Medicare can feel overwhelming when you’re trying to figure out which parts cover what. We at Dave Silver Insurance know that understanding Medicare Part A, B, C, and D coverage is the first step toward making smart healthcare decisions.

This guide breaks down each part so you know exactly what’s covered, what you’ll pay, and where the gaps are. By the end, you’ll have the clarity you need to choose the right coverage for your situation.

What Part A and Part B Actually Cover

Original Medicare splits into two distinct parts, and understanding what each covers matters before you consider Part C or Part D. Part A is hospital insurance, covering inpatient hospital stays, skilled nursing facility care for up to 100 days, hospice care, and some home health services. Part B is medical insurance, covering doctor visits, outpatient care, preventive services like screenings and vaccines, and durable medical equipment such as wheelchairs or oxygen tanks. According to Medicare.gov, most people pay zero premium for Part A in 2026 if they’ve worked long enough, but Part B costs $202.90 per month whether you use it or not. This is a critical distinction: you cannot access Part A without enrolling in Part B, which means the Part B premium is non-negotiable if you want hospital coverage at all.

What You Actually Pay Under Part A and Part B

The financial picture gets complicated fast because deductibles and coinsurance vary dramatically by service type. Part A has a $1,736 deductible per benefit period, but once you meet it, your first 60 days in a hospital cost nothing. Days 61 through 90 cost $434 per day, and days 91 through 150 cost $868 per day. After 150 days, you pay everything out of pocket.

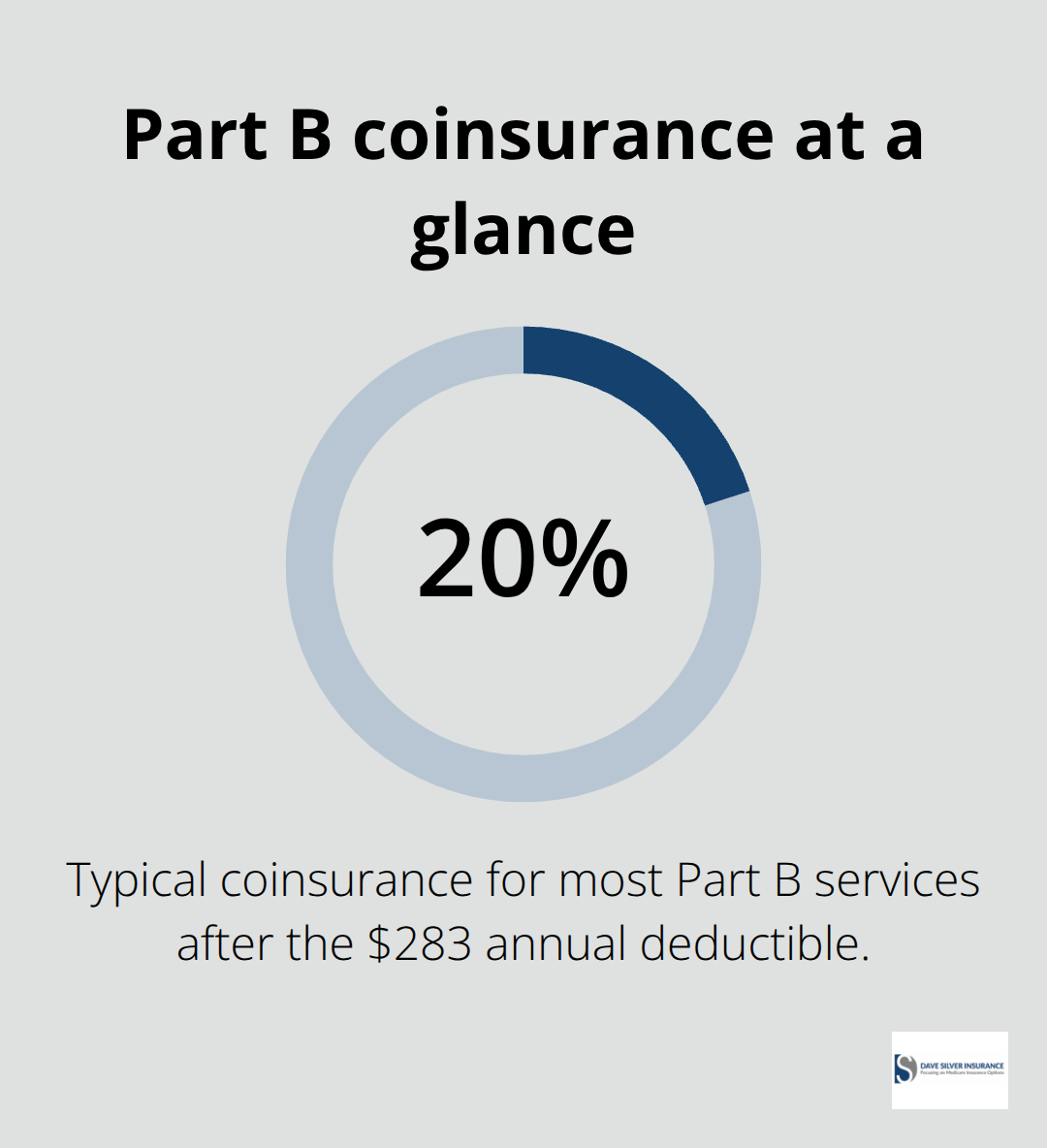

Skilled nursing facilities work differently: days 1 through 20 are free, but days 21 through 100 cost $217 per day. Home health care under Part A carries zero cost, and hospice care is also free for covered services. Part B operates on a different structure entirely. After you pay your $283 annual deductible, you typically owe 20 percent coinsurance for most services, though some preventive care like clinical laboratory services and depression screenings are completely free. A specialist visit might cost you $40 out of a $200 appointment if the Medicare-approved amount is $200.

The Real Financial Risk Nobody Talks About

Original Medicare has no yearly out-of-pocket limit, which is the single most dangerous aspect of Parts A and B combined. You could face unlimited costs if you have a serious illness or extended hospital stay. A 90-day hospitalization would cost you $434 per day for 30 days, totaling $13,020 in coinsurance alone, plus any additional medical services. Many people discover this gap only after a health crisis, which is why Medigap policies exist. However, the point here is clear: Parts A and B alone leave you exposed to catastrophic costs that could wipe out your savings.

Why Part C and Part D Change the Picture

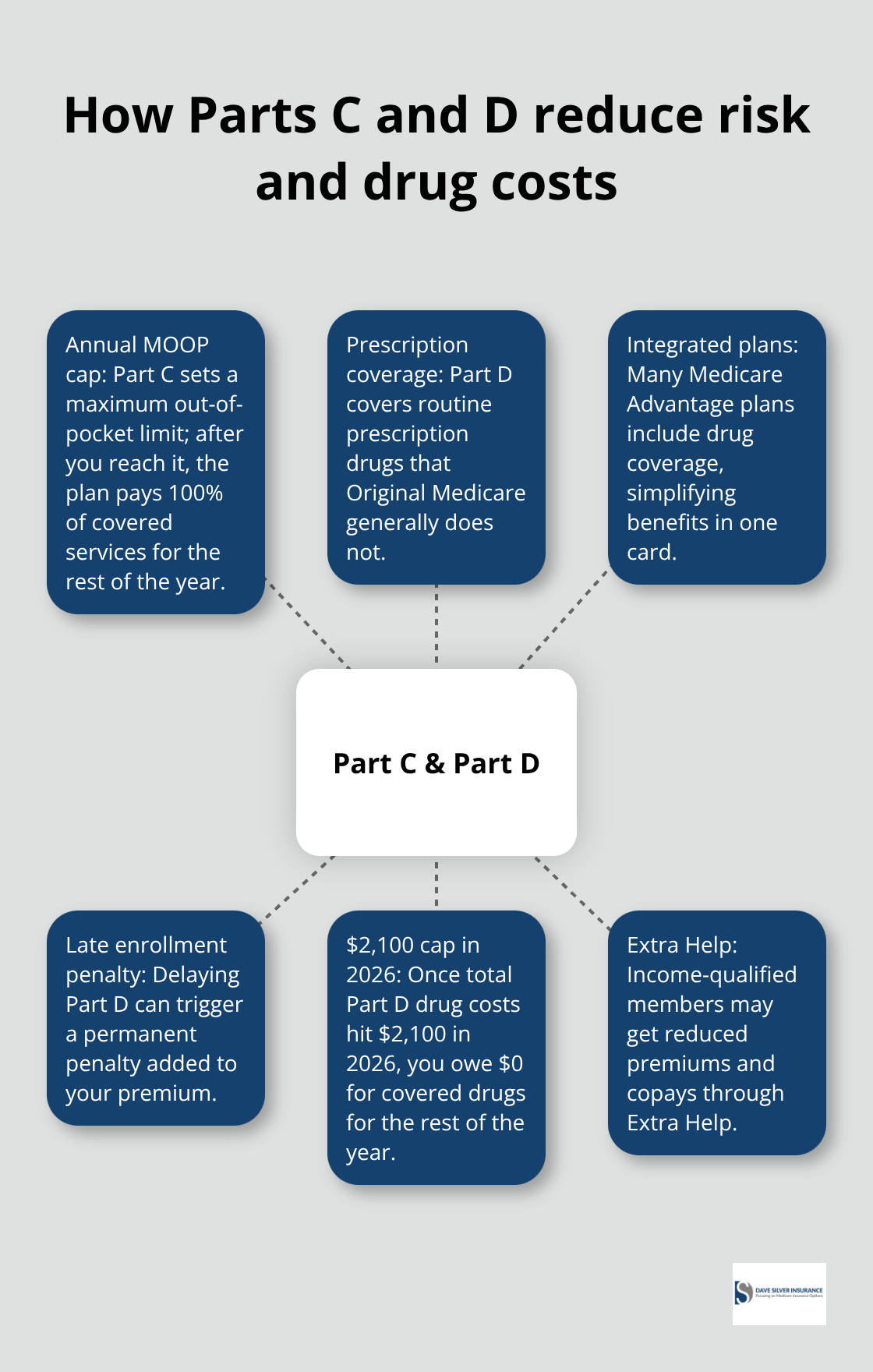

This exposure to unlimited costs is exactly why millions of Medicare beneficiaries turn to Part C (Medicare Advantage) or add Part D (prescription drug coverage) to their plans. Part C plans cap your annual out-of-pocket costs, meaning once you hit that limit, the plan pays 100 percent of covered services for the rest of the year. Part D addresses another gap entirely: Original Medicare does not cover most routine prescription drugs, leaving you to pay full price at the pharmacy. Understanding these gaps in Parts A and B sets the stage for evaluating whether Part C, Part D, or both make sense for your specific situation.

How Part C and Part D Solve Different Medicare Problems

Medicare Advantage Plans Cap Your Out-of-Pocket Costs

Medicare Advantage plans under Part C directly address the unlimited out-of-pocket exposure that Original Medicare creates. According to CMS data, roughly 34 million beneficiaries out of 67 million Medicare beneficiaries have chosen Part C, and that number keeps growing because these plans cap your annual out-of-pocket costs. Once you hit that limit, the plan pays 100 percent of covered services for the rest of the year, giving you predictability that Original Medicare never offers. The tradeoff is real though: you must use doctors and hospitals in the plan’s network, and your provider options shrink compared to Original Medicare’s freedom.

Verify Your Doctors and Medications Before You Enroll

Before you enroll in any Part C plan, verify that your preferred doctors and hospitals are in-network, because networks change annually and a plan you chose last year might exclude your cardiologist this year. Check the plan’s formulary to confirm your medications are covered and understand what you’ll pay at the pharmacy. Many Part C plans include Part D drug coverage within the same plan, while others require you to purchase Part D separately if you stay with Original Medicare. The financial structure matters: you’ll likely pay a Part B premium plus a Part C premium, but some plans charge zero premium on top of Part B. Compare each plan’s maximum out-of-pocket limit carefully because a plan with a lower premium might have a higher annual cap, which means you could pay more during serious illness.

Part D Fills the Prescription Drug Gap

Part D tackles the drug coverage gap that Original Medicare ignores completely. Most routine prescription drugs cost you full price under Parts A and B alone, which explains why you should enroll in Part D when you first become eligible even if you don’t take medications right now. Missing the enrollment window triggers a late enrollment penalty that increases the longer you wait, and that penalty sticks with you permanently. Drug plans vary significantly by region and plan, so entering your ZIP code into Medicare’s plan finder shows exactly what’s available where you live and what each plan charges for your specific medications. Some people qualify for Extra Help, a program that reduces drug costs if your income falls below certain thresholds. Part D drugs are capped at $2,100 in 2026, and once you reach this cap, you won’t have to pay for covered drugs for the rest of the year.

Weighing Network Flexibility Against Cost Predictability

If you choose Original Medicare with Part D, you get maximum flexibility with providers but face unlimited out-of-pocket costs for medical services. If you choose Part C with integrated drug coverage, you get cost predictability and broader benefits like dental and vision coverage that Original Medicare doesn’t provide, but you sacrifice network flexibility and may face smaller provider choices in your area. This decision shapes not just your monthly costs but your entire healthcare experience. The gaps in Original Medicare coverage extend beyond just drugs and out-of-pocket limits-they also include services that many people rely on as they age, which is where supplemental coverage enters the picture.

Common Coverage Gaps and How Medigap Fills Them

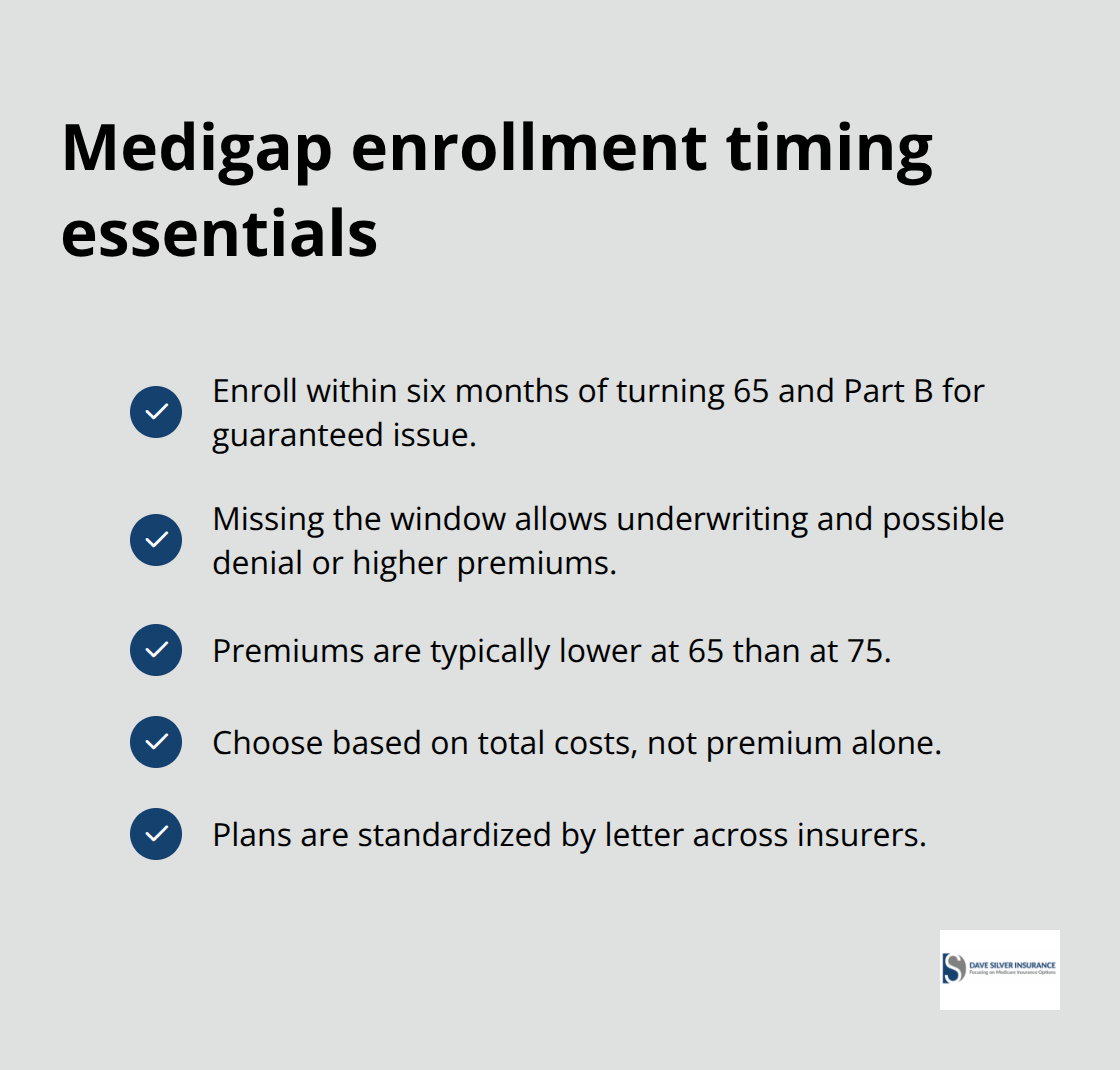

Original Medicare leaves you exposed to deductibles, coinsurance, and copayments that add up fast, especially during serious illness or extended hospital stays. Medigap, also called Medicare Supplemental Insurance, plugs these holes by paying the costs that Original Medicare doesn’t cover. Medigap plans are standardized by the federal government and named by letters like Plan G, Plan K, and Plan N, meaning the same Plan G from one insurance company covers identical benefits as Plan G from another company.

How Medigap Plans Differ in Coverage and Cost

The difference between plans comes down to how much they cover. Plan G covers your Part A hospital deductible, Part B deductible, coinsurance for hospital stays beyond 60 days, and your Part B coinsurance, among other costs. Plan K covers less and costs less monthly, making it appealing if you want to lower your premium but accept higher out-of-pocket costs when you use services. Plan N sits in the middle, covering most costs but leaving you responsible for up to $20 copayments for doctor visits and up to $50 for emergency room visits. Your Medigap choice directly determines how much you’ll pay when you actually need healthcare, so choosing based on premium alone is a costly mistake.

The Real Financial Protection Medigap Provides

The financial advantage of Medigap becomes clear when you face a serious health event. Under Original Medicare alone, a 90-day hospitalization costs you $434 per day for days 61 through 90, totaling $13,020 in coinsurance. With Plan G Medigap, that $13,020 disappears because your policy covers Part A hospital coinsurance. Your Part B coinsurance for doctor services during that hospitalization also vanishes. Over a lifetime, this protection prevents medical bills from destroying your savings.

Why Enrollment Timing Affects Your Premiums Permanently

Medigap comes with a monthly premium that varies by your age, location, and the plan letter you choose. A 65-year-old enrolling in Plan G might pay $120 to $180 monthly depending on where they live, while someone who waits until age 75 could pay $200 to $300 monthly for the same coverage.

Enrollment timing matters significantly: if you enroll in Medigap within six months of turning 65 and enrolling in Part B, insurance companies cannot deny you coverage or charge you more based on health conditions. Miss this window, and insurers can underwrite your application, meaning they review your medical history and can reject you or charge significantly higher premiums. The cost difference between enrolling at 65 versus 72 is substantial over your lifetime, and you cannot predict future health problems.

Final Thoughts

Medicare Part A, B, C, and D coverage works together to protect your health and finances, but only if you understand how each piece fits into your overall plan. Part A and B form the foundation of Original Medicare, covering hospital care and medical services, though they leave you exposed to unlimited out-of-pocket costs. Part C addresses that exposure by capping your annual costs and often adding benefits like dental and vision coverage, while Part D solves the prescription drug gap that Original Medicare ignores.

The right choice depends entirely on your health status, medications, preferred doctors, and financial situation. Someone with multiple chronic conditions and expensive medications might benefit from a Part C plan with integrated drug coverage and a predictable annual maximum, while someone else with a small network of trusted providers might prefer Original Medicare paired with Part D and a Medigap policy for maximum flexibility. Medicare Part A, B, C, and D coverage decisions are personal because no universal answer exists.

This complexity is exactly why working with someone who understands the details matters. We at Dave Silver Insurance have spent over 17 years helping people navigate these decisions with personalized guidance tailored to your unique circumstances, and our team is accessible seven days a week to provide recommendations based on your specific health and financial needs. Contact Dave Silver Insurance to get clarity on which Medicare coverage combination makes sense for you.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation