Cataract surgery restores your vision, but you’ll need new glasses afterward. Medicare Part B covers post-surgical glasses, though many people don’t realize exactly what that means for their wallet.

At Dave Silver Insurance, we help people understand their Medicare coverage for glasses after cataract surgery. This guide walks you through what Original Medicare pays, how to apply, and whether supplemental plans might give you better benefits.

What Medicare Part B Actually Covers for Post-Surgery Glasses

Medicare Part B covers one pair of eyeglasses or one set of contact lenses after cataract surgery with an intraocular lens implant, but the coverage comes with strict limitations that catch most people off guard. You pay 20 percent of the Medicare-approved amount for the lenses after you meet your Part B deductible, which means your out-of-pocket costs depend on what your eye doctor charges and whether they accept Medicare assignment. The critical detail most people miss: Medicare only covers standard frames coded as V2020, not deluxe frames or any upgraded options. If you want photochromic lenses, anti-reflective coatings, tinted lenses, or high-index materials, you’ll pay the full cost for those upgrades yourself. The frames must come from a Medicare-enrolled supplier, so call your eye doctor’s office and ask which suppliers they work with to prevent claim denials before they happen. Many suppliers aren’t enrolled in Medicare, which means submitting a claim through them results in automatic rejection and you absorb the entire bill.

When Coverage Kicks In After Surgery

Your coverage window opens after cataract surgery, but the timing matters for claims processing. You need a written prescription from your eye doctor specifically for post-surgical glasses to qualify, and that prescription should reflect the vision correction needed after the surgery heals (typically four to six weeks after the procedure). If you had cataract surgery in both eyes at different times, Medicare covers one pair after each surgery, so you could receive two pairs total across your lifetime if managed properly. However, if you skip getting glasses after your first eye surgery and later have surgery on the other eye, Medicare only covers one pair after the second surgery, eliminating your chance at a second pair. This rule catches people who delay ordering glasses thinking they’ll wait until both eyes are done. The claim must go through the Durable Medical Equipment channel using a DME PTAN, not through standard Medicare medical claims, which is why some suppliers struggle with processing and why you should verify your supplier’s DME credentialing before ordering.

What You Actually Pay Out of Pocket

After you meet your Part B deductible of 226 dollars in 2026, you pay 20 percent coinsurance on the Medicare-approved amount for lenses and standard frames combined. If Medicare approves 300 dollars for your glasses, you pay 60 dollars after the deductible. However, if your eye doctor charges 500 dollars and doesn’t accept assignment, you could owe significantly more. Upgraded lens features like scratch-resistant coatings, mirror coatings, or polarization add hundreds of dollars that Medicare won’t touch. Many people assume their supplemental insurance or Medicare Advantage plan covers these extras, but Original Medicare Medigap policies don’t cover vision, and you need to verify your specific MA plan’s vision benefits separately. Call your supplier and request a cost estimate before ordering to prevent surprises at checkout and to decide whether upgrades are worth the additional expense.

How to Verify Your Supplier’s Medicare Status

Not all eyewear suppliers accept Medicare, and submitting claims to non-enrolled suppliers guarantees denial. Your eye doctor’s office can tell you which suppliers they work with and which ones accept Medicare assignment (meaning Medicare pays the supplier directly). You can also use Medicare’s provider and supplier search tool to confirm enrollment status before placing an order. Suppliers who accept assignment typically charge less because Medicare pays them directly, reducing your out-of-pocket responsibility. If a supplier isn’t enrolled, you’ll pay the full amount upfront with no Medicare reimbursement, even if the glasses would otherwise qualify for coverage. Taking five minutes to verify enrollment status saves you hundreds of dollars and prevents the frustration of denied claims.

Navigating Coverage for Both Eyes

The two-eye rule creates confusion because it depends on the timing of your surgeries and whether you ordered glasses between procedures. If you had surgery on your first eye and ordered glasses, then later had surgery on your second eye, Medicare covers one pair after each surgery (two pairs total). If you had surgery on both eyes but didn’t order glasses after the first surgery, Medicare only covers one pair after the second surgery. This timing matters because once you receive your one pair after the second surgery, you’ve exhausted your lifetime benefit for both eyes. Understanding this rule before your first surgery helps you plan whether to order glasses immediately or wait until both eyes are done. Your eye doctor can explain your specific situation and help you decide the best timing for your orders.

Getting Your Medicare Claim Approved

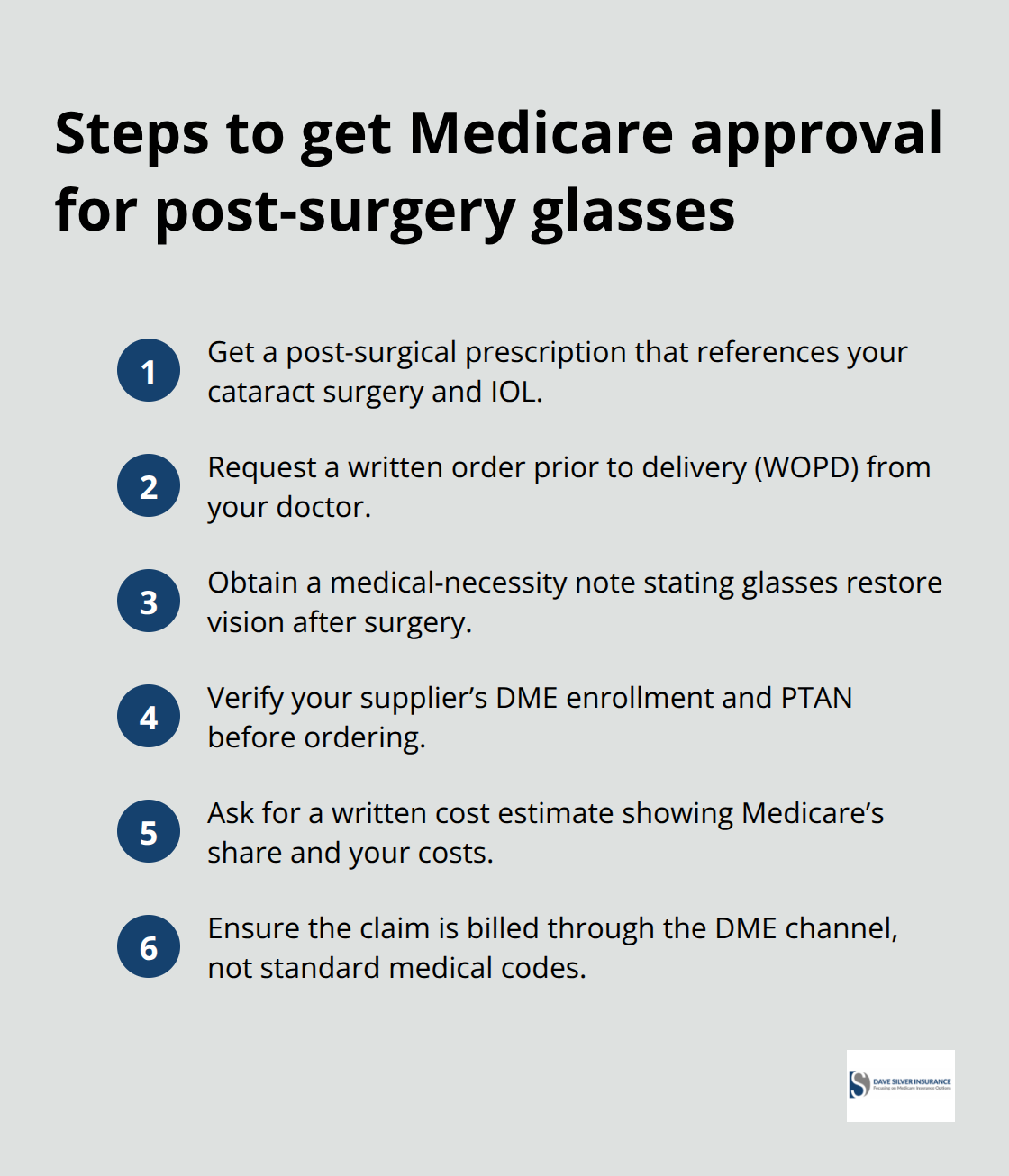

Gather Documentation Before You Order

Your eye doctor holds the key to Medicare approval, and most practices don’t provide the documentation you actually need. The moment your cataract surgery heals, ask your doctor’s office for a written prescription that specifically states the post-surgical vision correction required. This prescription must reference the cataract surgery and intraocular lens implant, not just a standard eyeglasses prescription, because Medicare’s DME processors reject claims that lack this surgical context.

Request that your doctor’s office also provide a written order prior to delivery (WOPD), which CMS requires for certain ophthalmic devices before the supplier ships your glasses. Many eye doctors won’t volunteer this document, so you must ask directly. Your doctor should also confirm in writing that the glasses are medically necessary to restore vision after surgery, not just a convenience purchase. Get this documentation in hand before contacting any supplier, because suppliers won’t process orders without it.

Verify Your Supplier’s DME Enrollment

When you call your supplier, provide them with your doctor’s prescription, the WOPD, and your Medicare information all at once so they can verify your eligibility through the DME channel using their DME PTAN. Ask the supplier to provide a written cost estimate showing what Medicare will pay, what you’ll owe after your Part B deductible, and what upgrades will cost out of pocket. This estimate prevents surprises and gives you time to decide whether deluxe features justify the additional expense. Most denials happen because suppliers submit claims through the wrong billing channel or lack proper DME credentialing, so confirming your supplier’s DME enrollment before placing an order eliminates the most common failure point. If your supplier can’t produce a DME PTAN or hesitates when you ask about DME processing, find a different supplier immediately because that supplier likely isn’t set up to handle post-cataract glasses properly.

Understand Why Claims Get Denied

When your claim gets denied, the reason usually falls into three categories: missing documentation, incorrect billing codes, or non-enrolled supplier status. If your supplier billed through standard Medicare medical codes instead of DME codes, the claim fails automatically, and you’ll need to resubmit through the DME channel. If your doctor’s prescription didn’t mention the cataract surgery or IOL implant, Medicare denies the claim as medically unjustified, forcing you to obtain a corrected prescription and resubmit. If your supplier wasn’t enrolled in Medicare’s DME program when they submitted the claim, you receive a denial and no reimbursement, leaving you to pay out of pocket and then fight for a refund. Appeals require the same documentation your initial claim needed, plus proof that the denial was incorrect, which takes months to resolve.

Act Fast to Prevent Problems

The faster solution is preventing denial in the first place by verifying your supplier’s DME credentialing, obtaining complete documentation from your doctor, and requesting a cost estimate before ordering. If a denial does arrive, contact your supplier first to determine whether the problem was on their end or your doctor’s, then decide whether resubmitting or finding a new supplier makes sense based on timing and cost. Once you’ve navigated the approval process and received your glasses, you’ll want to understand how supplemental coverage options could have reduced your out-of-pocket expenses-and how they might help with future vision care needs.

Supplemental Plans That Actually Cover Vision Costs

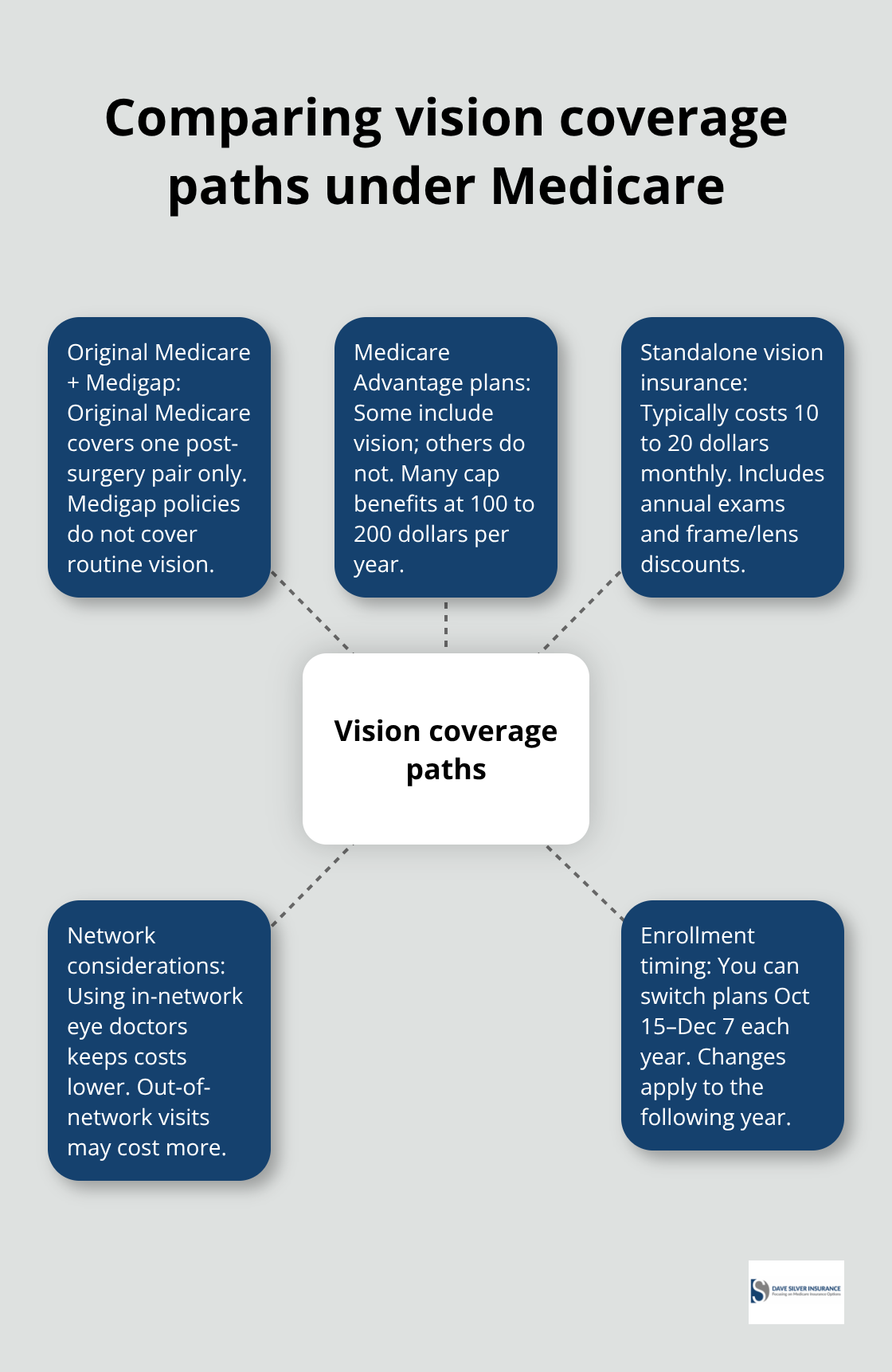

Original Medicare’s vision coverage stops after your post-surgery glasses, leaving you exposed to routine eye exams, new prescriptions, and unexpected vision problems that emerge months or years later. Medigap policies sold by insurance companies do not cover vision care at all, which surprises most people who assume supplemental insurance fills all the gaps Medicare leaves behind. If you have a Medigap plan, you’re paying for vision benefits that don’t exist in your policy, so adding separate vision insurance through a private carrier becomes necessary if you want protection beyond that single post-surgery pair.

How Medicare Advantage Plans Bundle Vision Benefits

Medicare Advantage plans operate differently because they can bundle vision benefits into their coverage, though not all plans include them and benefits vary dramatically by plan and region. Some Medicare Advantage plans offer extra benefits that include routine eye exams and eyeglasses or contact lenses, while others offer nothing beyond Original Medicare’s post-surgery glasses. The plans that do cover vision typically cap benefits at 100 to 200 dollars per year, which barely covers one eye exam and basic frames.

Standalone Vision Insurance for Original Medicare Users

If you’re on Original Medicare with a Medigap policy and you want comprehensive vision coverage, you’ll need to purchase standalone vision insurance through companies like VSP or EyeMed, which cost 10 to 20 dollars monthly and provide annual eye exams, discounts on frames and lenses, and coverage for contact lenses. This approach adds another monthly expense but fills the gaps that neither Original Medicare nor Medigap policies address.

Comparing Your Coverage Options

The financial trade-off matters because a Medicare Advantage plan with strong vision benefits might save you 100 to 150 dollars annually compared to Original Medicare plus Medigap plus standalone vision insurance, but only if you actually use the benefits and stay within the plan’s approved network. If your current eye doctor isn’t in your plan’s network, switching plans means finding a new provider or paying out of network at higher costs. We help you compare what your current coverage actually pays for vision versus what different Medicare Advantage plans offer in your area, so you can decide whether the vision benefit justifies switching plans.

Timing Your Plan Changes

Many people discover they’re overpaying for vision coverage that doesn’t align with their actual eye care needs, and a few minutes reviewing your specific situation reveals whether consolidating into a Medicare Advantage plan makes financial sense. The enrollment period to switch plans runs from October 15 through December 7 each year, so if you’re unhappy with your current vision coverage, you have a specific window to make changes and lock in better benefits for the following year.

Final Thoughts

Medicare coverage for glasses after cataract surgery follows specific rules that most people learn too late, after they’ve already paid hundreds of dollars in unexpected costs. Original Medicare Part B covers one pair of standard-frame glasses or contact lenses after your surgery, you pay 20 percent coinsurance after meeting your deductible, and your supplier must hold Medicare DME enrollment or your claim faces automatic denial. Timing your purchases around each eye’s surgery date and obtaining complete documentation from your eye doctor prevents the denials that trap most patients in claim disputes.

Beyond that single post-surgery pair, your vision coverage depends on supplemental insurance choices you make today. Medigap policies don’t cover vision at all, so you either need a Medicare Advantage plan with vision benefits or standalone vision insurance if you want protection for routine eye exams and future glasses. The financial math shifts based on your location, your eye doctor’s network status, and how often you actually need eye care, which is why comparing your specific options matters far more than following generic advice.

We at Dave Silver Insurance help you navigate these decisions with personalized guidance tailored to your health and financial situation. Schedule a consultation with us to review your current coverage, understand what Medicare coverage for glasses after cataract surgery means for your wallet, and explore whether switching plans would reduce your vision care expenses. We’re available seven days a week to answer your questions and provide the clarity you need to make confident decisions about your Medicare coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation