cleanings, exams, fillings, dentures, and root canals remain your financial responsibility. Medicare.gov states clearly: if your dentist bills for routine care, you pay 100 percent out of pocket. The only exceptions are extremely narrow. Medicare covers dental services only when they occur during a hospital inpatient stay for a procedure linked to a medical condition-such as an oral exam before a heart valve replacement or tooth extraction before cancer treatment. For end-stage renal disease patients, Medicare may cover oral exams required before dialysis. These situations are rare and do not apply to most seniors.

The reality hits hard: 65 percent of Medicare beneficiaries lack any dental coverage at all, according to data from SeniorLiving.org. This gap creates serious financial exposure.

The Dental Procedures That Hit Your Wallet Hardest

Seniors need dental care more than younger populations, yet they face the steepest costs. Gum disease affects 68 percent of Americans aged 65 and older, and dry mouth affects 30 percent-both conditions require professional treatment. Dentures represent one of the biggest expenses, ranging from $1,050 to $2,300 for a lower denture and $1,100 to $2,500 for an upper denture, according to Delta Dental’s cost data. Periodontal cleanings cost $120 to $200, while scaling and root planing runs $210 to $330 per section.

Crowns, bridges, and implants push costs even higher. Without supplemental coverage, a single crown can cost $900 to $2,000 out of your retirement savings. Nineteen percent of Medicare beneficiaries spent more than $1,000 annually on dental care, according to SeniorLiving.org data. More than one in four seniors have not visited a dentist in five years, largely because they cannot afford it without insurance.

Why Waiting Without Coverage Costs More

Postponing dental treatment creates compounding problems. A small cavity that costs $150 to fill today becomes a root canal costing $1,000 or more if ignored. Untreated gum disease leads to tooth loss, forcing denture replacement and additional surgeries. Seniors with untreated dental infections face complications before medical procedures like chemotherapy or organ transplants. The financial penalty for going without supplemental dental insurance extends beyond the immediate procedure cost. Your overall health suffers, increasing medical expenses elsewhere. Dry mouth from medications, common in seniors, accelerates tooth decay and gum disease without preventive care. Supplemental dental insurance typically costs $20 to $100 monthly with deductibles of $50 to $150 yearly, making the math straightforward: prevention through coverage costs far less than emergency treatment or living with dental pain and infection.

Understanding what Medicare won’t pay for is only half the battle. The next step involves exploring the supplemental dental insurance options available to you and how these plans actually work to fill those coverage gaps.

How Supplemental Dental Plans Actually Work

Supplemental dental insurance operates separately from Medicare and fills the gaps that Original Medicare leaves wide open. When you purchase a standalone dental plan, you pay a monthly premium-typically $20 to $100 according to SeniorLiving.org data-and access covered dental services through the plan’s network of providers. You visit an in-network dentist, the dentist bills your plan, and you pay only your portion of the cost. Out-of-network visits exist but cost significantly more, which is why network size matters. Spirit Dental & Vision operates a network of approximately 136,000 providers, while Mutual of Omaha boasts over 400,000 in-network locations, giving you real options for finding nearby dentists.

Coverage Levels and What You Actually Pay

Most plans cover preventive care at 100 percent-exams, cleanings, and X-rays cost you nothing after you meet any deductible, which typically runs $50 to $150 yearly or sometimes zero. Basic procedures like fillings and root canals receive partial coverage, usually around 80 percent. Major services such as crowns, bridges, and implants are covered at approximately 50 percent, meaning you still absorb significant costs for expensive work. Annual maximums cap your plan’s spending, and this number matters enormously for your budget planning. Spirit Dental and Mutual of Omaha both offer up to $5,000 annual maximums, while Aetna’s core plans max out at $1,000 to $1,250.

Waiting Periods: The Hidden Barrier to Coverage

Waiting periods determine whether you can access coverage when you need it most. Some insurers like Aetna require a full year before covering crowns or dentures, meaning you cannot file a claim for those services within twelve months of enrollment. This delay creates a false economy-you pay premiums while unable to use the coverage for procedures you actually need. Spirit Dental removes this barrier almost entirely, covering most services immediately upon enrollment with no waiting period. Mutual of Omaha similarly offers no waiting periods and guarantees acceptance regardless of health history, eliminating the underwriting delays that plague other carriers. If you already know you need a crown or denture soon, these zero-waiting-period plans deliver real value that plans with 12-month delays simply cannot match.

Enrollment and Eligibility Work Differently Than Medicare

Enrollment happens outside the standard Medicare Annual Enrollment Period, meaning you can purchase supplemental dental coverage whenever you want throughout the year. You do not need to wait for October 15 to December 7 to sign up. This flexibility matters because dental emergencies do not follow Medicare’s calendar. Eligibility is generally straightforward-you must be a Medicare beneficiary, typically aged 65 or older, though some plans accept younger disabled Medicare recipients. No medical underwriting exists for most plans; Spirit Dental guarantees acceptance, and Mutual of Omaha accepts all applicants without health questions. This contrasts sharply with Medigap supplemental insurance, which must cover all your pre-existing health conditions and can’t charge you more for past or present health problems. For seniors with significant dental history or health complications, guaranteed-issue dental plans remove rejection risk entirely.

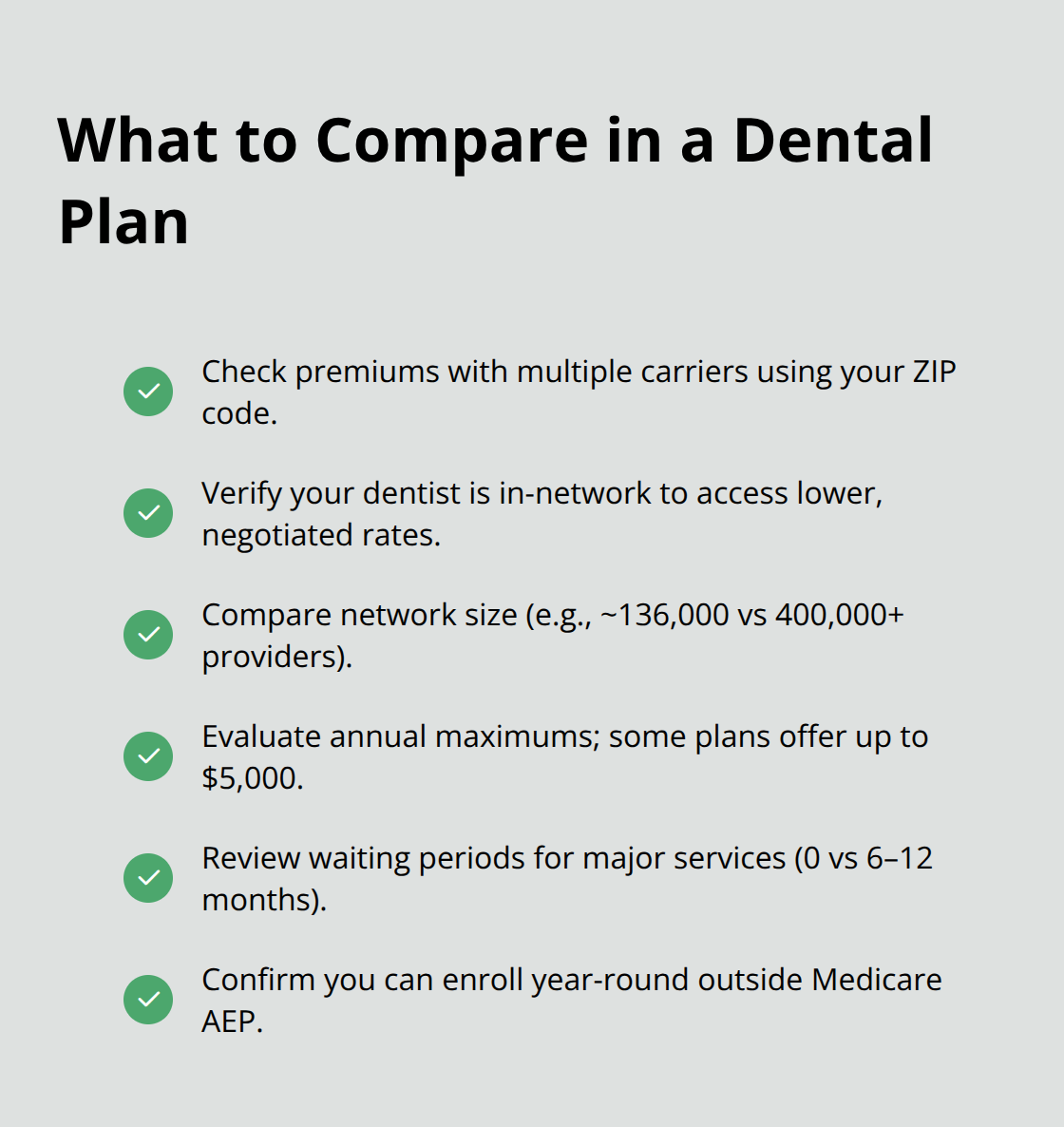

Finding the Right Plan for Your Situation

Network size and provider availability directly impact your out-of-pocket costs and convenience. A plan with 400,000+ providers (like Mutual of Omaha) gives you far more flexibility than a smaller network, especially if you travel or live in rural areas. Check whether your current dentist participates in the plan’s network before you enroll-switching providers mid-treatment creates headaches and potential gaps in care. Premium costs vary by state and age, but comparing quotes across multiple carriers reveals significant differences. A plan costing $23 monthly in one market might cost $35 in another, so enter your ZIP code with several insurers to see actual pricing. Your personal dental health needs should drive your plan selection. If you need dentures or major work soon, prioritize plans with no waiting periods and higher annual maximums. If you only need routine cleanings and occasional fillings, a lower-premium plan with solid preventive coverage may suffice.

Understanding how these plans work positions you to make a smart choice, but the real decision comes next: comparing specific plans side by side and evaluating which option aligns with your health needs and budget constraints.

Choosing the Right Dental Plan for Your Budget and Health Needs

Selecting a dental plan requires comparing three concrete factors: what you pay monthly, where you can go for treatment, and whether the coverage matches your specific dental situation. Start by entering your ZIP code with at least three different carriers to see actual premium quotes in your area. Spirit Dental might cost $23.45 monthly in one state but $35 in another, so generic pricing means nothing for your decision. Mutual of Omaha, Aetna, Cigna, and Humana all operate different networks and charge different rates by location.

Get quotes from each before deciding. The premium difference between carriers often reaches $15 to $20 monthly, which compounds to $180 to $240 yearly-money that could cover a cleaning or two if spent wisely.

Verify Your Dentist Participates in the Network

Once you have premium numbers, verify whether your current dentist participates in each plan’s network. Calling your dentist’s office takes five minutes and saves you from enrollment regret. An in-network dentist means you access negotiated rates that reduce your out-of-pocket costs significantly compared to out-of-network providers who charge full fees. If your dentist isn’t in-network with your preferred plan, either switch plans or accept higher costs for staying with that provider. Network size and provider availability directly impact your out-of-pocket costs and convenience. A plan with 400,000+ providers (like Mutual of Omaha) gives you far more flexibility than a smaller network, especially if you travel or live in rural areas.

Annual Maximums Determine Your Spending Limit

Annual maximums cap how much the insurance company will pay for your dental care each calendar year, and this number should align with your anticipated treatment needs. If you need significant work like multiple crowns or dentures, higher maximum plans deliver substantially better value even if the monthly premium costs slightly more. Calculate the real math: a $30 monthly premium ($360 yearly) for a plan with a $5,000 maximum beats a $20 monthly premium ($240 yearly) for a plan with a $1,000 maximum if you require $3,000 in dental work. The lower-premium plan forces you to cover the remaining $2,000 out of pocket, while the higher-premium plan limits your exposure to copays and deductibles. Review your dental history from the past three years-how much have you actually spent on dental care? If you average $1,500 yearly, a $1,250 maximum plan leaves you short. If you average $500 yearly, paying extra for a $5,000 maximum wastes money on coverage you won’t use.

Waiting Periods Create Real Barriers to Immediate Coverage

This is where your personal timeline matters enormously. If you already know you need a crown, denture, or implant within the next six months, plans with 6 to 12-month waiting periods for major services become nearly worthless. You pay premiums while unable to claim benefits for the exact procedures you need. Spirit Dental’s zero waiting period on most services and Mutual of Omaha’s immediate coverage eliminate this problem entirely, making them objectively better choices if you have urgent dental needs. However, if you only need preventive care and routine cleanings for the next year, a plan with waiting periods on major services costs less monthly because you won’t access those benefits anyway. The strategic decision hinges on honesty about your budget constraints and health status. Schedule a checkup with your dentist before enrolling in a plan if you haven’t seen one recently-knowing what work you actually need prevents purchasing the wrong coverage level.

Final Thoughts

Supplemental dental insurance for seniors on Medicare protects your retirement from the financial shock of unexpected dental costs. The numbers tell the story: 65 percent of Medicare beneficiaries lack dental coverage, leaving them exposed to bills that drain savings fast. A single crown costs $900 to $2,000, dentures run $1,050 to $2,500, and waiting only multiplies expenses when small problems become major procedures requiring emergency treatment.

Your next step requires action on three fronts. Enter your ZIP code with at least three carriers-Spirit Dental, Mutual of Omaha, Aetna, Cigna, and Humana all operate in most states-and compare actual premium quotes for your area. Verify whether your current dentist participates in each plan’s network, review the annual maximum and waiting periods against your personal dental needs, and select coverage that matches your situation.

The complexity of Medicare planning extends beyond dental coverage alone, and coordinating supplemental dental insurance with Medigap policies, Medicare Advantage plans, and prescription drug coverage requires expertise. Contact Dave Silver Insurance to receive personalized guidance on your complete Medicare picture and move forward with a dental coverage plan that protects both your health and your wallet.