Medicare Part A late enrollment penalties can cost you hundreds of dollars annually for life. Missing enrollment deadlines happens more often than most people realize.

We at Dave Silver Insurance see clients facing these avoidable penalties every month. The good news is that understanding the rules and timing can save you significant money.

What Are Medicare Part A Late Enrollment Penalties

Medicare penalties strike your wallet hard and remain permanent. The penalty equals 10% of your monthly premium for each 12-month period you delay enrollment without creditable coverage. Most people qualify for premium-free Part A, but those who don’t face monthly premiums based on their work credits and income levels.

Who Pays These Penalties

The penalty applies to anyone who doesn’t enroll during their Initial Enrollment Period and lacks qualifying employer coverage or other creditable insurance. Workers with fewer than 40 work credits get hit the hardest since they pay premiums plus penalties. The penalty duration equals twice the number of years you could have enrolled but didn’t. Wait three years to enroll, and you’ll pay penalties for six years.

Real Cost Examples

Consider someone with limited work credits who delays enrollment for two years. Their base premium varies based on work history, and the 20% penalty adds significant monthly costs. Over six years of penalty payments, these additional charges accumulate substantially. The math gets worse for those with minimal work credits who face higher premium rates. These penalties compound quickly and never disappear once applied to your coverage.

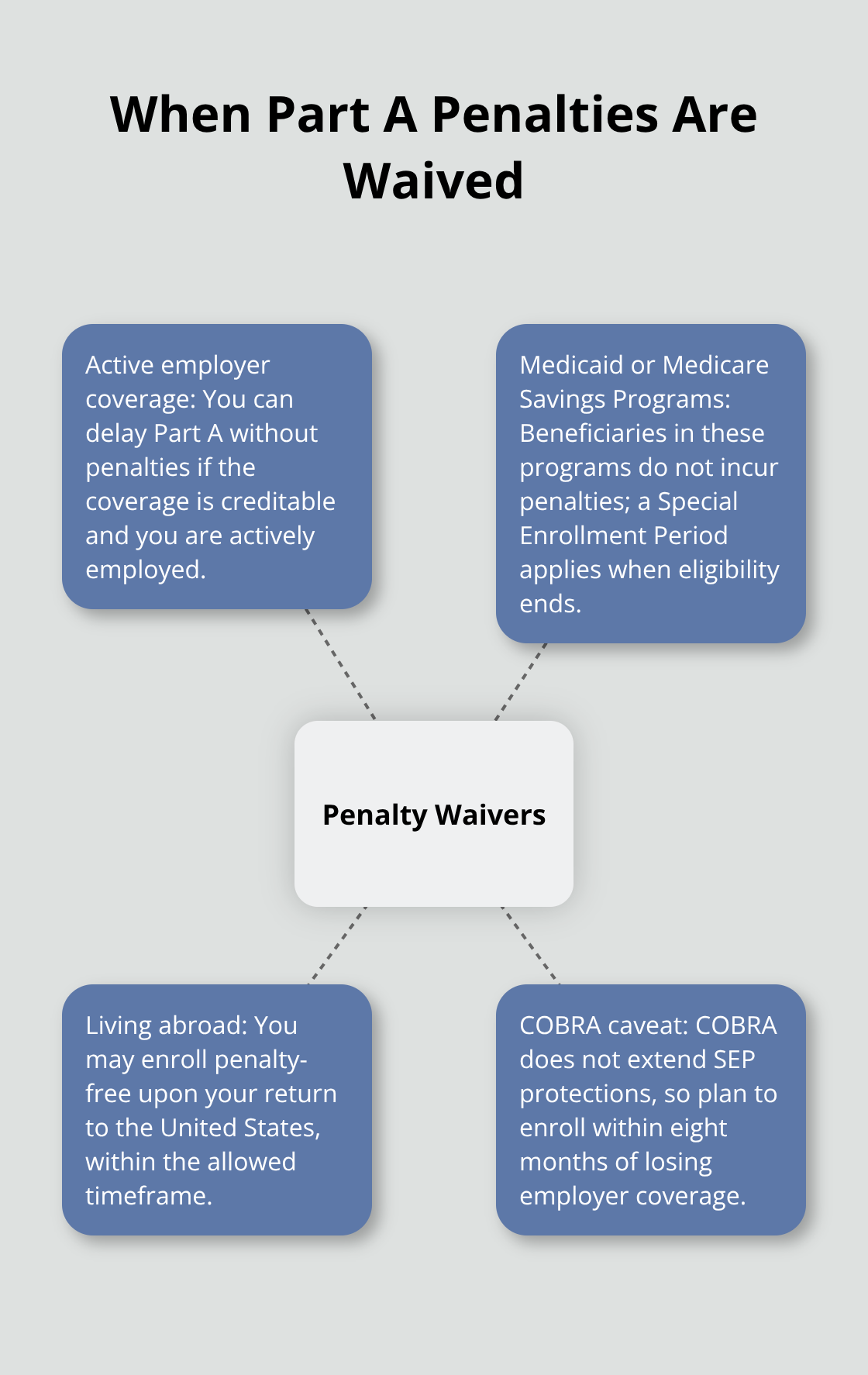

Special Circumstances That Waive Penalties

Active employment with group health coverage protects you from penalties through Special Enrollment Periods. Medicaid recipients and those in Medicare Savings Programs avoid penalties entirely. People who live outside the United States also gain penalty-free enrollment upon return. However, COBRA continuation coverage doesn’t extend these protections, which leaves many vulnerable to unexpected penalty charges when their coverage ends.

These penalty rules create complex situations that many people face when they transition between different types of health coverage.

Common Situations That Lead to Late Enrollment

Employer-sponsored health coverage creates the most dangerous enrollment trap people face. Workers approaching 65 often assume their job-based insurance eliminates the need for Medicare enrollment entirely. This misconception leads to costly penalties when they retire or lose coverage later.

The Centers for Medicare & Medicaid Services reports that Special Enrollment Periods allow changes to Medicare coverage due to life events like moving, losing coverage, or other exceptional situations, but this protection vanishes the moment employment ends. Workers must enroll within eight months of losing employer coverage to avoid penalties, yet many discover this requirement too late.

The Automatic Enrollment Myth

Social Security recipients receive automatic Part A enrollment at 65, but millions of Americans don’t collect Social Security benefits yet. These individuals must actively enroll during their seven-month Initial Enrollment Period (three months before their 65th birthday, their birthday month, and three months after) or face penalties. The Social Security Administration confirms that people who delay retirement benefits past 65 remain responsible for Medicare enrollment decisions. Workers who continue earning past 65 frequently miss this distinction and assume their delayed Social Security filing also delays Medicare requirements. This assumption costs them dearly when penalties accumulate during the gap between eligibility and enrollment.

Coverage Gaps After Job Loss

COBRA continuation coverage provides temporary insurance but doesn’t extend Medicare enrollment protections. When COBRA expires, former employees face immediate enrollment pressure without Special Enrollment Period benefits. The Department of Labor data shows COBRA typically lasts 18 to 36 months, creating dangerous timing scenarios for older workers. People who lose jobs at 63 or 64 often exhaust COBRA benefits after reaching Medicare eligibility and scramble to enroll during General Enrollment Periods from January through March. This timing forces them to wait months for coverage while accumulating penalty charges that will follow them throughout their Medicare years.

Misinformation About Work Credits

Many people believe they need 40 work credits to qualify for any Medicare benefits, but Part A eligibility differs from premium-free status. Workers with fewer than 40 credits can still enroll in Part A but pay monthly premiums based on their work history. Those with 30-39 quarters of coverage pay $278 monthly in 2024, while those with fewer than 30 quarters pay $505 monthly. These premium-paying enrollees face the same late enrollment penalties as premium-free beneficiaries, making timely enrollment even more important for their financial well-being.

Understanding these common pitfalls helps you recognize the specific strategies needed to protect yourself from Medicare Part A penalties.

How Can You Prevent Medicare Part A Penalties

Mark Your Calendar Three Months Early

Your Initial Enrollment Period starts three months before your 65th birthday and extends three months after. The Social Security Administration processes applications faster when you apply during the first three months rather than wait until your birthday month. Set calendar reminders at least six months before you turn 65 to research your options thoroughly.

Workers still employed at 65 must decide whether to enroll immediately or delay enrollment while they maintain employer coverage. Document your employment status and insurance details before you make this decision, as the Social Security Administration requires proof of active coverage to justify delayed enrollment.

Master Special Enrollment Period Rules

Employment-based coverage triggers an eight-month Special Enrollment Period that provides an opportunity for individuals who experience certain life changes or qualifying life events to enroll in or change coverage. The Centers for Medicare & Medicaid Services allows this protection only while you remain actively employed with creditable coverage that meets Medicare standards.

COBRA continuation coverage does not extend this protection period (which creates a dangerous gap for many retirees). Workers who lose employer coverage must track their termination date precisely and enroll within eight months to avoid penalties. Medicaid recipients qualify for Special Enrollment Periods when their Medicaid ends, but they must act quickly once they receive termination notice.

People who return to the United States after they live abroad also receive Special Enrollment Period benefits, but only for a limited time after they reestablish residency.

Keep Detailed Coverage Records

Maintain written documentation of all health insurance coverage from age 65 forward, which includes employer plan details, coverage dates, and termination notices. The Social Security Administration may request this documentation years later when you apply for Medicare benefits. Store copies of insurance cards, benefits summaries, and employment verification letters in a dedicated Medicare file.

Workers with complex employment histories need especially detailed records to prove continuous creditable coverage. Document any gaps in coverage immediately and research whether those gaps qualify for penalty exemptions. Insurance companies and employers sometimes provide inadequate documentation, so request formal letters that confirm your coverage status and dates before you leave any job or change insurance plans.

Navigate General Enrollment Periods Wisely

The General Enrollment Period runs from January 1 to March 31 each year for people who missed their initial enrollment opportunities. Coverage begins the following month (April), which means you face months without coverage if you miss earlier enrollment windows. This period forces you to pay penalties that accumulate during the gap between eligibility and enrollment.

Planning ahead and understanding Medicare enrollment characteristics helps you avoid penalty charges once they apply. The penalty calculation includes all months you were eligible but not enrolled, regardless of when you finally sign up.

Final Thoughts

Medicare Part A late enrollment penalty prevention demands proactive action and precise timing. You must track your Initial Enrollment Period six months before your 65th birthday and document all employer coverage details. Workers who maintain job-based insurance must understand Special Enrollment Period rules and act within eight months of coverage loss.

Professional Medicare guidance proves valuable when you face complex employment situations, have limited work credits, or navigate coverage transitions. The penalty calculations and enrollment rules create financial risks that compound over time (making early action essential). These penalties accumulate quickly and remain permanent once applied to your coverage.

We at Dave Silver Insurance help clients avoid these costly penalties through personalized Medicare enrollment guidance. Our expertise covers all Medicare parts and Medigap options, with accessibility for urgent enrollment questions. Schedule a consultation to gain clarity and confidence in your Medicare enrollment decisions before penalties accumulate.