Medigap Plan F offers comprehensive coverage that fills gaps in Original Medicare, but whether it’s worth it depends on your health needs and budget. The plan covers deductibles, copayments, and coinsurance that Medicare doesn’t pay, which can add up quickly for people with frequent medical visits.

At Dave Silver Insurance, we help beneficiaries understand if Plan F makes financial sense compared to other coverage options. The answer isn’t the same for everyone-it comes down to your specific situation and long-term healthcare costs.

What Plan F Actually Covers

The Nine Gaps Plan F Fills

Plan F fills nine significant gaps in Original Medicare, and understanding exactly what those gaps are matters more than knowing the plan name. According to Medicare.gov, Plan F covers your Part A deductible, Part B deductible, Part A coinsurance, Part B coinsurance, Part B excess charges, skilled nursing facility coinsurance, the first three pints of blood, Part A hospice care coinsurance, and foreign travel emergency care up to plan limits. This means after you pay your monthly premium, you face virtually zero additional costs for any Medicare-approved service. No deductibles to meet. No coinsurance percentages to calculate. No copayments at the doctor’s office. That simplicity carries real value for people who visit doctors frequently or manage chronic conditions.

What Plan F Doesn’t Cover

Plan F does not cover prescription drugs, dental care, vision care, hearing aids, or long-term care. If you need any of those services, you’ll pay out of pocket or purchase separate coverage like a Part D plan for medications. This limitation matters because many people assume comprehensive coverage includes everything-it doesn’t.

The Real Cost Question

The real question isn’t what Plan F covers-it’s whether that coverage justifies the cost. In 2026, the Part B deductible sits at $283 annually, and Plan G, the closest alternative, covers everything Plan F does except that one deductible. According to data from NerdWallet, a 75-year-old nonsmoker in Atlanta pays roughly $184 per month for Plan F and $152 per month for Plan G. Over a year, Plan F costs $2,208 while Plan G costs $2,107 when you factor in paying the Part B deductible yourself. Plan G saves you money in that scenario.

The Break-Even Rule

The break-even rule is simple: if Plan F’s monthly premium exceeds Plan G’s by more than $23.58 per month (roughly one-twelfth of the $283 deductible), Plan G becomes the smarter choice mathematically. This calculation changes by location and age, which is why comparing actual quotes from multiple insurers in your area matters far more than general advice.

Eligibility Restrictions That Matter

Plan F isn’t available to anyone who became eligible for Medicare on or after January 1, 2020, a restriction that affects most people turning 65 today and eliminates Plan F as an option for them entirely. This eligibility barrier means your decision about Plan F depends first on whether you even qualify to purchase it. If you don’t meet the eligibility requirement, Plan G becomes your best alternative for comprehensive coverage. Understanding your eligibility status and comparing Plan G quotes in your area will help you move forward with confidence in your coverage choice.

Who Should Actually Buy Plan F

Eligibility Determines Everything

Plan F only makes sense for a specific group of people, and if you don’t fit that profile, you’re likely throwing money away each month. The eligibility restriction to pre-2020 Medicare beneficiaries already eliminates most readers from consideration. If you became eligible for Medicare before January 1, 2020, you can purchase Plan F. If you became eligible on or after that date, Plan F remains unavailable to you regardless of your health status or budget. This single factor determines whether the rest of this analysis applies to you at all.

High Medical Users Break Even Quickly

For those who qualify, the decision hinges on medical spending patterns and personal preference for simplicity over savings. People who visit doctors frequently benefit most from Plan F because it eliminates all deductibles and copayments after your premium payment. This predictability removes the mental burden of calculating costs at every appointment. Someone managing multiple chronic conditions who sees specialists regularly experiences this benefit most acutely. According to NerdWallet data, a person with three or more doctor visits monthly plus annual lab work and imaging often breaks even on Plan F’s higher premium by mid-year. A 75-year-old in Atlanta pays $184 monthly for Plan F versus $152 for Plan G-a $32 monthly difference. If that person visits doctors frequently, Plan F’s comprehensive coverage quickly justifies the higher cost.

Low Medical Users Should Compare Plan G

If your medical visits average fewer than six annually and you’re comfortable paying the $283 Part B deductible when it occurs, Plan G’s lower monthly cost saves you real money. The $384 in annual savings from Plan G’s lower premium exceeds the Part B deductible most years. This calculation shifts based on your specific location and age group, which is why comparing actual quotes in your area matters far more than national averages. Your local market determines whether Plan F or Plan G wins financially.

The High-Deductible Option for Budget-Conscious Beneficiaries

The high-deductible Plan F option deserves consideration for budget-conscious people who qualify and rarely use healthcare. This version costs around $67 per month according to NerdWallet data, compared to $184 for standard Plan F, with a $2,950 annual deductible before coverage begins. This approach works well if you’re healthy and want catastrophic protection without premium strain. However, it fails for anyone with predictable ongoing medical expenses. Someone with regular doctor visits or chronic conditions would face the deductible repeatedly, making this option impractical.

Cost Predictability Versus Savings

People seeking absolute cost predictability should choose standard Plan F if eligible, accepting the higher premium for zero surprise bills. Those comfortable with manageable out-of-pocket expenses should compare Plan G quotes in their specific location and age group before deciding. The break-even calculation shifts based on regional pricing, so national averages mislead more than they help. Your actual decision requires running these numbers with real quotes from insurers in your area rather than relying on general guidance. Once you’ve gathered quotes and calculated your likely medical expenses, you’ll have the information needed to evaluate whether Plan F’s comprehensive coverage justifies its cost in your specific situation.

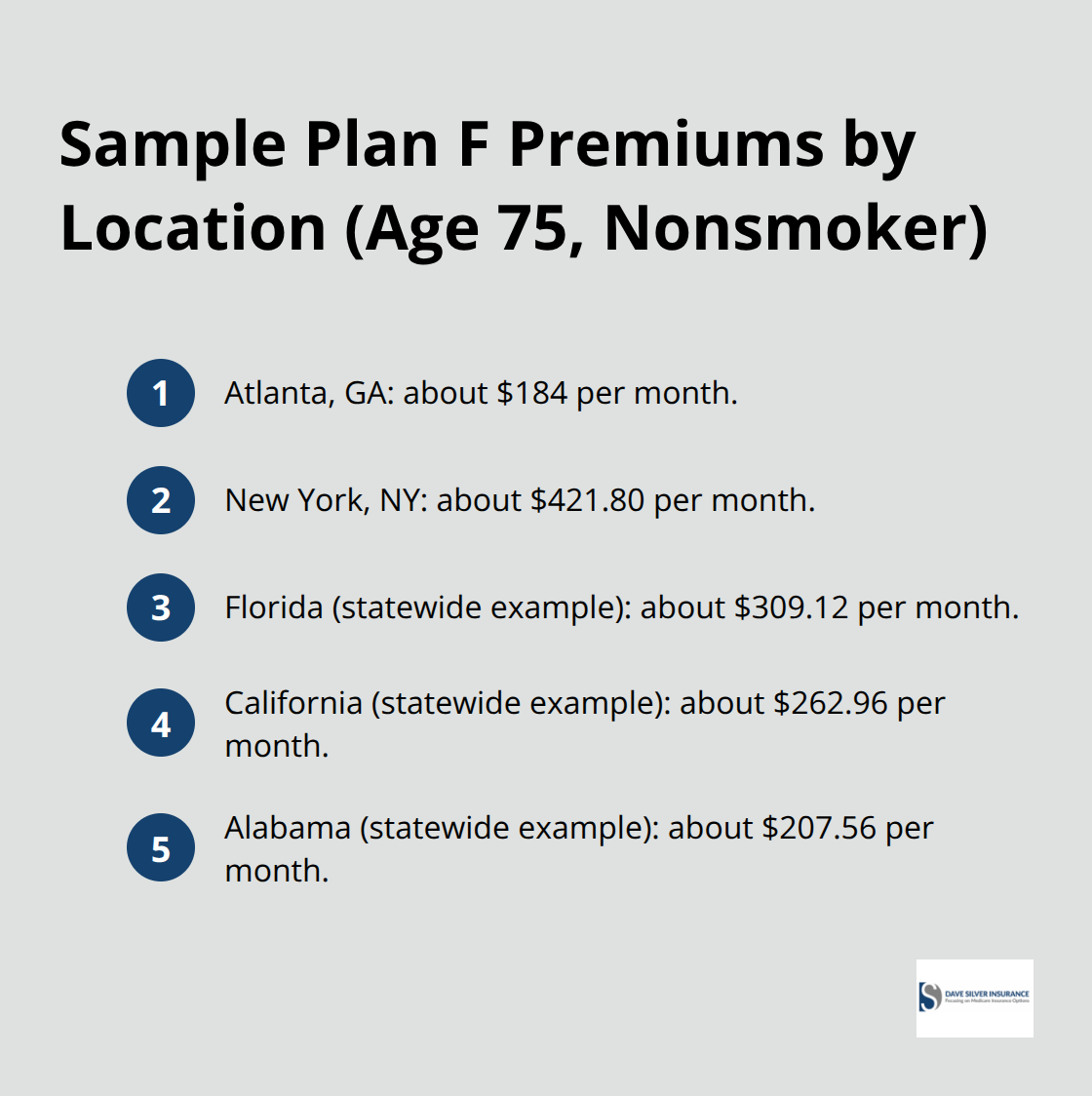

Plan F Premiums Across America

Regional Price Variations That Matter

Plan F premiums vary dramatically by location and age, making regional comparisons essential before you commit to this plan. According to NerdWallet data, a 75-year-old nonsmoker pays around $184 monthly in Atlanta but that same person pays roughly $421.80 monthly in New York-more than double the cost for identical coverage. Florida sits at approximately $309.12 monthly while California runs about $262.96 monthly.

These aren’t minor differences; they represent thousands of dollars annually in premium costs. Alabama offers some of the lowest rates at $207.56 monthly, suggesting you could save substantially by understanding your specific regional market rather than relying on national averages.

How Age Affects Your Premium

Age compounds these regional variations significantly. At age 65, Plan F costs roughly $166.21 monthly nationwide on average, but by age 95 that same plan costs approximately $421.75 monthly according to insurer data. This means a 30-year retirement could see premiums triple or quadruple over time depending on which pricing model your insurer uses. Attained-age-rated plans increase annually as you grow older, issue-age-rated plans lock in your enrollment age price but may jump if you switch insurers, and community-rated plans charge everyone the same price regardless of age. Understanding which pricing model your potential insurer uses matters far more than the initial monthly quote.

Plan G and Plan N as Lower-Cost Alternatives

Plan G consistently undercuts Plan F’s premiums while covering nearly everything except the $2,950 Part B deductible in 2026. NerdWallet data shows Plan G costs approximately $152 monthly for that same 75-year-old in Atlanta compared to Plan F’s $184, saving $32 monthly or $384 annually. Even when you account for paying the Part B deductible yourself, Plan G saves money in most scenarios unless you visit doctors so frequently that you hit the deductible multiple times yearly. Plan N offers another pathway with premiums around $128.08 monthly but includes copays for certain office visits and emergency room visits, making it suitable only for people comfortable with these additional costs.

High-Deductible Plans for Healthy Beneficiaries

The high-deductible Plan F option costs approximately $67 monthly according to NerdWallet, but requires you to pay $2,950 out of pocket before any coverage begins, making it viable only for exceptionally healthy individuals. This approach works well if you rarely use healthcare and want catastrophic protection without premium strain. However, it fails for anyone with predictable ongoing medical expenses, since someone with regular doctor visits would face the deductible repeatedly.

Finding Your True Total Cost

The real calculation isn’t which plan has the lowest premium-it’s which plan produces the lowest total annual cost when you combine premiums plus your expected out-of-pocket expenses. Someone expecting minimal medical use should compare actual Plan G quotes in their location rather than assuming Plan F justifies its higher premium. Rates vary substantially even for standardized plans, and your location, age, and health status create unique cost equations that national data cannot address. Gathering quotes from multiple insurers in your specific area reveals which option truly costs less over a full year.

Final Thoughts

Whether Plan F is worth it depends on three concrete factors: your eligibility status, your expected medical expenses, and your regional premium costs. If you became eligible for Medicare before January 1, 2020, you can purchase Plan F, but if not, Plan G becomes your best alternative for comprehensive coverage. Once you confirm eligibility, calculate your likely annual healthcare costs and compare them against actual premium quotes from multiple insurers in your area.

A person visiting doctors frequently breaks even on Plan F’s higher premium by mid-year, while someone with minimal medical needs saves money with Plan G’s lower monthly cost. The break-even calculation shifts based on your location and age, making regional comparisons far more valuable than national averages. Your next step involves gathering real quotes rather than relying on general guidance-contact insurers in your specific area and request quotes for both Plan F and Plan G at your age.

We at Dave Silver Insurance simplify this decision-making process with personalized guidance based on your unique health and financial needs. Our team works with you seven days a week to evaluate whether Plan F or another Medigap option fits your situation and helps you understand the real costs, compare plans accurately, and navigate enrollment deadlines. Contact Dave Silver Insurance today to get clarity on whether Plan F makes financial sense for you and to explore all your coverage options with confidence.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation