Medicare covers many healthcare costs, but it leaves gaps that can create significant out-of-pocket expenses for beneficiaries.

What is a Medigap insurance policy? It’s supplemental coverage designed to fill these gaps by paying for costs that Original Medicare doesn’t cover, like deductibles and coinsurance.

We at Dave Silver Insurance help Medicare beneficiaries understand how Medigap works and which plan options provide the best financial protection for their specific needs.

What Exactly Is Medigap Insurance

Understanding Medigap Coverage and Its Purpose

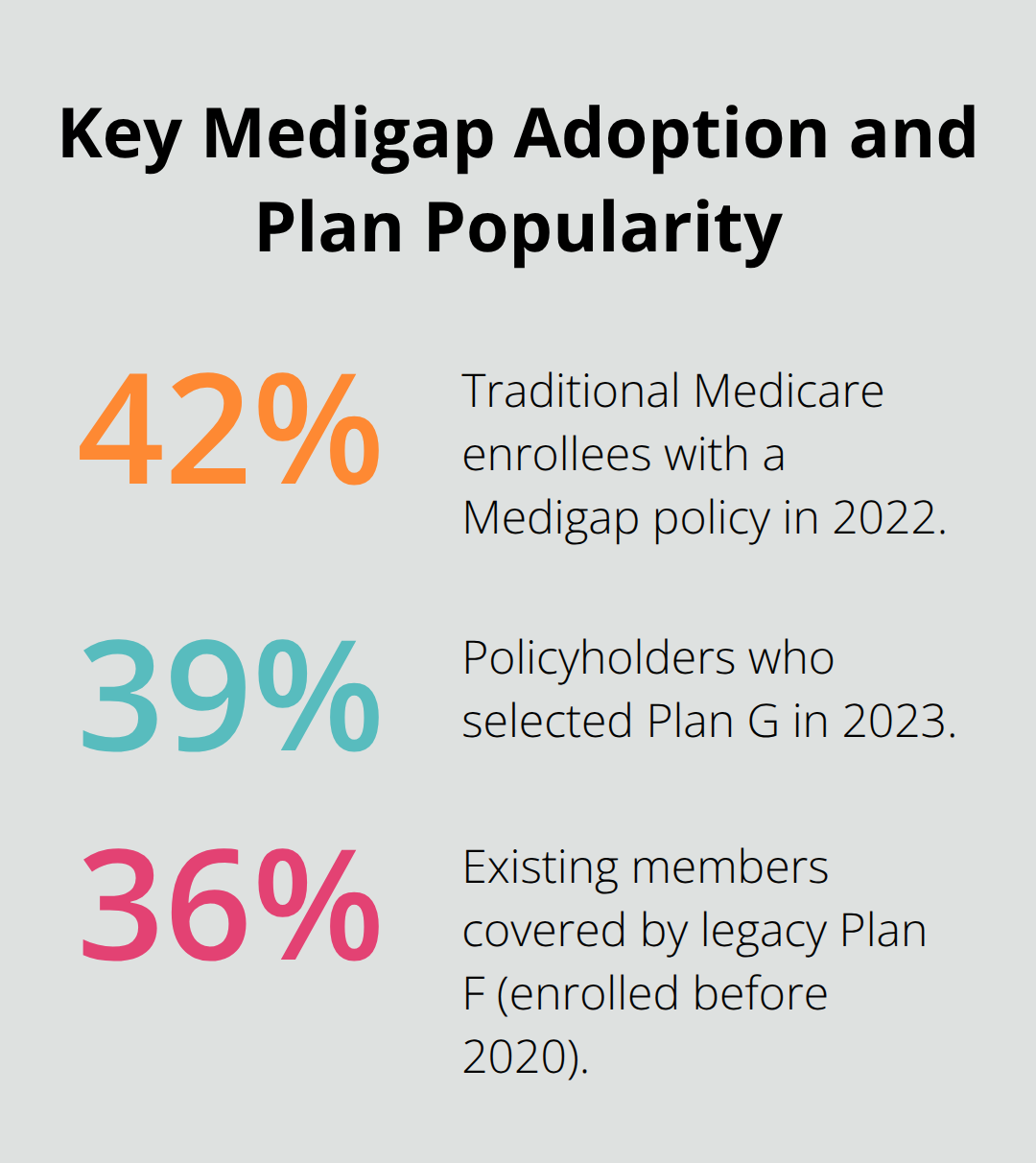

Medigap insurance provides private supplemental coverage that works exclusively with Original Medicare Parts A and B. The Kaiser Family Foundation reports that approximately 12.5 million Medicare beneficiaries (or 42% of traditional Medicare enrollees) had a Medigap policy in 2022. The average monthly premium reached $217 in 2023, but this investment protects against potentially thousands in medical bills.

Plan G became the most popular choice in 2023, with 39% of policyholders selecting this option, while legacy Plan F still covers 36% of existing members who enrolled before 2020.

How Medigap Differs From Medicare Advantage Plans

Medicare Advantage and Medigap serve completely different purposes and cannot work together. Medicare Advantage replaces Original Medicare entirely with private plan networks, while Medigap supplements Original Medicare by covering gaps like deductibles and coinsurance. The average Medicare Advantage premium costs just $17 monthly in 2025, but 23% of Medicare Advantage beneficiaries spend over 10% of their income on healthcare costs compared to only 17% of Medigap holders. Medicare Advantage plans cap annual out-of-pocket costs at $9,350 in 2025, but Medigap provides predictable costs upfront with comprehensive coverage.

Medigap Eligibility Requirements and Enrollment Windows

You must have Original Medicare Parts A and B to purchase Medigap. The optimal enrollment window occurs during the six-month Medigap Open Enrollment Period that starts when you turn 65 and enroll in Part B. Insurance companies cannot deny coverage or charge higher premiums based on health conditions during this period. Missing this window means you face medical underwriting and potential coverage denials. Each spouse needs a separate Medigap policy since coverage applies to individuals only. Only 7% of Medicare beneficiaries under 65 with disabilities have Medigap compared to 46% of those 65 and older (reflecting limited availability for younger beneficiaries in most states).

How Medigap Works With Your Healthcare Providers

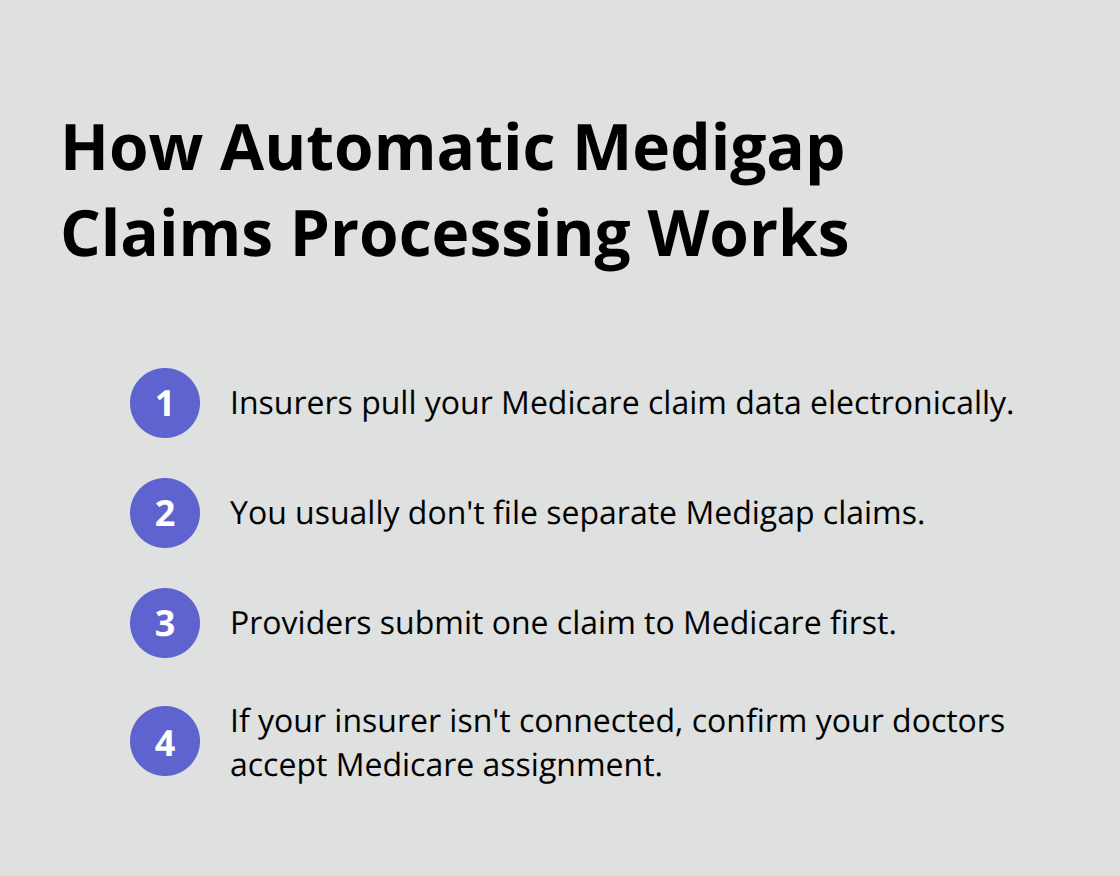

Most Medigap policies require the insurance company to obtain your Part B claim information directly from Medicare for efficient processing. If a Medigap insurer doesn’t retrieve claims info from Medicare, verify that your doctor participates in Medicare and accepts assignment for all patients. This coordination streamlines the payment process and reduces paperwork for beneficiaries. Understanding how these payment mechanisms work becomes essential when you explore the specific ways Medigap supplements your Original Medicare coverage.

How Medigap Processes Your Medical Claims

Payment Flow Between Medicare and Medigap

Medigap operates as a secondary payer that automatically activates after Medicare processes your claim. When you visit a healthcare provider, Medicare pays its portion first according to the approved amount for your service. Your Medigap policy then pays its share of the costs like deductibles, coinsurance, or copayments based on your specific plan coverage. The Centers for Medicare and Medicaid Services oversees programs that serve over 170 million Americans, with Medigap insurers handling secondary payments seamlessly for their 12.5 million policyholders.

Automatic Claims Processing Eliminates Paperwork

Most Medigap insurers retrieve your Medicare claim information directly from the government database through electronic data interchange systems. This means you typically won’t file separate Medigap claims or handle reimbursement paperwork. Your healthcare provider submits one claim to Medicare, and your Medigap insurer automatically receives the claim details to process their portion of payment.

However, if your Medigap company doesn’t participate in this automatic system, verify that your doctors accept Medicare assignment to avoid payment complications and potential balance bills.

Medicare Part A and Part B Coverage Coordination

Medigap coordinates differently with Medicare Part A hospital coverage versus Part B outpatient services. For Part A services, most Medigap plans cover the $1,676 hospital deductible in 2025, plus coinsurance for extended stays beyond 60 days. Part B coordination involves coverage of the annual $240 deductible and the standard 20% coinsurance that Medicare doesn’t pay. Plan G holders save an average of $2,400 annually on these out-of-pocket costs according to insurance industry data. The coordination happens automatically whether you receive inpatient hospital care, outpatient procedures, or physician visits covered under these Medicare components.

What Happens When Claims Get Denied

Medicare denial doesn’t automatically mean your Medigap claim gets denied, but it does affect the payment process. If Medicare denies a claim because the service isn’t covered under Parts A or B, your Medigap policy won’t pay either since it only supplements Medicare-approved services. However, if Medicare approves the service but you haven’t met your deductible, Medigap steps in to cover that gap (depending on your plan type). Appeal processes work through Medicare first, then Medigap follows Medicare’s final determination for secondary payment decisions.

These automatic payment systems work hand-in-hand with the specific benefits each Medigap plan provides, which vary significantly based on the standardized plan letters you choose from.

Which Medigap Plan Offers the Best Value

Understanding the Ten Standardized Medigap Options

Federal law standardizes Medigap plans A through N, which means Plan G from one insurer provides identical benefits to Plan G from another company. Plan G dominates the market, while legacy Plan F covers 36% of existing policyholders who enrolled before 2020. Plans C and F vanished for new Medicare beneficiaries after January 1, 2020, but remain available for those grandfathered in. The Kaiser Family Foundation data shows Plan G premiums averaged $140 to $236 monthly in 2023 (with rates that vary by state), and New York commands the highest rates. Plans K and L offer lower premiums but require cost-share through an annual out-of-pocket maximum of $6,940 for Plan K in 2023.

Coverage Gaps That Matter Most for Your Wallet

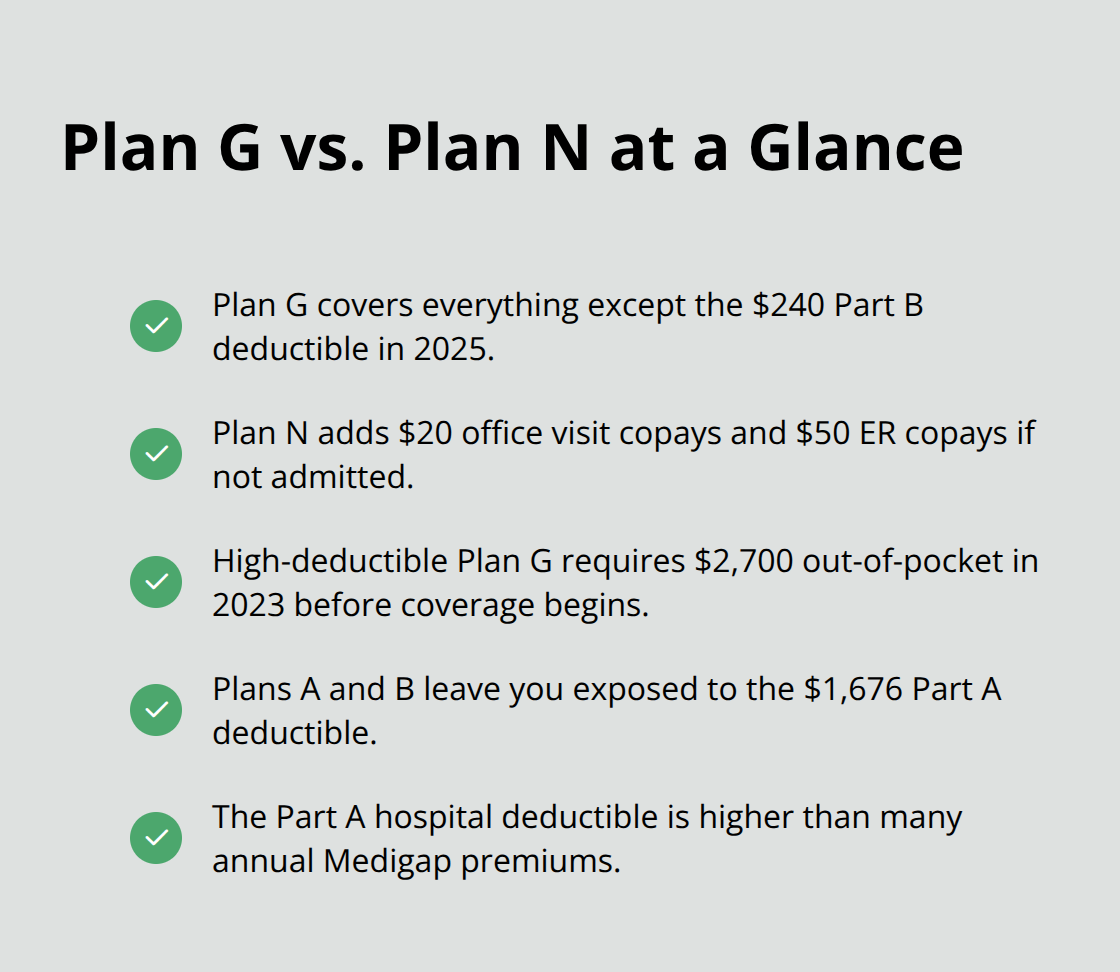

Plan G covers everything except the Medicare Part B annual deductible of $240 in 2025, which makes it the most comprehensive option for new enrollees. Plan N provides similar coverage but requires $20 copayments for office visits and $50 for emergency room visits that don’t result in admission.

High-deductible Plan G requires you to pay $2,700 out-of-pocket in 2023 before coverage begins, but premiums run significantly lower at around $50-80 monthly. Plans A and B cover basic hospital costs but leave you exposed to the $1,676 Medicare Part A deductible and skilled care facility coinsurance. The Medicare Part A hospital deductible alone costs more than many annual Medigap premiums (which makes comprehensive plans financially smart for most beneficiaries).

Premium Prices Vary Dramatically by State and Insurer

Medigap premiums for identical coverage can differ by $200 monthly between insurance companies in the same zip code. A 65-year-old man in Florida pays between $64 to $263 for similar Plan G coverage according to industry data, while Connecticut residents face community rates that spread costs evenly across all ages. Nine states require community rate systems that prevent age-based premium increases, but most states allow insurers to charge older beneficiaries significantly more. Compare at least three quotes from different insurers during your six-month open enrollment window when health conditions cannot affect price or approval decisions.

Final Thoughts

What is a Medigap insurance policy? It transforms unpredictable Medicare gaps into manageable monthly premiums that protect your financial health. With 42% of traditional Medicare beneficiaries who choose Medigap coverage, the data speaks clearly about its value. Plan G offers the best combination of comprehensive coverage and reasonable premiums for most new enrollees, while Plan N provides solid protection with modest copayments for budget-conscious beneficiaries.

The six-month open enrollment window that starts at age 65 represents your best opportunity to secure coverage without health questions or premium penalties. Compare quotes from multiple insurers since identical plans can vary by hundreds of dollars annually. Focus on long-term affordability rather than the lowest initial premium (as community-rated states offer more predictable costs over time).

We at Dave Silver Insurance provide personalized guidance through Medicare’s complexities. Our availability means you get tailored recommendations based on your unique health and financial situation. Schedule a consultation with Dave Silver Insurance to gain clarity and confidence in your healthcare decisions before your enrollment window closes.