Medicare costs explained can feel overwhelming, but they don’t have to be. Most seniors we work with at Dave Silver Insurance struggle to understand where their money goes each month.

This guide breaks down every cost you’ll face, from premiums to copayments. You’ll learn which expenses you can control and which ones are fixed.

What You Actually Pay for Part A and Part B

Part A Premiums and Hospital Deductibles

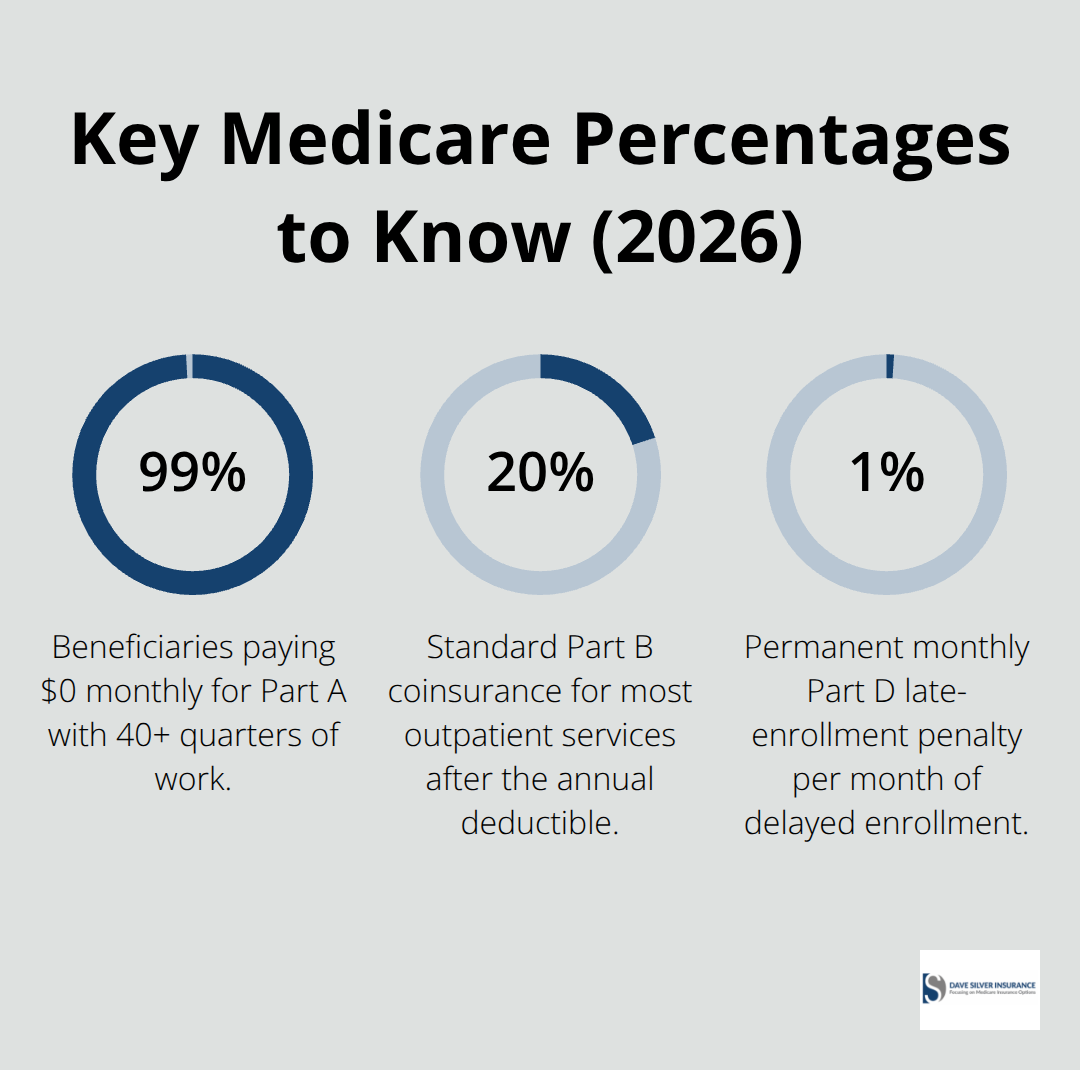

About 99% of Medicare beneficiaries pay $0 monthly for Part A because they have at least 40 quarters of work history, according to CMS data. However, Part A still carries significant costs when you need hospital care. The Part A inpatient hospital deductible is $1,736 per benefit period in 2026, and you can incur this deductible multiple times in a single year if separate hospitalizations occur. Days 1 through 60 of hospitalization cost nothing after you meet the deductible, but days 61 through 90 cost $434 daily, and days 91 through 150 cost $868 daily. These daily costs accumulate quickly for extended hospital stays.

Part B Premiums and the Annual Deductible

Part B costs $202.90 per month in 2026, and this amount increases if your income exceeds certain thresholds. The Part B deductible sits at $233 annually, meaning you pay this amount out of your own pocket before Medicare starts covering services. After you hit the deductible, you typically owe 20% coinsurance for doctor visits, lab work, and most outpatient services. This coinsurance structure means your actual costs depend entirely on how much care you use that year. A senior with minimal medical needs might only pay the deductible and premium, while someone managing chronic conditions could face thousands in coinsurance charges.

How Income Changes Your Part B Costs

If your modified adjusted gross income exceeds $97,000 as a single filer or $194,000 as a married couple filing jointly, you’ll pay more than the standard Part B premium. This income-related monthly adjustment amount, called IRMAA, can add anywhere from $63 to $76.40 monthly to your Part B bill in 2026. The CMS applies IRMAA based on your tax return from two years prior, which catches many seniors off guard. You might have received a large inheritance, sold a home, or had investment income that pushed you into a higher bracket without realizing it would affect Medicare costs. If your life circumstances change significantly, you can request a reduction in IRMAA by contacting Social Security with documentation of your income decrease.

Skilled Nursing Facility Costs After Hospitalization

Skilled nursing facility care, which many seniors need after surgery or illness, charges $217 per day for days 21 through 100. If you stay in a nursing facility for 100 days, you’ll pay $17,360 out of pocket, even though Medicare helps with costs. The key is understanding that Medicare Part A doesn’t mean free hospital care-it means you’re insured against catastrophic costs, but you’re still responsible for significant amounts depending on the length of stay. These expenses often surprise seniors who assume Part A covers everything once they’ve met the deductible.

These Part A and Part B costs form only the beginning of your Medicare expenses. Part C and Part D introduce additional options and costs that can either reduce or increase your overall spending, depending on which plans you select and how you use them.

Part C and Part D: Where Your Real Choices Begin

Medicare Advantage Plans and Out-of-Pocket Limits

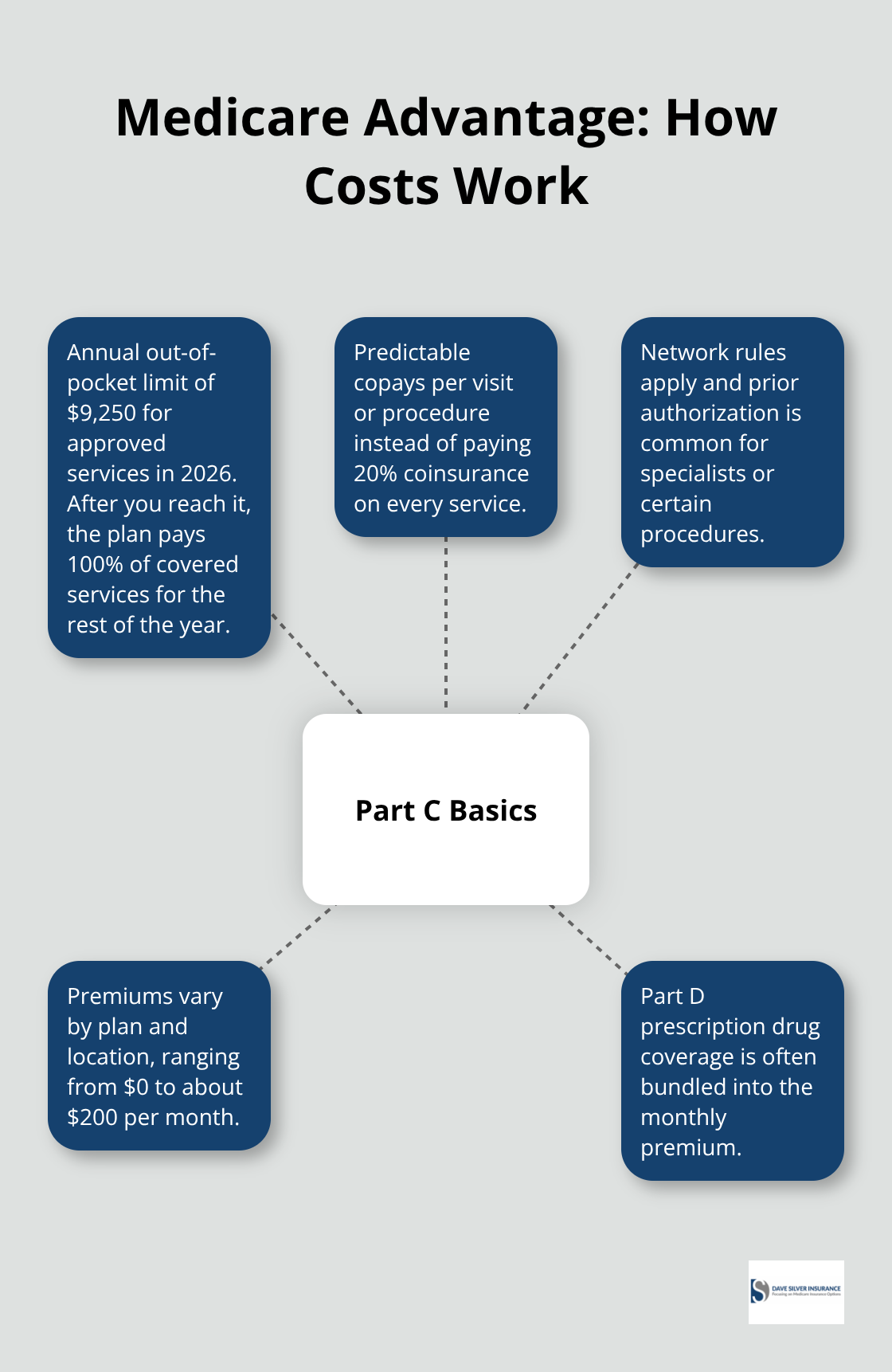

Medicare Advantage plans (Part C) fundamentally change how you pay for coverage. Instead of paying 20% coinsurance for every service, you pay a fixed amount per visit or procedure, and more importantly, your out-of-pocket costs have a yearly cap. In 2026, once you hit your plan’s out-of-pocket limit-$9,250 for approved services-Medicare pays 100% of covered services for the rest of that year. This ceiling doesn’t exist in Original Medicare unless you buy Medigap, which costs extra.

Network Restrictions and Plan Premiums

Most Medicare Advantage plans include Part D drug coverage in their monthly premium, so you don’t pay a separate drug plan fee. However, this convenience comes with a tradeoff: you must use doctors and hospitals within the plan’s network, and many plans require prior authorization before you can see specialists or get certain procedures. The monthly premium for Medicare Advantage varies dramatically by plan and location. Some plans charge $0 premium but make money through higher copayments and deductibles, while others charge $50 to $200 monthly with lower out-of-pocket costs.

Choosing Medicare Advantage Based on Your Health Needs

The real decision hinges on your health situation. If you take multiple prescription drugs or anticipate hospital stays, the out-of-pocket cap in Medicare Advantage often saves you thousands annually compared to Original Medicare with 20% coinsurance everywhere. Your prescription drug needs and expected medical utilization should drive your plan selection, not the lowest advertised premium.

Part D Drug Plans and Coverage Gaps

Part D drug plans operate separately from Medicare Advantage, though most Advantage plans bundle them in. If you choose Original Medicare, you must enroll in a standalone Part D plan or face a penalty of roughly 1% per month of delay, applied permanently to your premiums. Part D premiums vary from $5 to $100+ monthly depending on the plan and your income level.

The plan structure includes a deductible (usually $100 to $500), then you pay a percentage of drug costs until you reach the plan’s coverage gap threshold, around $6,500 in total drug spending. Inside the gap, you pay higher percentages for each drug. Once your out-of-pocket spending hits roughly $8,000, catastrophic coverage kicks in and you pay minimal amounts. Income-related adjustments apply to Part D just like Part B, so higher earners pay substantially more.

Comparing Specific Medications During Open Enrollment

When comparing plans during annual Open Enrollment, focus on the drugs you actually take, not the lowest premium. A plan charging $15 monthly might exclude your blood pressure medication while another at $45 monthly covers it with a $5 copay. Use the plan comparison tool on Medicare.gov to see exact costs for your specific medications before enrolling. The difference between plans can easily exceed $1,000 annually per person.

These Part C and Part D decisions set the foundation for your overall Medicare spending strategy, but they represent only part of your total healthcare costs. Hidden expenses-copayments, coinsurance, and services Medicare doesn’t cover at all-often catch seniors off guard and can add thousands to your annual bills.

What Medicare Doesn’t Pay For

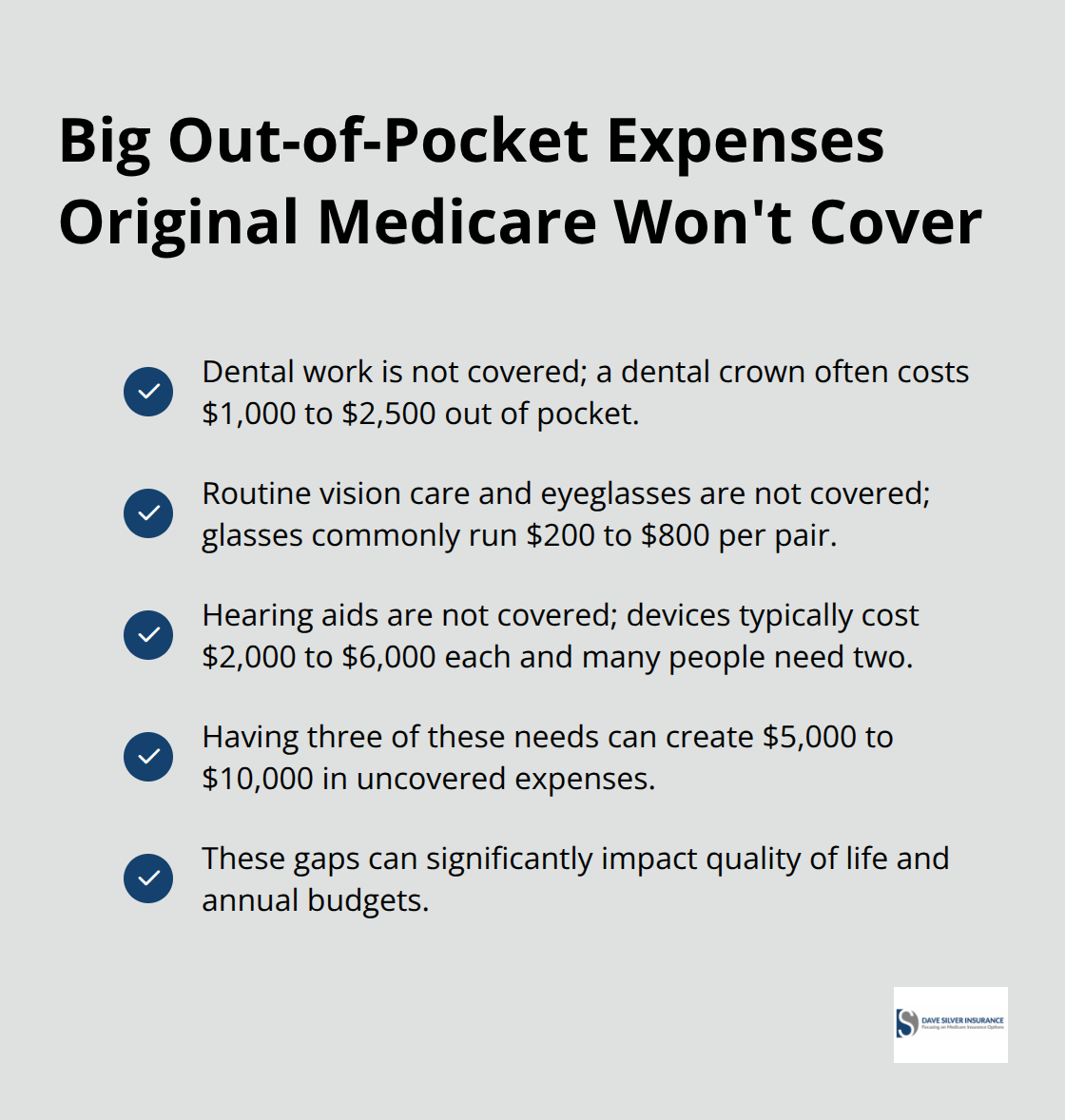

Most seniors discover too late that Medicare has significant coverage gaps, and these gaps create real out-of-pocket expenses that add up quickly. Dental work, vision care, and hearing aids aren’t covered by Original Medicare, yet these services affect your quality of life and overall health. A dental crown costs $1,000 to $2,500 out of pocket. Eyeglasses run $200 to $800 per pair. Hearing aids cost $2,000 to $6,000 each, and you typically need two. If you have three of these common needs, you’re looking at $5,000 to $10,000 in uncovered expenses that Medicare won’t touch.

This reality catches most seniors off guard, especially those who assumed Medicare covers everything at age 65.

Uncovered Services That Drain Your Savings

Beyond the big three uncovered services, you’ll face copayments and coinsurance that vary depending on your plan choice. If you use Original Medicare, you pay 20% coinsurance for most services after meeting your $283 Part B deductible. That means a specialist visit costing $200 nets you a $40 bill, but an MRI at $1,200 means $240 out of pocket. These percentages compound across multiple visits and procedures throughout the year.

How Plan Type Affects Your Out-of-Pocket Exposure

Medicare Advantage plans cap your annual out-of-pocket spending at $9,250 for in-network services, which protects you from catastrophic costs but only if you stay within the network. The moment you go out of network without authorization, you face much higher bills or no coverage at all. The difference between Original Medicare and Medicare Advantage becomes starkest when you add up these coinsurance amounts across a full year of medical care.

Someone managing diabetes, arthritis, and hypertension might easily spend $3,000 to $5,000 annually in coinsurance with Original Medicare, whereas a Medicare Advantage plan caps exposure at the plan’s out-of-pocket limit. This is why plan selection matters far more than choosing based on the lowest monthly premium advertised.

Medigap Closes the Gaps Original Medicare Creates

Medigap insurance, also called Medicare Supplement Insurance, directly addresses these out-of-pocket costs by covering the 20% coinsurance you’d otherwise owe. A Medigap Plan G or Plan N covers most of your coinsurance, deductibles, and copayments, transforming your financial exposure from potentially thousands annually into predictable monthly premiums. Medigap Plan G costs between $100 and $250 monthly depending on your age and location, but it eliminates that 20% coinsurance on every service.

The math works in your favor if you use healthcare regularly. Someone paying $1,800 yearly for Medigap but saving $4,000 in coinsurance comes out $2,200 ahead. However, Medigap only works with Original Medicare, not Medicare Advantage, so you must choose one path or the other.

Why You Can’t Mix Medigap with Medicare Advantage

You cannot use Medigap to reduce out-of-pocket costs under a Medicare Advantage plan because the plans operate under different structures. If you have a Medicare Advantage plan and want supplemental coverage, you’re limited to specific state programs or employer coverage, which most retirees don’t have access to. This constraint makes your initial plan choice genuinely important because switching later becomes complicated and expensive.

Final Thoughts

Your Medicare costs explained comes down to three annual decisions made during Open Enrollment. Choose between Original Medicare with Medigap or a Medicare Advantage plan based on your actual prescription drugs and expected medical needs, not the lowest advertised premium. Then select a Part D drug plan by checking your specific medications against each plan’s formulary and copayments, and decide whether Medigap makes financial sense by calculating your expected coinsurance against the monthly premium cost.

Review your current coverage immediately, as plans from three years ago likely no longer match your health situation or prescription needs. Costs change annually, plan networks shift, and your medications may have moved to different tiers. Spending two hours comparing plans during Open Enrollment can save you thousands annually through Medicare.gov’s plan comparison tool, where you enter your specific drugs and see exact out-of-pocket costs before enrolling.

Investigate whether you qualify for Medicare Savings Programs or Extra Help for prescription drugs, as roughly half of eligible people never enroll despite these programs helping low-income seniors pay premiums, deductibles, and copayments. Contact your state Medicaid office to check eligibility, and schedule a consultation with us at Dave Silver Insurance to receive personalized recommendations backed by our expertise in Medicare regulations and plan details. Our team works with you seven days a week to review your health needs, medications, and financial situation, then recommend the specific plans that minimize your out-of-pocket costs while maintaining access to your doctors.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation