Missing a Medicare Advantage enrollment deadline can lock you out of coverage for an entire year. The three enrollment periods for Medicare Advantage each serve different purposes, and knowing which one applies to you makes all the difference.

At Dave Silver Insurance, we’ve helped countless people navigate these windows without costly mistakes. This guide walks you through every deadline you need to know.

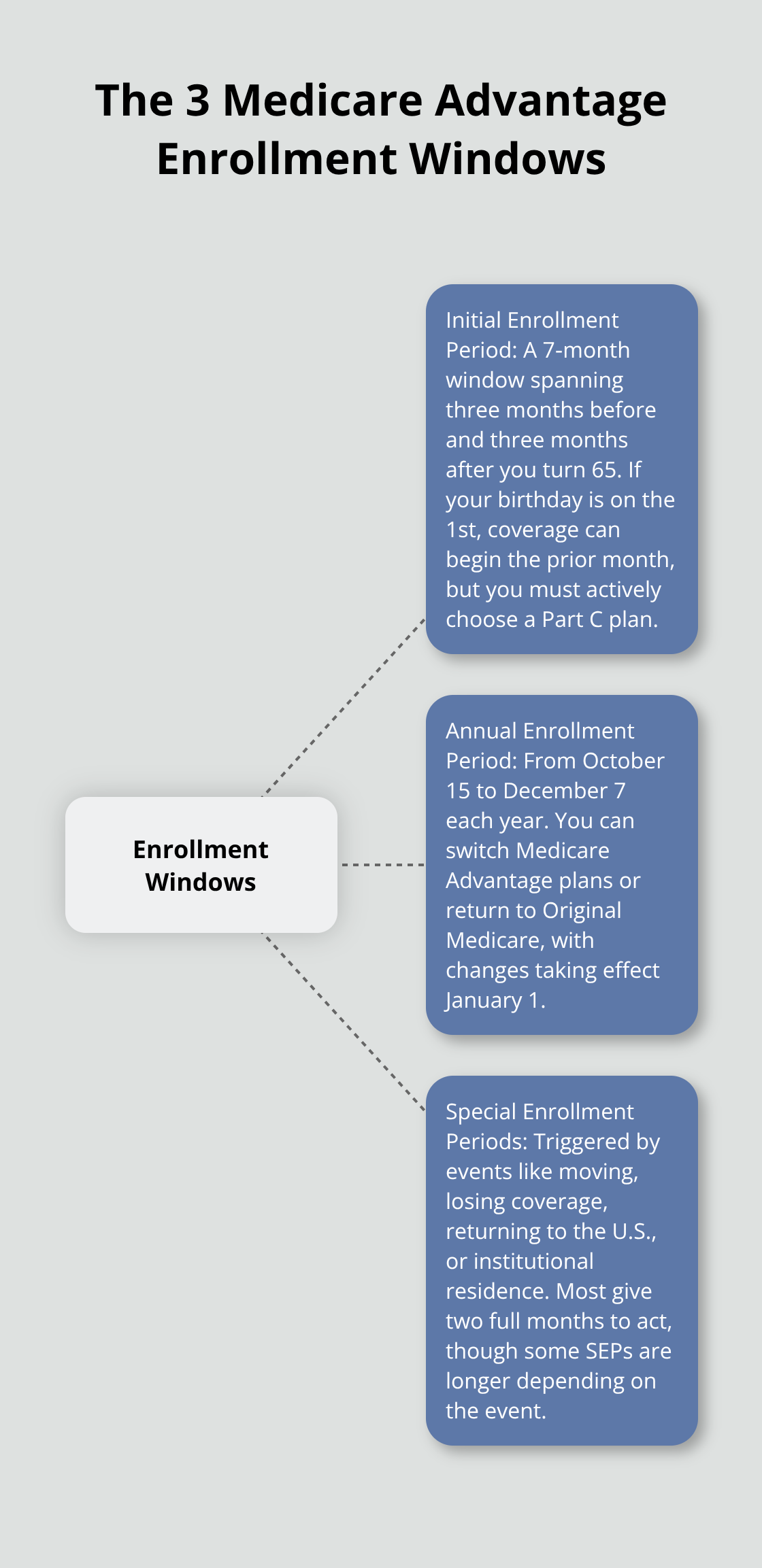

Three Enrollment Windows That Matter

Your Initial Enrollment Period: A Seven-Month Window Around Age 65

The Initial Enrollment Period starts three months before you turn 65 and ends three months after, giving you a seven-month window to enroll in Medicare Advantage. If your birthday falls on the first of the month, your coverage can start the month before you turn 65.

Most people who already receive Social Security benefits get automatically enrolled in Original Medicare Parts A and B when they turn 65, but you still need to actively choose a Medicare Advantage plan during this window if you want Part C coverage. The stakes are high: missing this deadline triggers a late enrollment penalty that increases the longer you wait, and this penalty stays with you permanently as long as you have Part B. If you turn 65 in March, your Initial Enrollment Period runs from December through June, which means you have time to research plans without rushing.

The Annual Enrollment Period Resets Your Coverage Each Year

From October 15 through December 7 each year, you get another chance to switch Medicare Advantage plans or move back to Original Medicare. This annual window is more restrictive than your Initial Enrollment Period because you can only switch to a different Medicare Advantage plan or return to Original Medicare, not enroll in one for the first time. Changes made during this period take effect January 1, so if you switch plans in November, your new coverage starts on New Year’s Day. If you’re happy with your current plan, it automatically renews on January 1 unless you actively make a change. Many people miss this window because they assume their plan will stay the same, but plan benefits and networks change annually, so reviewing your options during October and November protects you from unexpected coverage gaps.

Special Enrollment Periods Respond to Life Changes

Qualifying life events open Special Enrollment Periods that let you enroll or switch plans outside the regular windows. Moving to a new address outside your plan’s service area gives you two full months to switch plans, starting from when you notify your plan or from the move date itself. Losing other health or prescription coverage-whether from an employer or Medicaid-triggers a two-month window to enroll in Medicare Advantage without penalties. Returning to the United States after living abroad also qualifies, giving you two full months to join a plan. If you live in an institution like a nursing home, you can make changes whenever you’re there, plus two full months after you move out. The Medicare Rights Center emphasizes that documentation may be required to prove your SEP eligibility, so you should gather proof of your life event before contacting plans. These periods exist specifically to prevent people from losing coverage due to circumstances beyond their control, making them invaluable for those who experience major life changes.

What Happens When Life Events Trigger Your Options

Beyond moving and losing coverage, other life events open enrollment windows. If you get released from incarceration, you have 12 months after the month of release to enroll in Medicare Advantage. Losing Medicaid or Extra Help benefits gives you three full months from the date you’re no longer eligible to make changes. If a plan makes an error or provides inaccurate information, you have two full months after you receive notice to switch to a different plan. These Special Enrollment Periods (SEPs) vary in length and scope depending on your situation, so understanding which event applies to you determines how much time you actually have to act. The window closes once you miss it, so identifying your specific SEP early prevents you from losing your opportunity to change coverage without penalties.

What Happens When You Miss an Enrollment Deadline

The Cost of Missing Your Initial Enrollment Period

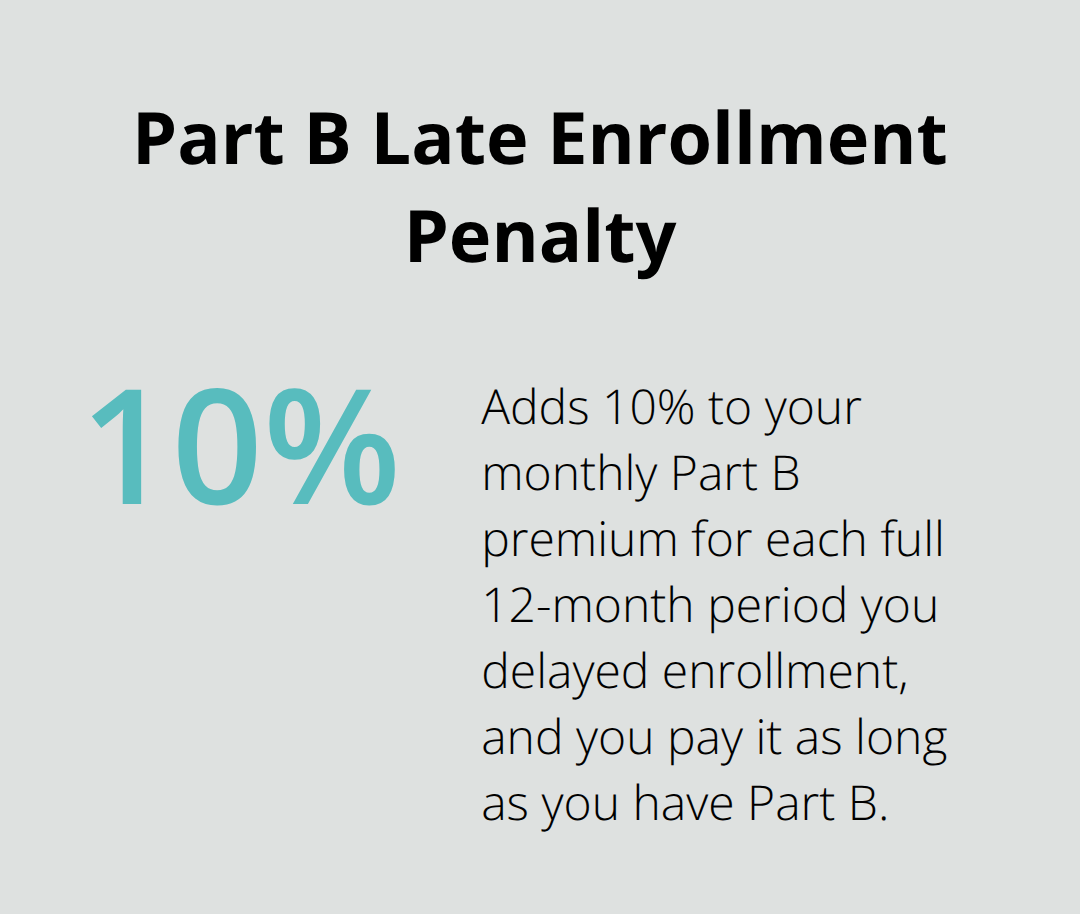

Missing your Initial Enrollment Period costs you permanently. According to Medicare.gov, the late enrollment penalty for Part B adds 10% to your monthly premium for each full 12-month period you waited to sign up, and you’ll pay it for as long as you have Part B coverage. This is why acting within your seven-month Initial Enrollment Period around age 65 matters so much. The penalty applies whether you turn 65 and delay intentionally or simply forget the deadline exists.

Once you’re locked into that higher premium, switching plans later won’t erase it.

The only way to avoid this trap is understanding exactly when your window opens and closes. If you turn 65 in September, your Initial Enrollment Period begins in June and ends in December. If you turn 65 on the first of the month, your coverage can start one month earlier, giving you slightly more breathing room. Write these dates down immediately rather than relying on memory. Many people assume Social Security will notify them automatically, but Social Security only handles Parts A and B enrollment for those already receiving benefits. Medicare Advantage requires your active choice, separate from any automatic enrollment.

Creating a System to Track Your Enrollment Windows

Tracking enrollment deadlines throughout the year requires a specific system because three different windows apply depending on your situation. The Annual Enrollment Period from October 15 to December 7 affects everyone already in a Medicare plan, and changes take effect January 1. Set a calendar reminder for October 1 to review your current plan’s benefits, network changes, and prescription drug coverage before the October 15 start date. If you’re in a Special Enrollment Period due to a life event, your window is typically two to three months, so document your event immediately and contact your plan within days rather than weeks.

The Medicare Rights Center notes that documentation proving your life event is required, so gather proof of moving, job loss, or coverage changes before calling plans. Don’t assume verbal notification counts; get written confirmation that your plan received your enrollment request. Coverage typically starts the first day of the month after enrollment, so enrolling on October 20 means coverage begins November 1. This timing matters for medication refills and doctor appointments.

Understanding State-Specific Enrollment Rules

Medicare Advantage plans themselves vary by state and even by county within states, but the federal enrollment periods apply uniformly across all 50 states. However, some states offer additional programs like Medicaid-Medicare coordination that create extra enrollment opportunities. Contact your state’s Health Insurance Assistance Program to learn whether additional state programs affect your timeline. The key distinction is that while enrollment deadlines are federal and identical nationwide, which plans are actually available to you depends entirely on your ZIP code and state residence. This variation means your next step involves researching which specific plans operate in your area and what each one covers.

How to Pick a Medicare Advantage Plan That Actually Covers What You Need

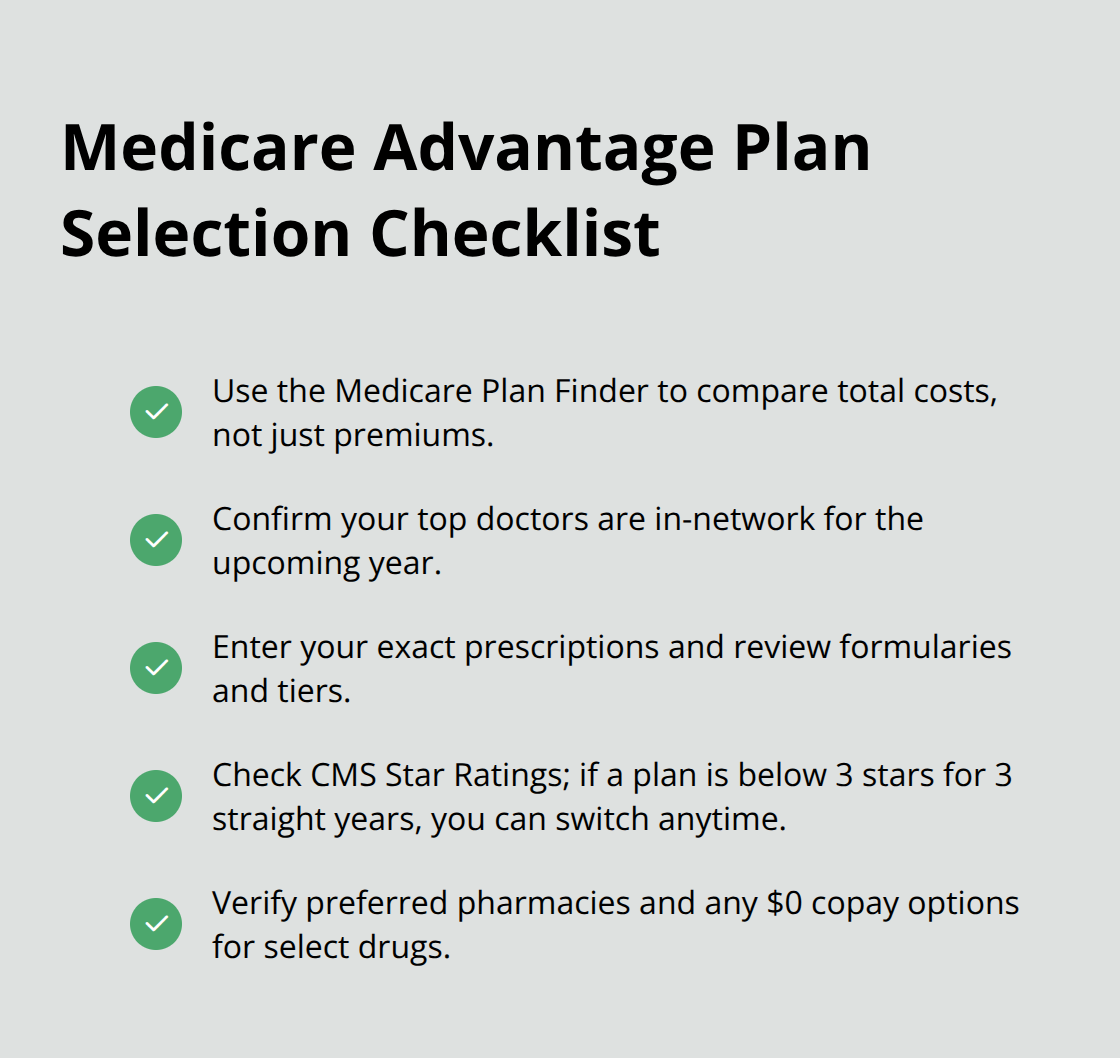

Use the Medicare Plan Finder to Compare Real Costs

The Medicare Plan Finder tool at Medicare.gov lets you enter your current prescriptions to see estimated monthly and yearly drug costs for each plan in your area. This single step provides the most practical information you can gather before enrolling. Don’t focus only on the premium; out-of-pocket maximums matter far more if you have chronic conditions. A plan with a $0 premium but a $7,000 out-of-pocket maximum costs significantly more than a $50 monthly premium plan with a $4,000 maximum if you need regular specialist visits or medications.

Verify Your Doctors and Pharmacies Are Actually In-Network

Call the plans directly and ask whether your three most important doctors participate in their network before you enroll, because switching networks mid-year creates real disruption. Medicare Advantage plans change their networks annually, so a doctor who was in-network last year might not be this year; verify coverage for the upcoming year specifically, not past coverage.

Prescription drug formularies also shift yearly, meaning your current medication might move to a higher tier or disappear entirely. Enter your exact medications into the Plan Finder tool to see not just whether they’re covered but which tier they fall into, because a tier 4 drug costs far more than a tier 1 generic. Some plans offer zero-dollar copays for certain medications if you use their preferred pharmacy, so confirm which pharmacy chains participate in each plan you’re considering.

Check Star Ratings and Plan Performance Data

Plans with four or five stars according to the CMS Star Ratings system generally outperform lower-rated plans on service quality and customer satisfaction, so check star ratings on Medicare.gov for independent performance data beyond marketing claims. If your current plan has fallen below three stars for three consecutive years, you can switch anytime, which signals that performance has genuinely declined. This rating system provides concrete evidence of how well plans actually serve their members rather than relying on promotional materials.

Act During Your Enrollment Window to Switch Plans

Understanding when to switch plans requires honest assessment of your current situation rather than hoping things stay the same. If your doctor dropped out of your plan’s network or your medication moved to a more expensive tier, the Annual Enrollment Period from October 15 to December 7 is your moment to switch without penalty. Don’t wait until January when your new coverage starts; switching in November gives you time to confirm your new plan’s details and notify your pharmacy of any formulary changes. If you qualify for a Special Enrollment Period due to moving, losing coverage, or another life event, act within your window because waiting costs you months of potentially inadequate coverage.

Final Thoughts

The three enrollment periods for Medicare Advantage each serve a specific purpose, and understanding which one applies to your situation determines whether you pay penalties or maintain seamless coverage. Your Initial Enrollment Period around age 65 gives you seven months to act, the Annual Enrollment Period from October 15 to December 7 lets you adjust coverage yearly, and Special Enrollment Periods respond to life changes like moving or losing coverage. Missing these windows costs real money through permanent late enrollment penalties and coverage gaps that disrupt your healthcare.

Before your enrollment window closes, take three concrete steps. First, write down your specific deadline based on when you turn 65 or when your life event occurs. Second, use the Medicare Plan Finder to compare plans in your area and verify your doctors and medications are covered. Third, contact your chosen plan and confirm your enrollment request was received in writing.

We at Dave Silver Insurance understand that Medicare enrollment feels overwhelming because the rules genuinely are complex. Our team has spent over 17 years helping people navigate these exact decisions, and we remain accessible seven days a week to answer your questions. Whether you need guidance on which of the three enrollment periods for Medicare Advantage applies to you, help comparing Medicare Advantage plans against Medigap options, or clarification on how late enrollment penalties work, our personalized approach ensures you understand your choices before committing. Schedule a consultation with us to get expert advice tailored to your health and financial situation.