Medicare costs explained for 2026 are more complex than ever, with premiums, deductibles, and coverage gaps affecting your wallet in different ways. At Dave Silver Insurance, we’ve seen too many people overpay simply because they didn’t understand their options.

This guide breaks down exactly what you’ll pay for Parts A, B, C, and D, plus the practical strategies to cut your out-of-pocket expenses. We’ll also show you the costly mistakes that could drain thousands from your retirement savings.

What You Actually Pay for Medicare in 2026

Part A and Part B: The Foundation Costs

Most people turning 65 assume Medicare is affordable because Part A is free. That’s only half the story. In 2026, the real costs start piling up across Parts A, B, C, and D, and understanding each component separately won’t save you money-you need to see how they work together.

Part A covers hospital stays, but the $1,736 deductible per admission hits immediately. Then you pay $434 per day for days 61–90 and $868 per day for days 91–150. A two-week hospitalization costs roughly $3,000 out-of-pocket after the deductible alone.

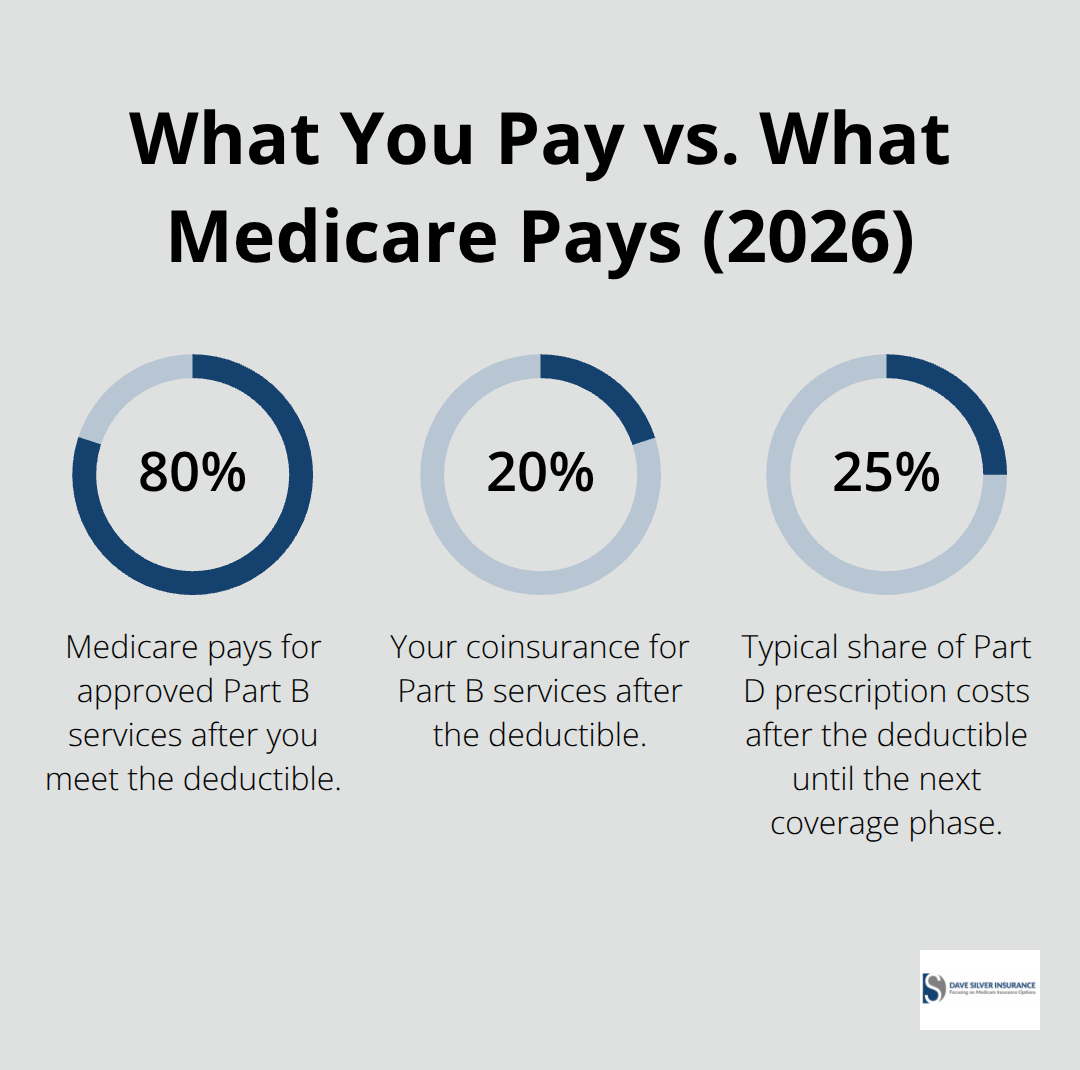

Part B medical insurance runs $202.90 per month in 2026, but that’s just the base. After you pay the $283 annual deductible, Medicare covers 80% and you cover 20% of all approved services. A single specialist visit costing $500 means you pay $283 upfront plus 20% of the remaining amount.

Income-Related Adjustments Change Everything

If you earn over $109,000 as a single filer, income-related adjustments (IRMAA) add another $81.20 to $487 monthly to your Part B bill, pushing total annual Part B costs to $3,400–$5,000 before you see a doctor. Original Medicare has no annual spending cap, so these costs accumulate indefinitely throughout the year.

Medicare Advantage: Lower Premiums, Hidden Restrictions

Medicare Advantage plans (Part C) look cheaper upfront-many have $0 premiums beyond your Part B payment-but they impose network restrictions and require prior authorization for many services. The average Medicare Advantage premium sits around $14 monthly in 2026, yet you pay copays instead of coinsurance, typically $20–$50 per visit.

The advantage is the annual out-of-pocket maximum of $9,250 in 2026; once you hit that ceiling, the plan covers everything. This predictability matters far more than the low upfront premium.

Part D: Drug Costs That Shift Annually

Part D prescription drug coverage adds another layer. The maximum deductible is $615 in 2026, though many plans charge less or none. After meeting your deductible, you pay roughly 25% of drug costs until you reach $2,100 in total out-of-pocket spending, then catastrophic coverage kicks in and your drugs cost almost nothing. The insulin cap of $35 per month helps diabetes patients significantly.

Plan premiums vary wildly-some plans cost $15 monthly, others $80-and the formulary (list of covered drugs) changes yearly, so a plan that worked perfectly in 2025 might exclude your medication in 2026.

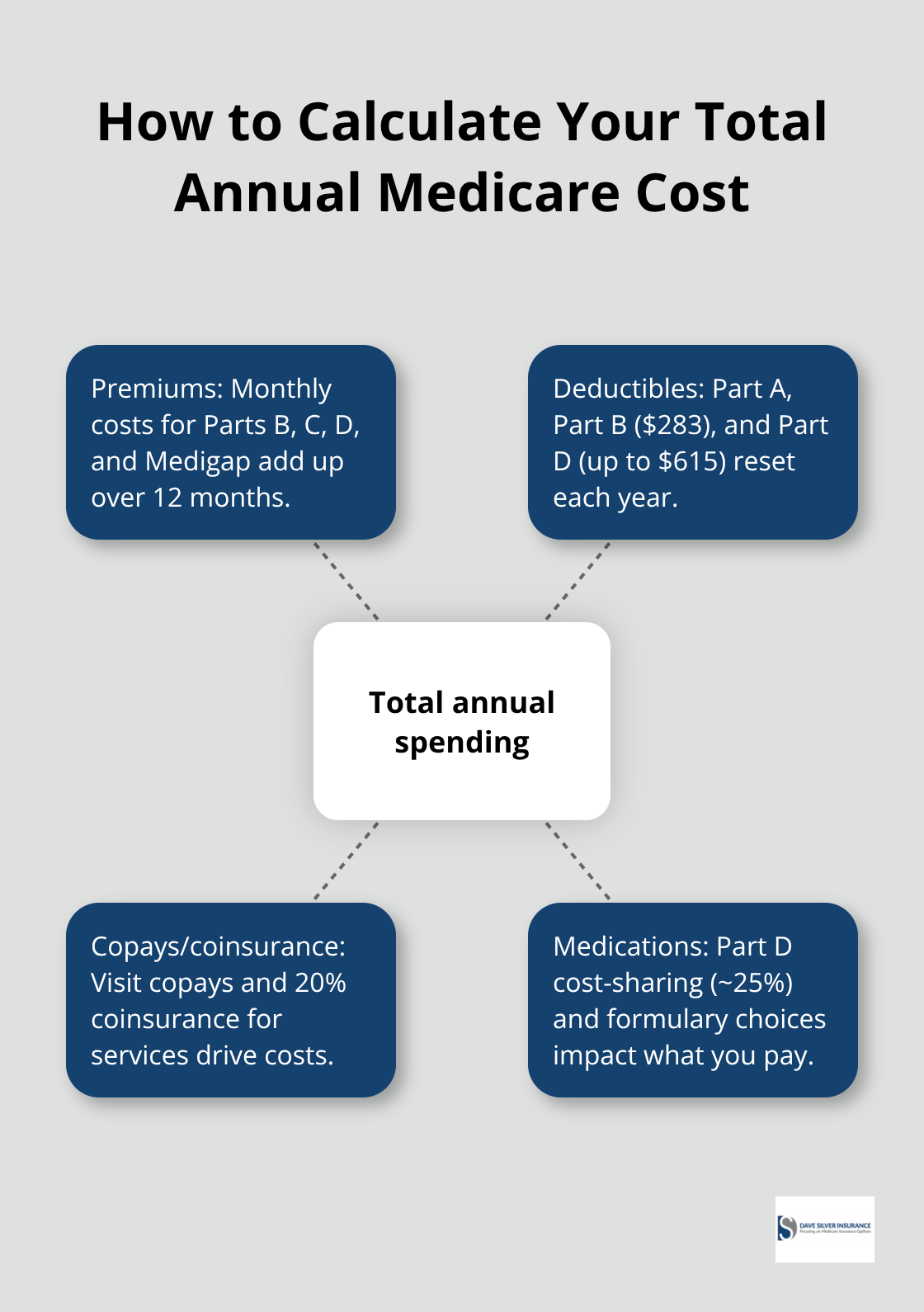

The Real Decision: Total Annual Spending

The real decision isn’t which plan sounds best; it’s calculating your total annual spending by combining premiums, deductibles, copays for your actual doctors, and drug costs for your specific medications. This calculation reveals which option truly fits your budget and health situation.

How to Cut Your Medicare Costs Without Sacrificing Coverage

Medigap Plans Fill the Gaps Original Medicare Leaves Open

Medigap insurance covers what Original Medicare doesn’t, and the numbers prove its value. After you hit the Part B deductible of $283, you pay 20% coinsurance on everything-a $5,000 surgery costs you $1,000 out of pocket. Plan G covers 100% of that coinsurance plus the Part A deductible, so you pay predictable premiums instead of facing catastrophic bills. Kaiser Family Foundation data shows Plan G averages $164 monthly across the country, though premiums range from $140 to $236 depending on location and insurer. Over a year, Plan G costs roughly $1,968 to $2,832, but it caps your exposure completely-Original Medicare has no annual maximum. If you’re healthy and use few services, Plan N might work; it costs less (around $168 monthly on average) but charges you a $20 copay for some doctor visits and doesn’t cover Part B excess charges in certain states. High-deductible Medigap options like Plan G cut premiums to roughly $56–$100 monthly by requiring you to pay a $2,950 annual deductible first, making sense only if you rarely need care.

Calculate Total Spending, Not Just Premiums

Don’t compare premiums alone. Calculate what you’d actually spend on your expected doctor visits and procedures, then add the Medigap premium to that number. A $150 monthly Plan G premium plus zero coinsurance beats a $50 monthly plan premium plus 20% coinsurance on $10,000 in annual care. This calculation reveals which option truly fits your budget and health situation.

Enrollment Windows Determine Your Options

Your enrollment window determines whether you can switch plans without penalties or medical underwriting. You have a six-month Medigap open enrollment period starting the month you turn 65 and enroll in Part B-miss it, and insurers can deny coverage or charge higher premiums based on health status. If you’re currently in Medicare Advantage and want to switch to Original Medicare plus Medigap, you can do so during the annual open enrollment from October 15 to December 7, but Medigap carriers aren’t required to accept you outside your initial enrollment window. The birthday rule, available in some states, lets you switch Medigap plans once yearly during your birth month without medical underwriting, though not all insurers participate.

Shop Multiple Carriers During Eligible Windows

Shop aggressively during your eligible windows-get quotes from at least three carriers, since the same Plan G can cost $140 at one company and $236 at another in the same area. Don’t wait until January to enroll; plans sold in October often start coverage January 1, giving you time to understand your new benefits before you need them. Your actual doctors and medications determine which plan saves you the most money, so verify that your preferred providers accept each plan you’re considering and that your prescriptions fall on the formulary.

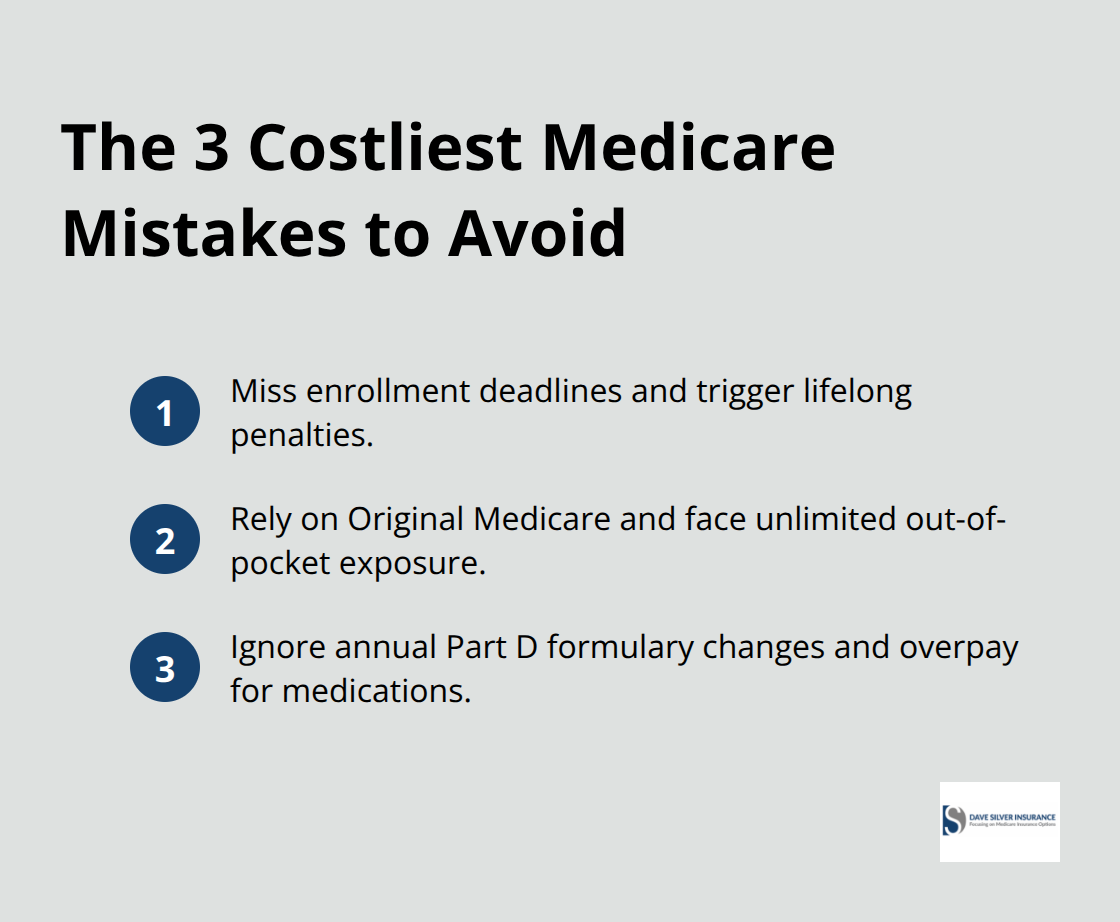

Mistakes That Cost You Thousands in Medicare

The three most expensive Medicare mistakes happen before you turn 65, not after. Missing enrollment deadlines triggers penalties that stick with you for life. Not understanding Original Medicare’s coverage gaps leaves you exposed to unlimited out-of-pocket costs. Ignoring annual Part D formulary changes means your medications might not be covered next year, forcing you to switch plans mid-year or pay full price. These aren’t theoretical problems-they’re financial disasters that happen regularly, and they’re entirely preventable with specific actions taken at the right time.

Enrollment Penalties Lock In Permanent Cost Increases

The Part B late enrollment penalty alone costs 10% extra on your premium for every year you could have enrolled but didn’t. If you delay enrolling in Part B by just three years, you’ll pay an additional 30% on your Part B premium forever, according to Medicare.gov. In 2026, that’s $202.90 per month becoming $263.77 per month permanently. Over a 20-year retirement, that three-year delay costs roughly $14,600 in extra premiums. The Part D late enrollment penalty works the same way-1% per month you could have enrolled but didn’t, also permanent. Miss Part D enrollment by 18 months and you’ll pay 18% extra on every prescription drug plan premium for the rest of your coverage. These penalties compound across Parts A, B, and D. The six-month window for Medigap enrollment starting when you turn 65 and enroll in Part B is ironclad; insurers can legally deny your application or charge substantially more based on health status if you miss it. Your enrollment window determines everything, yet most people don’t realize these deadlines exist until it’s too late. Mark your calendar now if you’re turning 65 within the next 12 months, because Social Security doesn’t send reminders and Medicare.gov assumes you’re checking their website monthly.

Original Medicare’s Unlimited Out-of-Pocket Exposure Destroys Budgets

Original Medicare has no annual out-of-pocket maximum, meaning your 20% coinsurance costs accumulate all year with no ceiling. A serious health event like cancer treatment or major surgery can trigger $20,000 to $50,000 in out-of-pocket costs in a single year because you keep paying 20% coinsurance on everything after meeting the Part B deductible. This exposure surprises people specifically because Medicare covers 80%-it sounds protective until you face a $100,000 surgery and realize you’re paying $20,000 out of pocket. Medigap plans eliminate this risk by capping your exposure completely, but people often assume Original Medicare alone is sufficient because they’ve been healthy so far. A single hospitalization lasting 100 days costs you the $1,736 Part A deductible plus $434 daily for 30 days plus $868 daily for 10 days, totaling roughly $31,500 out of pocket before Medigap or Medicare Advantage coverage kicks in. Original Medicare’s design assumes you’ll buy supplemental coverage; going without it is financially reckless. The coverage gap isn’t hidden-it’s documented on Medicare.gov-but people don’t read the fine print until they get a bill.

Part D Formulary Changes Destroy Your Plan Mid-Year

Insurance companies change their Part D drug formularies every single year, and your medication might move to a higher tier, get excluded entirely, or require prior authorization for the first time. A drug that cost you $15 per month in 2025 might cost $80 per month in 2026 because the plan moved it from Tier 1 generic to Tier 3 preferred brand. You won’t discover this until January 1 when you try to fill your prescription at the pharmacy. This problem requires action in October during annual enrollment, not in January when it’s too late. Compare your exact medications on each plan’s 2026 formulary before you enroll, using the actual dosage you take and your preferred pharmacy. Prescription drug costs vary dramatically by plan even within the same region-Plan A might cover your three medications for $120 monthly while Plan B charges $280 monthly for identical coverage. Shop Part D plans annually specifically for formulary changes, not just price increases. The $35 insulin cap under Part D helps diabetes patients, but only if your specific insulin is covered at that price on your plan’s formulary. Generic alternatives exist for many medications, but your doctor prescribes specific drugs for specific reasons, so switching to generics isn’t always an option without medical consultation.

Final Thoughts

Medicare costs explained for 2026 boil down to one reality: the cheapest plan upfront rarely saves you the most money overall. You’ve now seen how Part A deductibles, Part B coinsurance, Part C network restrictions, and Part D formulary changes interact to determine your actual annual spending. The three biggest mistakes-missing enrollment deadlines, ignoring Original Medicare’s unlimited out-of-pocket exposure, and overlooking annual Part D changes-cost thousands in penalties and unexpected bills.

Calculate your personal total annual cost by combining premiums, deductibles, and expected out-of-pocket expenses for your actual doctors and medications. This number reveals which option truly fits your budget and health situation far better than comparing premiums alone. If you turn 65 within the next 12 months, mark your enrollment deadlines on your calendar immediately, since Social Security won’t remind you and missing these windows locks in permanent penalties.

We at Dave Silver Insurance simplify this complexity with personalized guidance based on your unique health and financial needs. Schedule a consultation with Dave Silver Insurance to receive tailored recommendations backed by thorough analysis of your situation. The cost of getting this decision wrong far exceeds the value of expert guidance.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation