Medicare Part C coverage offers a different approach to health insurance than Original Medicare. These plans, also called Medicare Advantage, combine hospital and medical coverage with prescription drug benefits in one package.

At Dave Silver Insurance, we know that choosing between Medicare options can feel overwhelming. This guide walks you through what Part C actually covers, how costs work, and whether it’s the right fit for your situation.

How Medicare Part C Actually Works

[Medicare Advantage (Part C) operates fundamentally differently from Original Medicare because private insurers manage the plans rather than the federal government. These private companies receive a fixed monthly payment from Medicare to cover your hospital care, doctor visits, and typically prescription drugs all in one integrated package. As of February 2026, 35.1 million people enrolled in Medicare Advantage according to Kaiser Family Foundation data, representing more than half of all Medicare beneficiaries. The appeal is straightforward: instead of juggling Original Medicare plus separate Medigap and Part D policies, you get comprehensive coverage bundled together. However, this convenience comes with trade-offs that matter for your actual healthcare experience.

Network Limitations Shape Your Doctor Access

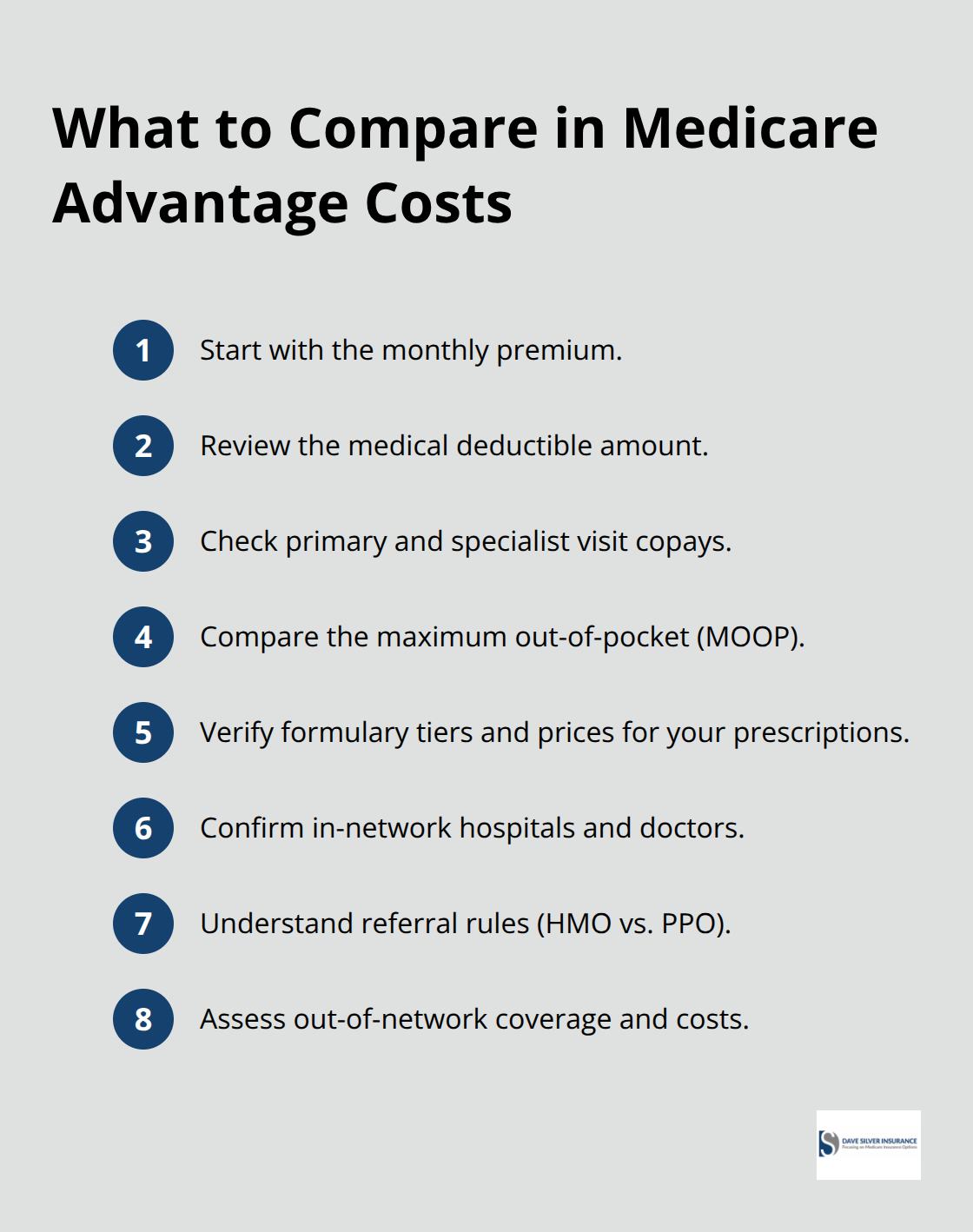

Part C plans operate with defined provider networks, and this is where theory meets reality. Kaiser Family Foundation research shows that Medicare Advantage enrollees have access to roughly half the physicians available to Traditional Medicare beneficiaries in their area. This isn’t just a number on paper-it affects which doctors you can see without paying out-of-network rates. Before you enroll in any Part C plan, you must verify that your current doctors and preferred hospitals participate in that specific plan’s network. Many people discover mid-year that their longtime specialist isn’t covered, forcing them to switch providers or pay significantly higher costs. The official Medicare Plan Finder lets you check network participation by entering your ZIP code, which displays all available plans and their participating providers in your area. This step is non-negotiable.

Out-of-Pocket Costs Have Built-In Protections

Unlike Original Medicare, Part C plans include an annual out-of-pocket maximum. Once you hit this cap (which varies by plan), you pay nothing for covered services for the remainder of that calendar year. This protection doesn’t exist in Original Medicare, where costs can accumulate indefinitely. However, the trade-off is that individual copayments and deductibles for Part C tend to be higher than Original Medicare for specific services. A doctor visit might cost $25 under one plan but $40 under another, even within the same geographic area. When you evaluate plans, comparing maximum out-of-pocket costs matters more than focusing solely on monthly premiums. A plan with a lower premium might saddle you with higher deductibles and copayments, making the total yearly cost substantially more expensive if you need regular medical care.

How Prescription Drug Coverage Integrates Into Part C

Most Medicare Advantage plans bundle prescription drug coverage directly into the plan, eliminating the need to purchase a separate Part D policy. This integration simplifies your coverage structure, but it also means you must verify that your specific medications appear on that plan’s formulary before you enroll. The formulary list shows which drugs the plan covers and at what cost tier-some medications cost less than others depending on the plan’s negotiated rates. If your current medications aren’t covered or fall into expensive tiers, that plan becomes significantly more costly for you. You should compare formularies across multiple plans in your area to find the option that covers your prescriptions at the lowest out-of-pocket cost. This comparison directly impacts your total healthcare expenses throughout the year.

Extra Benefits Vary Significantly Across Plans

Part C plans frequently offer benefits that Original Medicare doesn’t cover, such as routine dental care, vision exams, hearing aids, and fitness program memberships. These extras can add substantial value to your coverage, but availability and scope differ dramatically from plan to plan. One plan might cover dental cleanings and X-rays at no cost, while another covers only limited preventive care. Vision benefits might include glasses or contacts under one plan but not under another. Fitness benefits like SilverSneakers memberships appear in many plans but not all. You should prioritize which extra benefits matter most to your health situation, then verify which plans in your area actually offer those specific benefits at the coverage level you need. This targeted approach helps you select a plan that truly matches your healthcare priorities rather than paying for extras you won’t use.

Understanding these operational details positions you to make an informed choice about whether Part C aligns with your healthcare needs and financial situation. The next section examines the specific medical services that Part C covers and breaks down how deductibles, copayments, and coinsurance actually function in practice.

What Medical Services and Costs Actually Come With Part C

Medicare Advantage plans cover all the services included in Original Medicare Parts A and B, meaning hospital stays, doctor visits, emergency care, and preventive services are part of your package. The critical difference is how you pay for these services and what additional coverage gets bundled in. Part C plans structure costs around copayments, deductibles, and coinsurance rather than the fee-for-service model of Original Medicare.

Understanding Copayments, Deductibles, and Coinsurance

A copayment is a fixed dollar amount you pay for a specific service, such as $25 for a doctor visit or $50 for an emergency room visit. Coinsurance works differently-you pay a percentage of the service cost after meeting your deductible, typically ranging from 10 to 20 percent depending on the plan. Deductibles under Part C vary substantially; some plans have no deductible at all while others require you to pay $500 or more before coverage kicks in.

The Kaiser Family Foundation reported that as of 2026, Medicare Advantage plans offered an average of 32 different options with prescription drug coverage in most areas, meaning your actual costs depend entirely on which specific plan you select. This variability is why comparing the exact cost structure across multiple plans matters far more than focusing on advertised monthly premiums. A plan advertising zero premium might require a $1,000 deductible and $45 copayments per doctor visit, while a plan charging $50 monthly might have a $250 deductible and $20 copayments.

Your total yearly spending depends on how often you use healthcare services. If you visit your doctor four times annually and take three prescription medications, calculate your out-of-pocket costs across competing plans to reveal which option actually costs less over the full year, not just the premium difference.

How Network Restrictions Affect Your Healthcare Costs

Network restrictions create the second major cost consideration in Part C. When you use an in-network provider, you pay the copayment or coinsurance amount specified in your plan documents. Using an out-of-network provider typically costs significantly more-sometimes double or triple the in-network rate-or the plan may not cover the service at all. This distinction fundamentally changes your healthcare costs throughout the year.

If your preferred cardiologist isn’t in the plan’s network, every visit costs substantially more than if you switched to an in-network specialist. Some Part C plans operate as HMOs and require referrals from your primary care doctor before seeing specialists, adding administrative steps that delay care. PPO-style Part C plans generally allow direct specialist access without referrals but often charge higher copayments for out-of-network services.

Verify before enrollment whether your current doctors participate in the specific plan’s network. Many people enroll based on premium alone, then discover their doctor isn’t covered and face the choice of switching providers mid-year or paying out-of-network rates. This scenario is entirely preventable through advance research using the Medicare Plan Finder, which displays participating providers by plan and ZIP code. Additionally, plan networks change annually, so a doctor who was in-network in 2025 might not be in 2026. Check your plan’s network every October during open enrollment to prevent surprise coverage gaps.

The Annual Out-of-Pocket Maximum Provides Financial Protection

The annual out-of-pocket maximum provides a financial safety net that Original Medicare lacks. Once you reach this limit, you pay nothing for covered services for the remainder of that calendar year. This protection is particularly valuable if you face unexpected hospitalizations or develop conditions requiring frequent specialist visits.

However, the monthly copayments and deductibles you pay throughout the year count toward this maximum, and out-of-network services often don’t count, meaning your actual spending protection depends on using in-network providers consistently. Understanding this distinction helps you anticipate your true financial exposure under any Part C plan you consider.

The cost structure of Part C plans creates a complex landscape where the lowest premium doesn’t necessarily mean the lowest total cost. Your next step involves examining which specific benefits Part C plans add beyond Original Medicare coverage and how those extras influence your overall healthcare value.

Comparing Medicare Part C to Other Medicare Options

How Part C Eliminates the Need for Medigap Coverage

Part C removes the requirement for separate Medigap policies that Original Medicare enrollees typically purchase to cover gaps in hospital and doctor visit costs. With Original Medicare, you pay 20 percent coinsurance for most doctor visits after meeting your annual deductible, and hospital stays involve separate deductibles for each benefit period. Many people add Medigap coverage on top to reduce these out-of-pocket expenses, which means paying premiums for both Original Medicare and a supplemental plan. Part C structures coverage differently: you pay predictable copayments instead of percentage-based coinsurance, and once you hit your annual out-of-pocket maximum, additional covered services cost nothing. This structure eliminates the need for Medigap entirely since Part C already includes the financial protections that supplemental coverage provides.

The trade-off involves network restrictions. Original Medicare with Medigap allows you to see any provider accepting Medicare nationwide, while Part C forces you into a defined network. If you have established relationships with specific doctors or specialists, this network restriction matters significantly for your healthcare experience.

Prescription Drug Coverage and Extra Benefits Shape the Real Decision

The real decision hinges on your prescription drug needs and extra benefit priorities. Part C plans bundle prescription coverage directly into the plan, while Original Medicare requires a separate Part D policy that costs additional premiums and involves different formularies and pharmacy networks. If you take multiple medications, Part C integration simplifies administration and potentially reduces total costs compared to managing separate Part D coverage.

Part C plans also offer dental, vision, hearing, and fitness benefits that Original Medicare never covers, requiring separate out-of-pocket payments if you choose Original Medicare. Kaiser Family Foundation data on Part C plan availability shows substantial choice in finding plans that match your specific medication needs and desired extra benefits.

Evaluating Your Actual Healthcare Costs Across Both Approaches

The trade-off remains network restriction and potentially higher copayments for frequent services. If you rarely see specialists, take few medications, and prioritize maximum provider choice, Original Medicare with Medigap and standalone Part D may cost less overall. If you take multiple prescriptions, use dental or vision services regularly, and have healthcare providers within specific networks, Part C typically delivers better value.

Comparing your actual annual costs across both approaches using the Medicare Plan Finder tool reveals which option your wallet actually prefers rather than relying on general assumptions about what coverage type works best. Calculate your expected out-of-pocket expenses under each scenario (Original Medicare plus Medigap plus Part D versus Part C) based on your current doctors, medications, and anticipated healthcare usage. This calculation transforms an abstract comparison into concrete numbers that guide your decision.

Final Thoughts

Medicare Part C coverage requires you to evaluate your specific healthcare situation rather than make assumptions based on what works for others. Your actual costs depend entirely on which plan you select, whether your preferred doctors participate in available networks, and whether your current medications appear on plan formularies at affordable cost tiers. The Medicare Plan Finder tool reveals which options genuinely fit your situation when you enter your ZIP code and compare the specific copayments, deductibles, and extra benefits each plan offers.

We at Dave Silver Insurance bring over 17 years of expertise helping people navigate these exact decisions. Our team works with you to understand your health needs, medications, and provider preferences, then identifies which Medicare Part C plans actually deliver the coverage and costs that match your situation. We remain accessible seven days a week to answer your questions and guide you through enrollment.

Rather than spending hours comparing plans independently, contact Dave Silver Insurance to receive personalized recommendations backed by detailed analysis of your actual healthcare costs. This clarity transforms Medicare enrollment from overwhelming to straightforward, giving you confidence that your coverage decision aligns with both your health and financial needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation