Turning 65 brings a major decision: choosing the right Medicare coverage. The process can feel overwhelming with multiple parts, enrollment deadlines, and coverage options to evaluate.

At Dave Silver Insurance, we’ve helped thousands of retirees navigate Medicare for retirees without confusion or costly mistakes. This guide breaks down everything you need to know to make confident decisions about your health coverage.

When Should You Enroll in Medicare

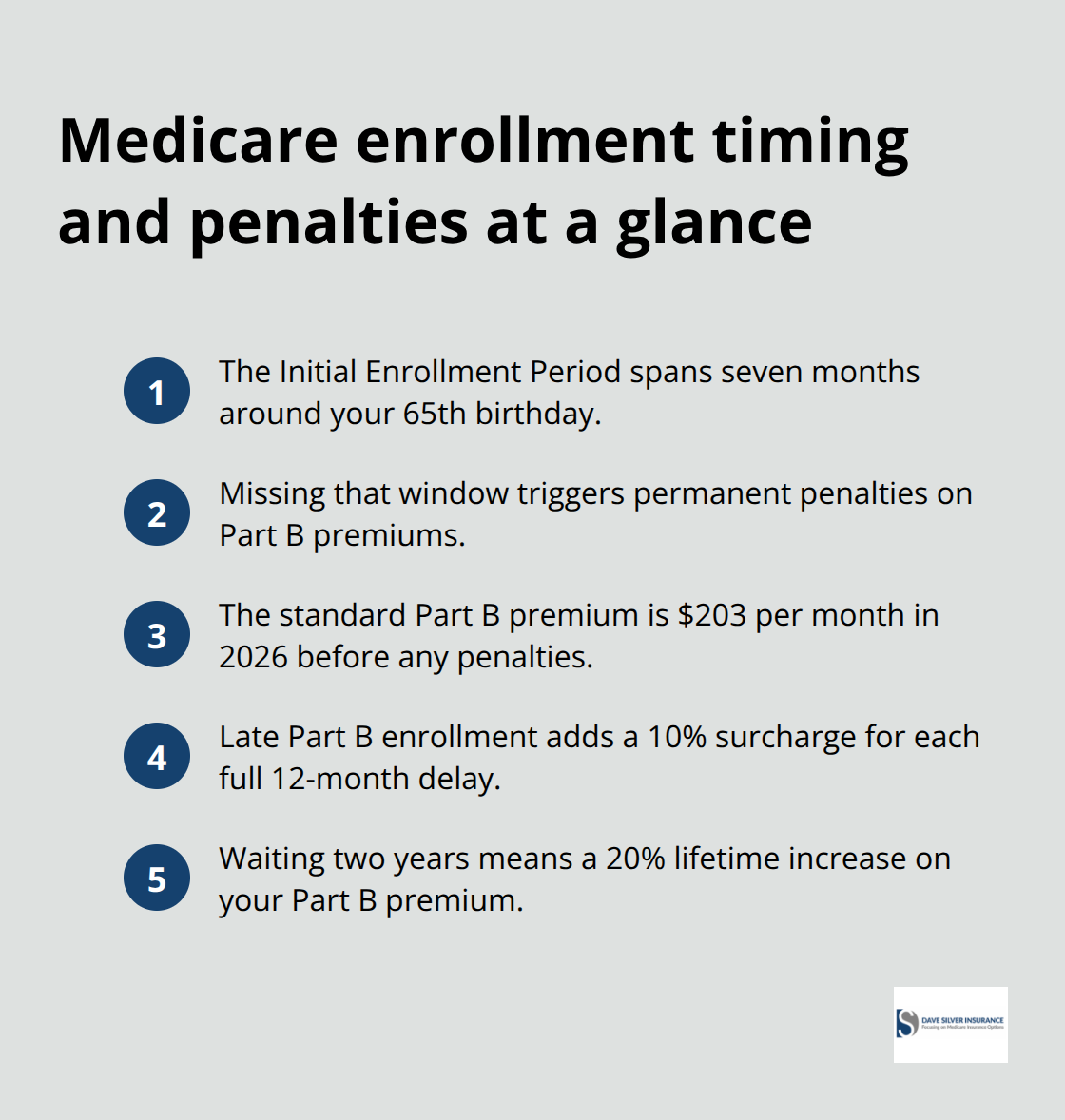

Medicare eligibility begins the month you turn 65, and this is where timing becomes critical. You have a seven-month window called your Initial Enrollment Period that spans three months before your 65th birthday, the month you turn 65, and three months after. Missing this window triggers permanent penalties that follow you for life. The standard Part B premium for 2026 is $203 per month, but if you enroll late without qualifying for a Special Enrollment Period, you pay an additional 10% penalty for each 12-month period you delayed. Waiting just two years costs you a 20% premium increase forever.

Part D Penalties Add Up Quickly

For Part D prescription drug coverage, the penalty is 1% of the national base beneficiary premium for each month you go without creditable coverage. Unlike Part B, this penalty resets each year but compounds if you stay uninsured. Someone who waits three years to enroll faces hundreds in additional annual costs. These penalties stick with you, making early enrollment far less expensive than playing catch-up later.

Special Enrollment Periods Create Second Chances

Your Initial Enrollment Period is your best opportunity, but life circumstances can create additional windows. A Special Enrollment Period applies if you lose employer coverage, move to a new state, or experience other qualifying events like loss of Medicaid. You get two months from when your coverage ends to enroll without penalties. The Annual Enrollment Period runs October 15 through December 7 each year, allowing beneficiaries already on Medicare to switch plans.

Retiree Coverage Requires Immediate Action

If you have retiree coverage from a former employer, contact your benefits administrator immediately. They must tell you annually whether your drug coverage is creditable, meaning it provides the same value as Medicare Part D. If your retiree coverage is creditable, you can skip Medicare drug enrollment without penalty, but this decision affects your long-term costs and coordination with Medicare. Many retirees assume employer coverage continues seamlessly into retirement-it does not. When you turn 65, you typically must enroll in Medicare Part A and Part B to receive full benefits from your retiree coverage. Delaying this enrollment can cause your retiree plan to stop paying costs during Medicare-eligible periods, leaving you exposed to thousands in unexpected bills.

Understanding these enrollment windows and deadlines shapes your entire Medicare experience. The next section walks you through each Medicare part and what you actually pay for coverage.

What Do Medicare Parts A, B, C, and D Actually Cover

Part A and Part B: The Foundation of Original Medicare

Medicare Part A covers inpatient hospital stays, skilled nursing facility care after hospitalization, and hospice services. You pay no monthly premium for Part A if you or your spouse paid Medicare taxes for at least 10 years, but you face a $1,736 hospital deductible in 2026 for each benefit period. Part B covers physician visits, outpatient services, diagnostic tests, and preventive care, costing $202.90 per month in 2026 with a $283 annual deductible plus 20% coinsurance on most services.

Together, Part A and Part B form Original Medicare, which gives you broad access to providers nationwide but leaves significant cost-sharing gaps. A serious illness or injury can drain thousands from your savings fast when you factor in the 2026 hospital deductible and Part B coinsurance.

Medicare Advantage: Bundled Coverage with Built-In Limits

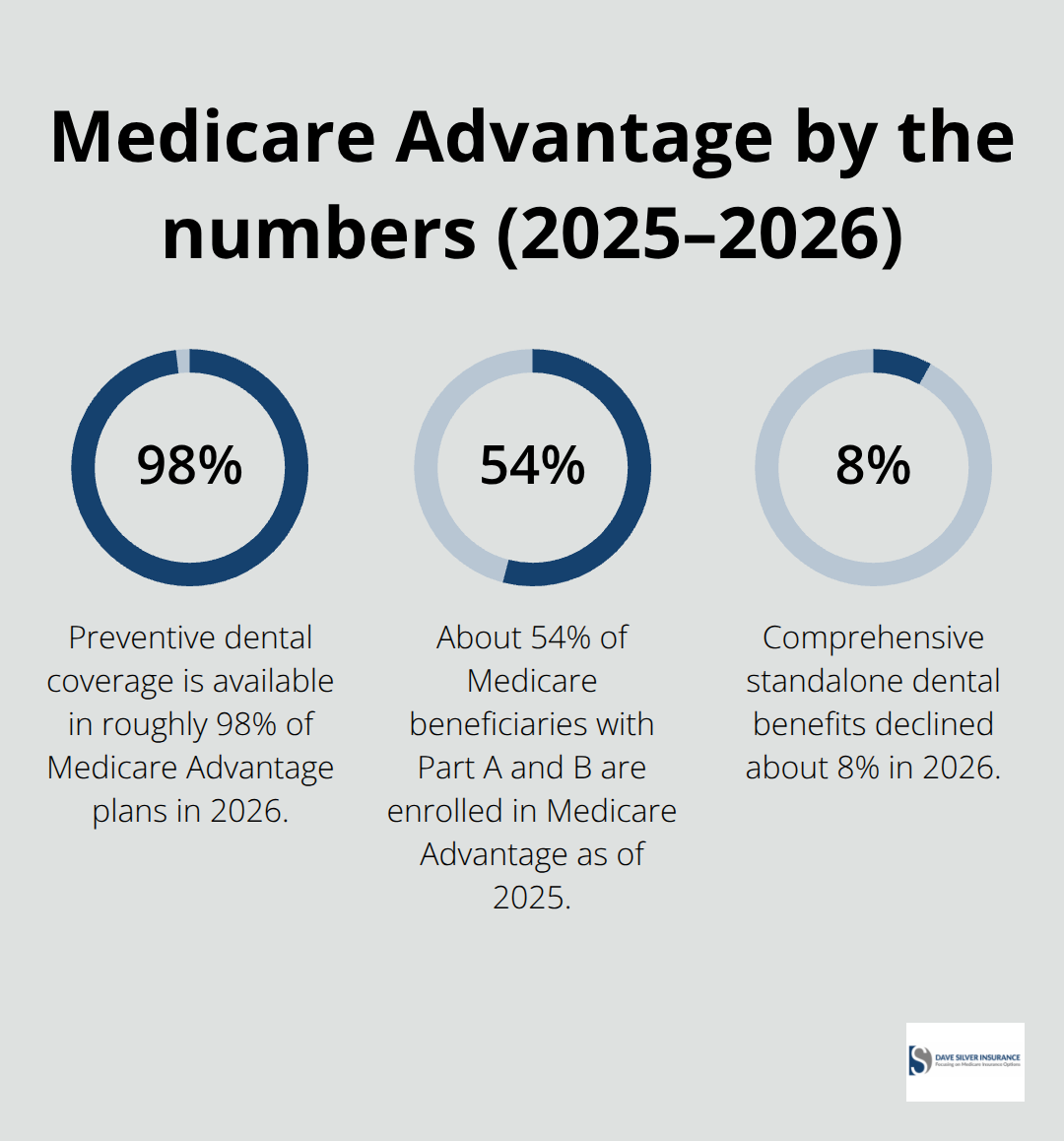

Part C, also called Medicare Advantage, bundles Part A and Part B coverage into a single managed care plan offered by private insurers. These plans include an annual out-of-pocket spending cap, capping your total costs at a set limit each year. In 2026, a large majority of Medicare Advantage plans cover dental, vision, and hearing benefits, with preventive dental coverage available in roughly 98% of plans.

However, these supplemental benefits come with limits and may not cover everything you need. Comprehensive standalone dental benefits declined about 8% in 2026, while vision hardware limits fell roughly 15%, signaling tighter coverage. Medicare Advantage limits your network to specific providers and typically requires referrals for specialists, but the annual out-of-pocket cap provides predictability. About 54% of Medicare beneficiaries with Part A and B are enrolled in Medicare Advantage as of 2025, totaling 34.1 million people.

Part D: Prescription Drug Coverage and Penalty Costs

Part D covers prescription drugs and works with Original Medicare or Medicare Advantage. If you skip Part D enrollment without creditable coverage from an employer or retiree plan, you face a permanent 1% monthly penalty on your premiums each year you go uninsured. The 2026 national base beneficiary premium for Part D is around $34.70 monthly, meaning three years of delayed enrollment could add $1,250 or more to your lifetime drug costs.

Coordinating Coverage with Retiree Plans

If you have retiree coverage from a former employer, coordinate carefully with Medicare. Medicare pays first after you turn 65, then your retiree plan covers remaining costs according to plan rules. Many retiree plans cap your out-of-pocket costs or cover specific gaps like coinsurance, but details vary dramatically by plan.

Contact your benefits administrator to obtain your plan’s benefit booklet and understand exactly how your retiree coverage coordinates with Medicare Parts A and B. Some retiree plans offer extra hospital days not covered by Medicare or start paying out-of-pocket costs only after you meet a maximum. This coordination matters tremendously because enrolling in Medicare Part D might cause you to lose retiree drug coverage entirely, fundamentally changing your total costs. Before deciding between Medicare drug coverage and creditable retiree drug coverage, check whether switching triggers loss of other retiree health benefits for you or your dependents.

Filling Gaps with Medigap Insurance

Original Medicare often leaves you vulnerable to catastrophic costs since it offers maximum provider choice but no annual cost cap. Those choosing Original Medicare frequently add Medigap supplemental insurance to cover cost-sharing gaps, with roughly 43% of traditional Medicare beneficiaries holding a Medigap policy in 2023. Average Medigap premiums run around $2,600 annually according to KFF data.

Your coverage choice fundamentally shapes your out-of-pocket expenses and provider flexibility. The decision between Original Medicare with Medigap, Medicare Advantage, or coordination with retiree coverage depends on your health needs, budget, and provider preferences. Understanding these options positions you to evaluate which supplemental coverage strategy works best for your situation.

Medigap Fills the Gaps Original Medicare Leaves Behind

Original Medicare covers broad services but exposes you to serious out-of-pocket costs that catch many retirees off guard. The 2026 hospital deductible of $1,736 hits immediately when you’re admitted, and then you pay 20% coinsurance on virtually every doctor visit, test, and procedure after that. There’s no annual spending cap in Original Medicare, meaning a major health event or chronic condition can drain tens of thousands from your savings. Medigap policies step in to address this vulnerability. Roughly 43% of traditional Medicare beneficiaries hold a Medigap policy according to KFF data from 2023, and they do so because the math works. Average Medigap premiums run around $2,600 annually, but they predictably cover the cost-sharing gaps that would otherwise be unpredictable and catastrophic.

Medigap policies coordinate directly with Medicare: Medicare pays first based on its rules, then your Medigap policy pays the remaining balance according to your specific plan design. If you have retiree coverage from a former employer, a Medigap policy works alongside your retiree plan in the same way, with Medicare paying first, then your retiree coverage and Medigap filling gaps. The critical detail most retirees miss is that you generally need both Medicare Part A and Part B to purchase a Medigap policy at all. If you don’t buy within six months of first getting Part A and Part B, you may lose the right to purchase later or face substantially higher premiums due to medical underwriting.

Your Six-Month Enrollment Window Determines Your Options

Your Medigap enrollment window is narrow and expensive to miss. The six-month window following your Part B enrollment start date is your guaranteed issue period, meaning insurers cannot reject you or charge more based on your health history. Wait beyond six months and insurers can impose waiting periods for pre-existing conditions or simply deny your application entirely. The State Health Insurance Assistance Program offers free personalized advice on whether a Medigap policy makes sense for your situation; contact your local SHIP office through shiphelp.org to discuss your specific health and financial circumstances.

During your enrollment window, compare the standardized Medigap plans available in your state. Plans are labeled A through N, and each letter represents identical coverage regardless of which insurer sells it, so your decision focuses purely on price and insurer reliability. Some plans cover the Part B deductible entirely, others cover it partially, and a few cover nothing. Most plans cover 100% of Part B coinsurance, which is where your true savings emerge over time.

How Medicare and Medigap Claims Work Together

The coordination between Medicare and Medigap is straightforward. You submit claims to Medicare first, then your Medigap insurer automatically receives the claim information and pays its portion directly to the provider or to you. This removes the administrative burden of managing multiple claim submissions yourself. The process happens behind the scenes, so you experience seamless coverage without tracking separate claim deadlines or submission requirements.

Calculate Total Annual Costs, Not Just Monthly Premiums

The monthly premium matters less than total annual costs when comparing Medigap plans. A plan with a lower monthly premium might carry a higher deductible, which means you pay more out-of-pocket before coverage kicks in. Calculate your expected annual costs by estimating how many doctor visits you’ll have, any anticipated procedures, and prescription drugs you’ll need. If you’re relatively healthy with minimal provider visits, a plan with higher deductibles and lower premiums might save money. If you have chronic conditions requiring frequent care, paying more monthly for comprehensive coverage typically costs less overall.

Some Medigap insurers offer discounts for paying annually instead of monthly, which can reduce your total premium cost by 5-10%. Shop rates across multiple insurers because the same Medigap plan letter can vary significantly in price between companies in your state. An insurer charging $150 monthly for Plan G in your area might be substantially more or less expensive than competitors offering identical coverage. The enrollment period is your leverage point: use it to get quotes from at least three insurers before deciding. After your six-month guaranteed issue period ends, switching to a different plan or insurer becomes medically underwritten, meaning pre-existing conditions can affect approval and pricing.

Final Thoughts

Medicare for retirees demands careful planning, but the fundamentals are straightforward once you understand the pieces. Your enrollment window determines whether you pay penalties for life, your coverage choice shapes your annual costs, and your supplemental strategy protects you from catastrophic expenses. The 2026 hospital deductible of $1,736 combined with 20% coinsurance on most services proves that Original Medicare alone leaves you vulnerable.

Start by contacting your benefits administrator if you have retiree coverage, since coordinating that coverage with Medicare Part A and B prevents you from losing benefits when you turn 65. Gather your plan documents and understand whether your drug coverage is creditable before the Annual Enrollment Period arrives. If you’re choosing Original Medicare, apply for Medigap within six months of your Part B start date to lock in guaranteed issue rates and avoid medical underwriting that could deny coverage or charge substantially more.

Missing your Initial Enrollment Period triggers permanent penalties, delaying Medigap enrollment beyond six months can result in rejection or higher premiums, and failing to coordinate with retiree coverage can cause your employer plan to stop paying costs during Medicare-eligible periods. Dave Silver Insurance brings over 17 years of Medicare expertise to simplify your enrollment process and provide personalized guidance on Medicare Parts A, B, C, and D, plus Medigap strategies tailored to your unique health and financial circumstances.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation