Medicare enrollment deadlines are unforgiving. Miss them, and you’ll face penalties that stick around for years. At Dave Silver Insurance, we’ve seen countless people make preventable mistakes during this critical window.

That’s why Medicare enrollment help today matters so much. The right guidance can save you thousands of dollars and protect your healthcare access when you need it most.

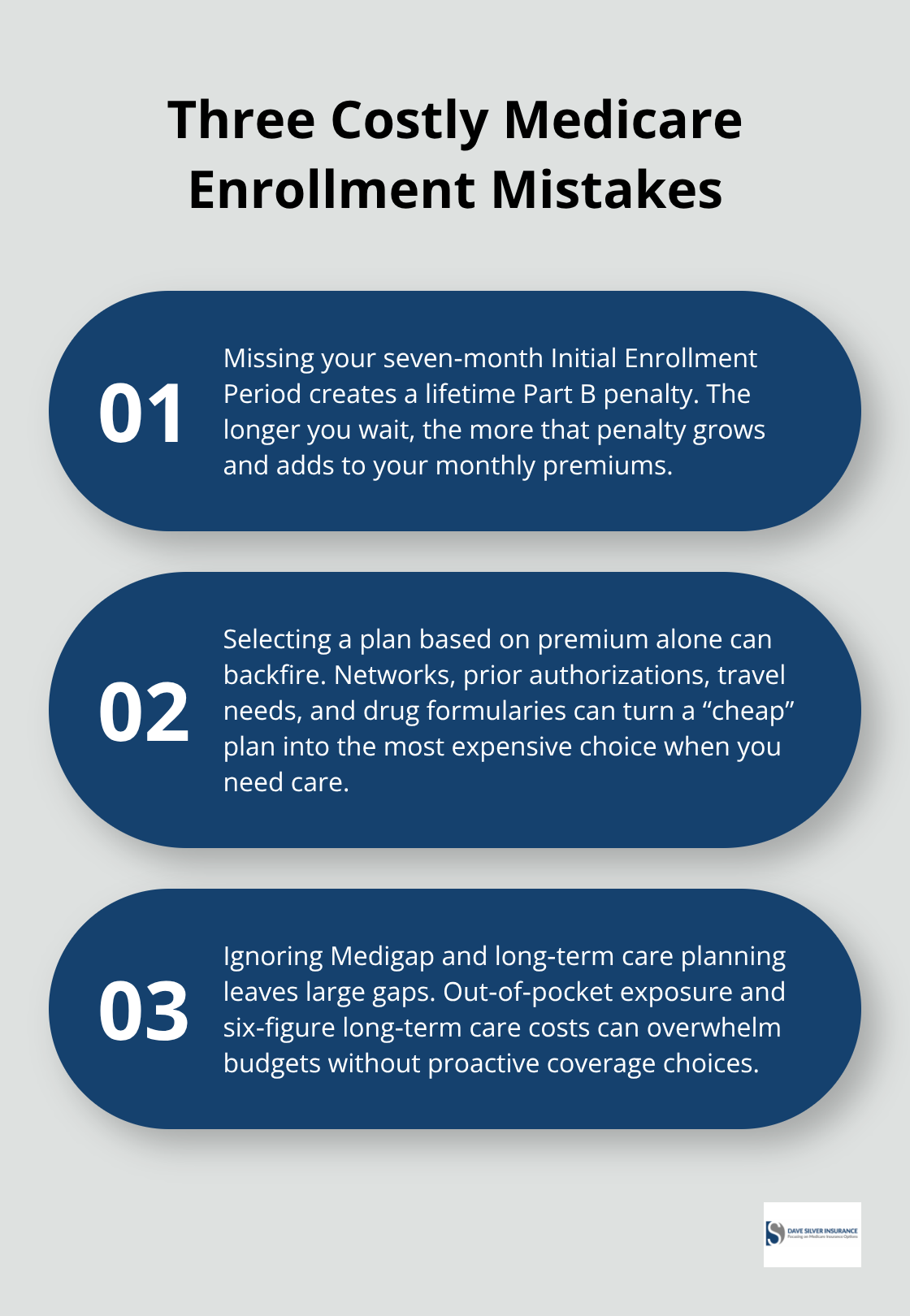

Three Mistakes That Cost Medicare Enrollees Thousands

Missing Your Seven-Month Enrollment Window

The Initial Enrollment Period lasts for 7 months, starting 3 months before you turn 65, and ending 3 months after the month you turn 65. Miss this window, and you’ll pay a monthly Part B late enrollment penalty for as long as you have Part B coverage. The penalty increases the longer you wait. Most people don’t realize this timing detail and assume they have more flexibility than they actually do.

Enrollees who discovered they missed their deadline by weeks faced permanent penalties that added hundreds of dollars annually to their premiums.

Selecting a Plan Based on Price Alone

Choosing the wrong plan ranks equally high on the list of costly mistakes. Medicare Advantage plans often require provider networks and prior authorization, meaning the doctors you’ve seen for years might not be in-network or may require approval before you receive care. If you travel frequently, Medicare Advantage coverage becomes even riskier because these plans typically don’t cover services outside their geographic area. Original Medicare with a Medigap policy offers broader flexibility, but you must enroll in Medigap during your initial enrollment window or face medical underwriting and significantly higher premiums later.

Many people pick a plan based on monthly premium alone, ignoring deductibles, copayments, and whether their medications are covered under Part D. The Social Security Administration calculates Income-Related Monthly Adjustment Amounts starting at income thresholds of $109,000 for individuals and $218,000 for couples in 2026, meaning higher earners pay hundreds more monthly than they anticipated.

Ignoring Medigap and Long-Term Care Gaps

Overlooking Medigap entirely leaves you exposed to substantial out-of-pocket costs that Original Medicare doesn’t cover, including most dental, hearing, and vision services. Long-term care costs can exceed $100,000 per year and aren’t covered by Medicare at all, yet many enrollees don’t plan for this gap until it’s too late. These three mistakes-missed deadlines, poor plan selection, and inadequate supplemental coverage-create financial stress that professional guidance can prevent. Expert advisors help you navigate these decisions with personalized recommendations tailored to your health and financial situation.

Why Expert Guidance Transforms Your Medicare Enrollment

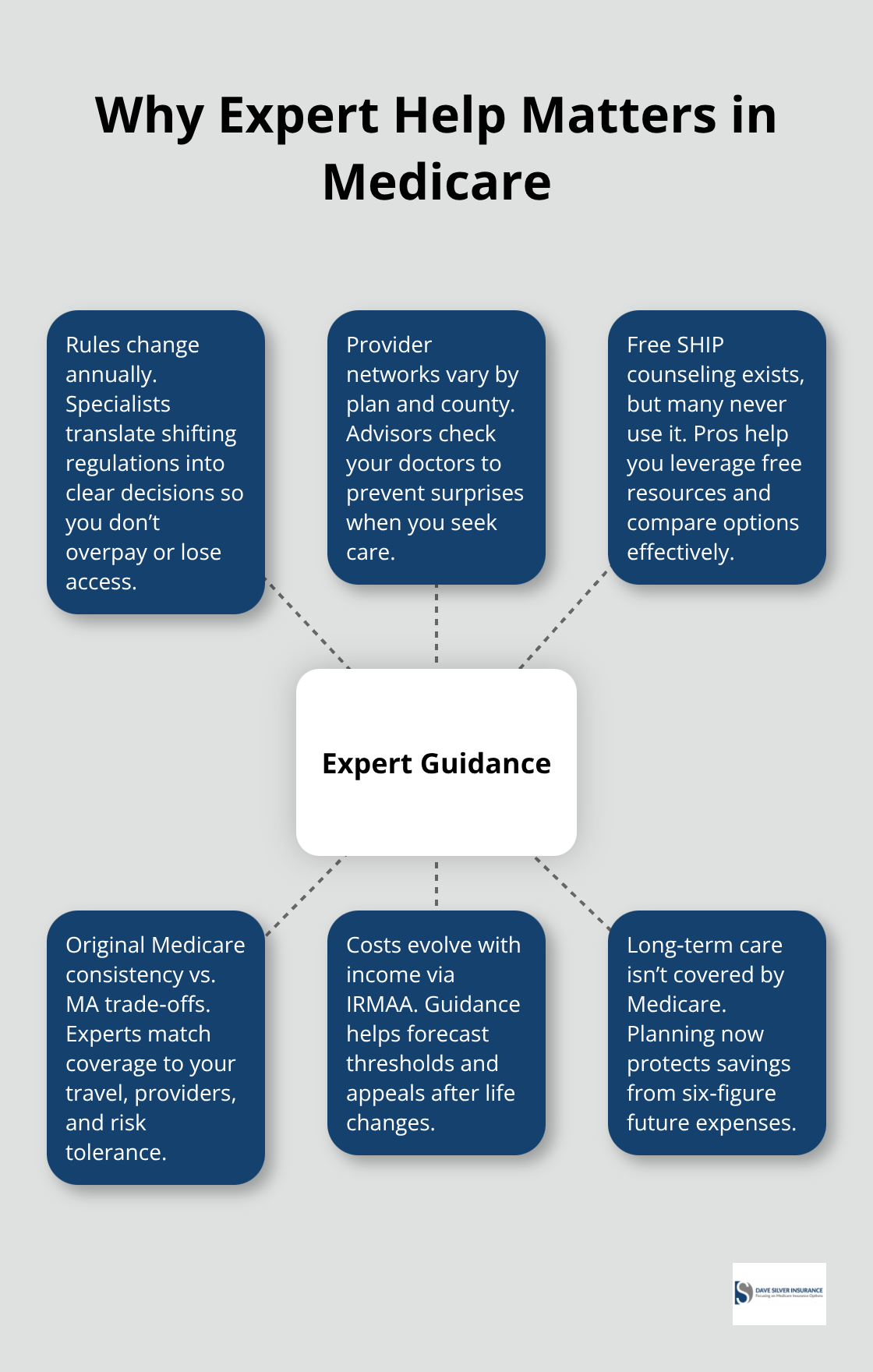

Medicare Rules Shift, But Your Mistakes Stick Around

Medicare regulations change annually, and the gap between a well-chosen plan and a costly mistake often comes down to understanding rules most people encounter for the first time at 65. State Health Insurance Assistance Programs provide free counseling on plan selection and cost management, yet many enrollees never contact them.

The reality is that Medicare Advantage networks vary dramatically by geography and plan-a doctor who accepts Plan A in your county might reject Plan B entirely. You won’t discover these gaps until you need care.

Original Medicare Offers Consistency, But Timing Matters

Original Medicare offers nationwide coverage consistency, but pairing it with Medigap requires enrollment during your Initial Enrollment Period or facing medical underwriting that can add hundreds to your monthly premiums. Income-Related Monthly Adjustment Amounts recalculate every year based on your prior tax returns, and a significant life change like retirement or divorce can trigger an appeal to lower these surcharges. Without personalized guidance, most people optimize for today’s premium and ignore tomorrow’s healthcare access.

Expert Advisors Analyze What Actually Matters

Expert advisors examine which providers you actually use, whether you take medications requiring specialized formularies, and whether your income will trigger IRMAA thresholds in future years. They identify whether you qualify for Special Enrollment Periods tied to job loss or qualifying events, potentially recovering months of retroactive coverage. Long-term care planning receives virtually no attention during standard enrollment, yet nursing home costs exceeding $100,000 annually demand decisions about supplemental insurance or savings strategies made now, not when a health crisis forces your hand.

Your Health Trajectory Shapes Better Decisions

Personalized recommendations account for your health trajectory, travel patterns, and financial situation rather than treating enrollment as a checkbox exercise. The stakes justify professional guidance because enrollment mistakes compound across years, whereas informed decisions made once protect your access and finances for decades. Getting started with the right support transforms confusion into clarity.

Get Professional Help Before You Enroll

Why Timing Matters More Than You Think

The difference between contacting a Medicare specialist before enrollment versus after mistakes occur amounts to thousands of dollars. State Health Insurance Assistance Programs offer free counseling through Medicare.gov, and they field calls from people who realize too late that their chosen plan doesn’t cover their doctors or medications. The enrollment window moves fast, and decisions made in those seven months shape your healthcare costs and access for years. Calling 1-800-MEDICARE provides 24/7 assistance through the Centers for Medicare and Medicaid Services, but that line handles volume-based questions rather than personalized analysis.

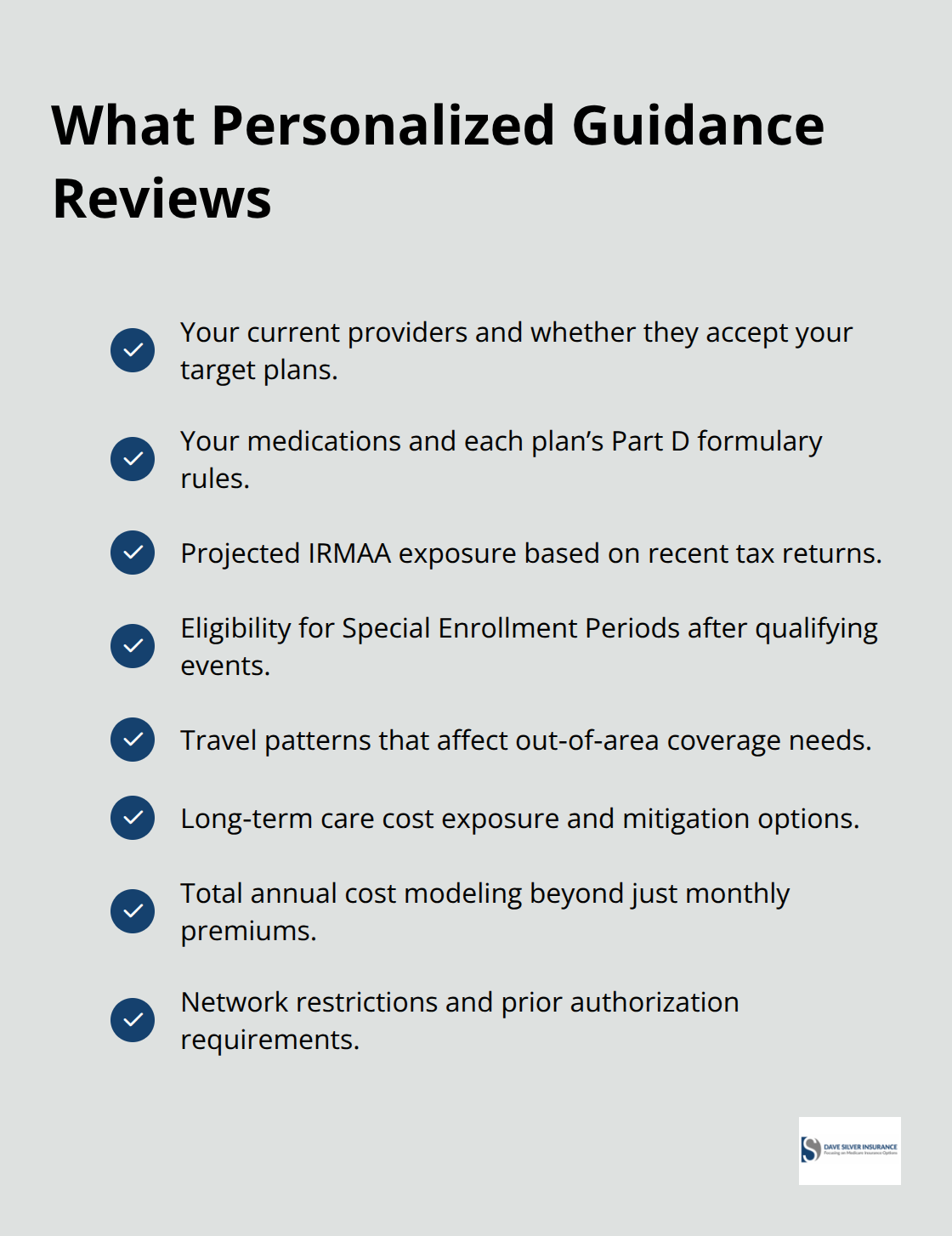

What Personalized Guidance Actually Examines

Personalized guidance requires someone who examines your specific situation: which providers you actually visit, whether your medications appear on your plan’s formulary, and whether income changes will trigger IRMAA surcharges in 2027 or beyond. A Medicare specialist reviews your 2025 tax returns to predict whether you’ll cross the $109,000 threshold for individuals or $218,000 for couples, helping you avoid surprise premium increases. They identify whether you qualify for Special Enrollment Periods tied to job loss, Medicaid coverage changes, or other qualifying events that could recover months of retroactive coverage. Without this analysis, most people enroll based on current monthly premiums and discover coverage gaps only when they need care.

How Specialists Match Plans to Your Life

A specialist walks through your health history, medication list, and travel patterns to recommend plans that actually match your life rather than theoretical needs. They confirm whether Medigap makes sense for your situation or whether Medicare Advantage’s lower premiums justify network restrictions. They explain how long-term care costs exceeding $100,000 annually fall outside Medicare coverage and discuss whether supplemental insurance or savings strategies fit your financial plan. You complete enrollment with full understanding of what your plan covers, what it doesn’t, and which actions to take if your health or income changes.

Starting the Conversation Now Eliminates Regret

This clarity eliminates the regret that follows discovering you selected wrong. Starting this conversation now, before enrollment deadlines pressure your decision-making, transforms the process from stressful to straightforward. Accessible seven days a week, personalized guidance fits your schedule and removes the pressure of making irreversible decisions under time constraints.

Final Thoughts

Medicare enrollment decisions made today determine your healthcare access and costs for years ahead. The mistakes outlined in this post-missed deadlines, poor plan selection, and inadequate supplemental coverage-are entirely preventable with the right support. You don’t need to navigate this alone or risk costly errors that compound across decades.

Medicare enrollment help today means connecting with specialists who understand your specific situation rather than treating your enrollment as a generic transaction. We at Dave Silver Insurance examine which doctors you actually see, whether your medications appear on plan formularies, and how income changes will affect your premiums in future years. We identify whether you qualify for Special Enrollment Periods that could recover retroactive coverage and explain what Medicare doesn’t cover-like long-term care costs exceeding $100,000 annually-so you can plan accordingly.

The difference between enrolling with personalized guidance and enrolling alone often amounts to thousands of dollars in unnecessary out-of-pocket costs or coverage gaps that emerge when you need care most. When you’re ready to move forward with confidence, contact Dave Silver Insurance and gain the clarity that transforms enrollment from stressful to straightforward. Your healthcare decisions deserve expert analysis, not guesswork.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation