Medicare costs explained can feel overwhelming, but they don’t have to be. We at Dave Silver Insurance break down exactly what you’ll pay for premiums, deductibles, and out-of-pocket expenses in 2026.

Understanding these costs upfront helps you budget better and avoid surprises. This guide walks you through each component so you can make informed decisions about your coverage.

Medicare Part A and Part B Premiums in 2026

What You Pay for Part A

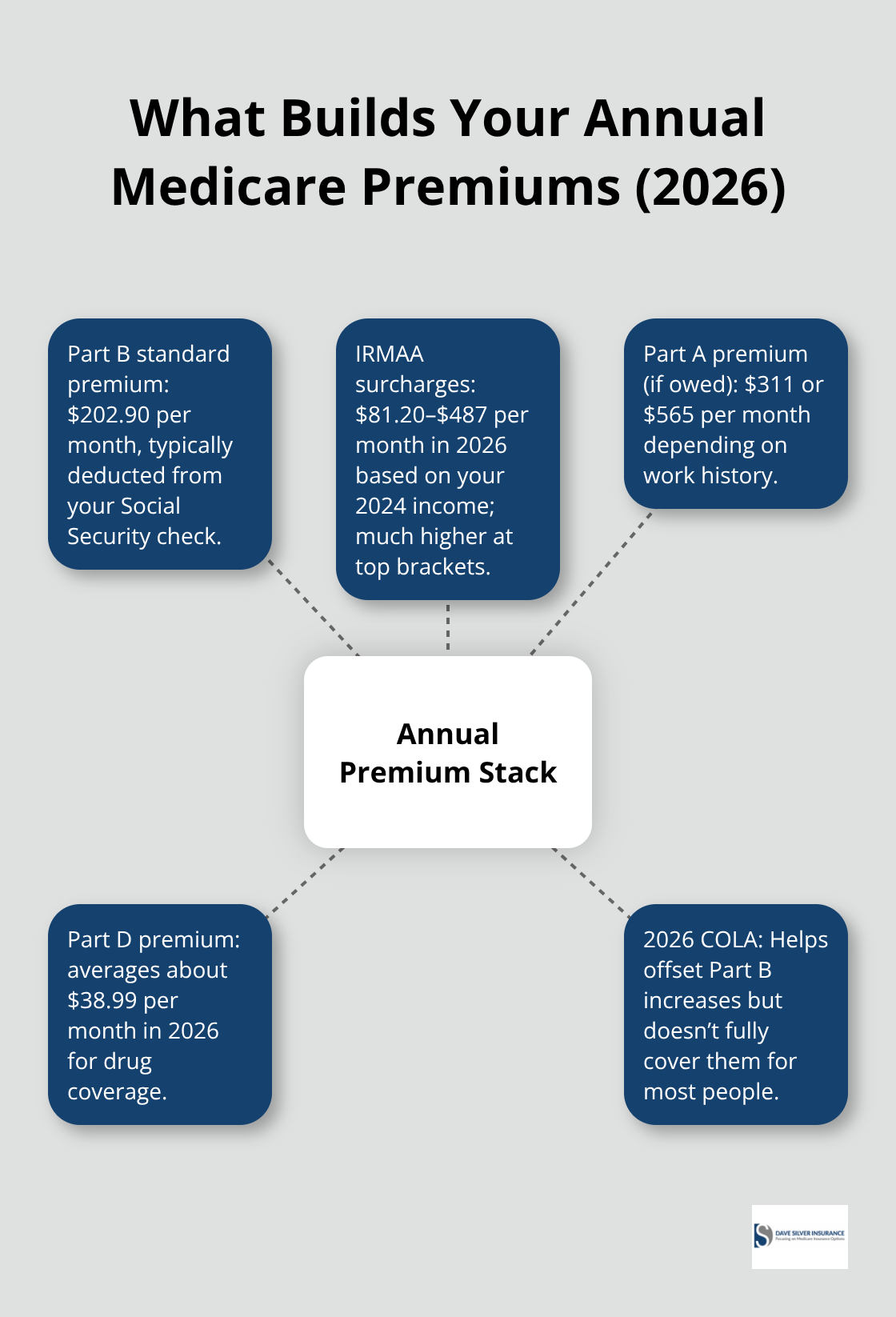

Most people pay $0 for Medicare Part A in 2026 if they or their spouse worked and paid Medicare taxes for at least 10 years, according to Medicare.gov. If you don’t meet that requirement, you’ll pay either $311 or $565 per month depending on your work history. This baseline cost applies regardless of your income level, making Part A relatively straightforward to calculate.

Part B Premiums and Standard Costs

Part B costs $202.90 per month for standard coverage in 2026, and this amount comes directly from your Social Security check each month. You pay this premium even if you don’t use Part B services, so it represents a fixed monthly expense. However, your actual premiums may be significantly higher if your income exceeds certain thresholds set by Medicare.

How IRMAA Increases Your Premiums

Income-Related Monthly Adjustment Amounts (IRMAA) apply to both Part B and Part D if your modified adjusted gross income from 2024 exceeds specific limits. Single filers earning more than $109,000 and joint filers earning more than $218,000 pay extra premiums on top of the standard rates. For Part B, these surcharges range from $81.20 to $487 per month depending on how much your income exceeds the threshold, according to Medicare.gov. If you earned $500,000 or more as a joint filer, you pay nearly $690 monthly for Part B alone. Your 2026 IRMAA is based on your 2024 tax return, so review your income situation now to anticipate what you’ll owe.

Appealing IRMAA After Life Changes

If you experienced a major life event like retirement, job loss, or death of a spouse in 2024 or 2025, you may qualify to appeal your IRMAA with Social Security and potentially reduce your payments. The appeal process varies by situation, so contact Social Security directly to discuss your circumstances. This option can provide meaningful relief if your current income no longer matches your 2024 tax return.

Calculating Your Annual Premium Costs

To estimate your true annual premium cost, multiply your monthly Part B premium by 12 and add any Part A premium if applicable. If you’re subject to IRMAA, add those surcharges to your calculation. Someone earning $150,000 as a single filer might pay $202.90 standard Part B plus an additional $81.20 for IRMAA, totaling roughly $3,408 annually just for Part B. Add a Part A premium if you need one, plus any Part D drug coverage premiums averaging around $38.99 per month, and you’re looking at $4,000 to $5,000 annually before you even pay deductibles or copays. The 2026 Social Security cost-of-living adjustment helps offset some of the Part B increase, but it doesn’t fully cover the rise for most beneficiaries.

These premium costs form only the first layer of your Medicare expenses-deductibles and out-of-pocket limits add substantially to what you’ll actually spend on healthcare.

What Deductibles and Out-of-Pocket Limits Actually Cost You

Part A Hospital Costs Add Up Fast

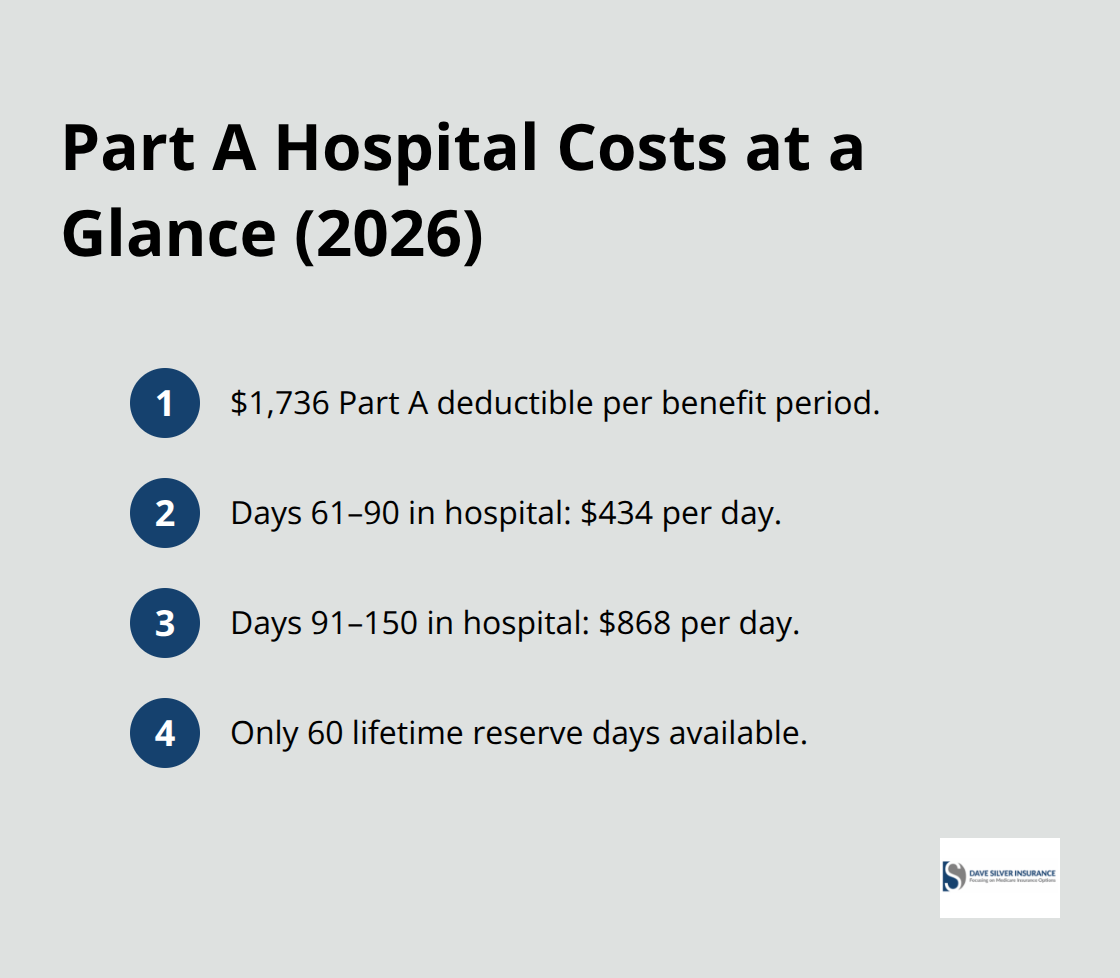

The $1,736 Part A hospital deductible hits you once per benefit period, not once per year, which means you could face this cost multiple times in a single calendar year if you’re hospitalized more than once. After you pay that deductible, your costs continue climbing. Days 61 through 90 of a hospital stay cost $434 per day, and days 91 through 150 cost $868 per day, covering only 60 lifetime reserve days total. This structure punishes longer hospitalizations severely.

A 100-day hospital stay would cost you $1,736 upfront plus $12,420 for days 61 to 90 plus $17,360 for days 91 to 100, totaling $31,516 out of your pocket. These numbers illustrate why extended hospital stays create financial strain for many seniors on fixed incomes.

Part B Deductibles Reset Every Year

Part B adds another layer with its $283 annual deductible, after which Medicare covers 80 percent of approved services and you cover 20 percent. Unlike Part A, this deductible resets every calendar year, so January brings a fresh $283 obligation. A single specialist visit costing $500 means you pay $283 toward the deductible plus 20 percent of the remaining $217, landing you $326 in total costs for that one visit.

Original Medicare Offers No Annual Spending Cap

Original Medicare offers no annual out-of-pocket maximum, which distinguishes it fundamentally from Medicare Advantage plans. You could theoretically face unlimited costs under Parts A and B combined. Someone with a chronic condition requiring frequent specialist visits, imaging, and procedures could easily spend $5,000, $10,000, or more annually without supplemental coverage. This unlimited exposure creates real financial risk for beneficiaries managing multiple health conditions.

Medigap and Part C Provide Spending Limits

Medigap insurance exists precisely to address this gap. A high-deductible Medigap plan carries a $2,950 annual deductible in 2026 but then covers most remaining costs, capping your exposure. Medicare Advantage plans establish clear out-of-pocket limits at $9,250 maximum for in-network care in 2026, providing predictable spending caps that Original Medicare simply does not offer. The trade-off involves network restrictions and prior authorization requirements that Original Medicare doesn’t impose.

Part D Drug Costs Cap at $2,100

Part D prescription drug coverage adds another $2,100 annual out-of-pocket cap once you reach that threshold, after which covered drugs cost nothing for the remainder of the year. Understanding these separate deductibles and limits requires calculating your realistic healthcare spending across all components rather than viewing them in isolation. The interaction between Part A, Part B, Part D, and any supplemental coverage you select determines your true annual financial exposure. Choosing the right combination of coverage becomes essential when you recognize how quickly these costs accumulate.

How Medigap and Medicare Advantage Cut Your Costs

Medigap Policies Wrap Around Original Medicare

Medigap insurance, sold by private insurers, wraps around Original Medicare to cover deductibles, coinsurance, and copays that Medicare doesn’t pay. A Medigap Plan G covers the $1,736 Part A hospital deductible, the $283 Part B deductible, and 20 percent coinsurance on most services after you meet those deductibles. Plan G premiums for a 65-year-old nonsmoker in many regions run roughly $122 to $200 monthly depending on location and insurer. If you face a $100,000 hospital stay, your Part A deductible of $1,736 and subsequent coinsurance would normally cost thousands out of pocket. With Plan G, you pay that monthly premium instead of facing those massive bills.

The math favors Medigap when you anticipate frequent medical care or chronic conditions requiring specialist visits. However, Medigap policies require enrollment during your six-month open enrollment window starting when you turn 65 and enroll in Part B. Miss that window and insurers can deny coverage or charge higher premiums based on health status. You also cannot hold both Medigap and Medicare Advantage simultaneously, so the choice locks you into one path.

Medicare Advantage Plans Replace Original Medicare

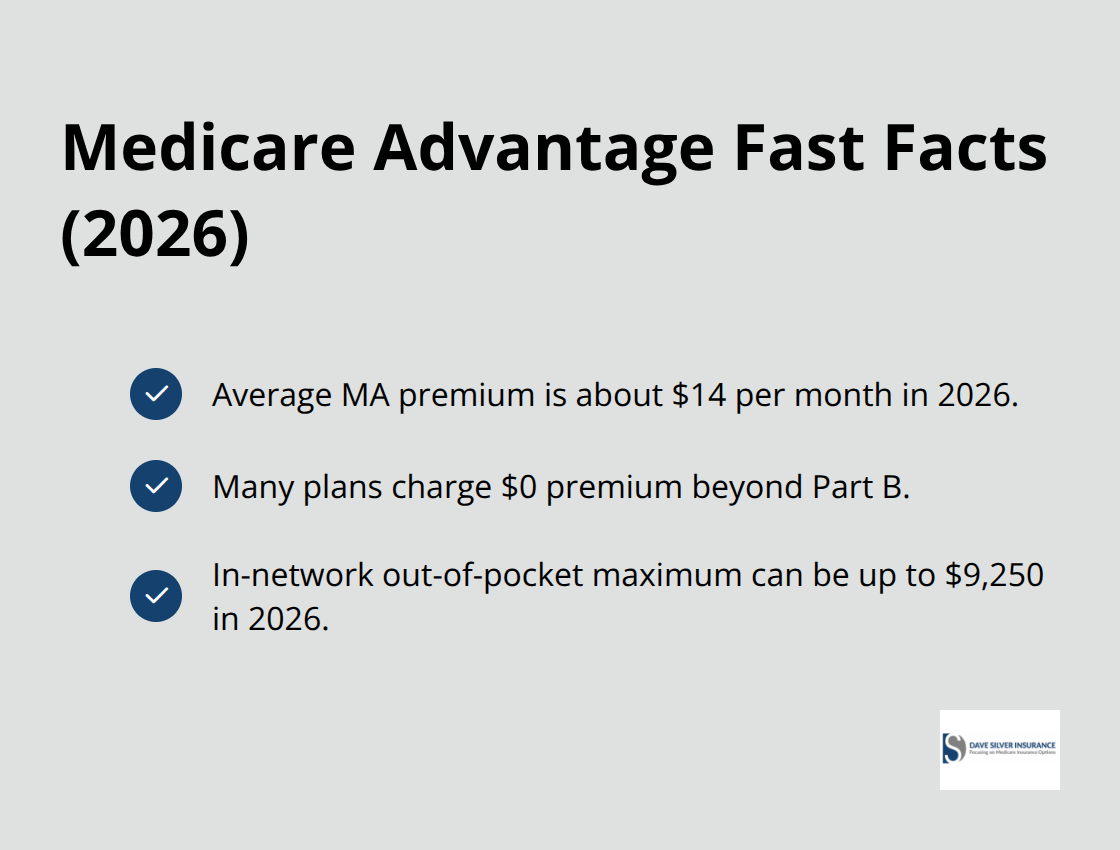

Medicare Advantage (Part C) plans take a different route by replacing Original Medicare entirely with private insurance that covers Parts A, B, and usually D combined. The average Medicare Advantage premium sits around $14 monthly in 2026, with many plans charging zero premium beyond your mandatory Part B payment. Medicare Advantage plans establish a maximum out-of-pocket limit for in-network care in 2026, meaning once you hit that spending threshold, the plan pays 100 percent of covered services for the remainder of the calendar year.

Many plans include dental, vision, and hearing benefits that Original Medicare doesn’t cover, adding real value for beneficiaries managing multiple health needs. The trade-off involves network restrictions and prior authorization requirements that Original Medicare avoids. If your preferred doctor doesn’t participate in the plan’s network, you face higher costs or must switch providers.

Comparing Spending Under Each Approach

A person with a $5,000 annual healthcare budget faces different decisions under each approach. Under Medigap with Original Medicare, you pay premiums plus your Part A and B deductibles plus 20 percent coinsurance on covered services. Under Medicare Advantage, you pay a lower or zero premium, then pay nothing else for covered in-network care once you reach your out-of-pocket maximum. For moderate to high healthcare spenders, that cap provides predictability that Original Medicare cannot match.

The right choice depends entirely on your health situation and network preferences, not on which option sounds cheaper in isolation. We at Dave Silver Insurance provide personalized guidance comparing both options based on your specific doctors, prescriptions, and anticipated healthcare needs rather than pushing one solution universally.

Final Thoughts

Medicare costs explained requires you to assess your personal health situation rather than chase the lowest premium. Your choice between Original Medicare with Medigap versus Medicare Advantage hinges on your actual doctors, prescriptions, and anticipated healthcare spending patterns. Start by reviewing your 2024 tax return to calculate your IRMAA exposure, list your current doctors and medications, then compare the total annual cost of each option including premiums, deductibles, and out-of-pocket maximums.

We at Dave Silver Insurance help you navigate these decisions with personalized guidance tailored to your specific health and financial situation. Our team works with you to identify which combination of Medicare Part A, B, C, and D coverage plus any supplemental insurance reduces your out-of-pocket expenses most effectively. Contact Dave Silver Insurance to review your coverage options and build a Medicare plan that fits your budget and healthcare needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation