Turning 65 brings Medicare, but it doesn’t cover everything. That’s where Medigap comes in-and getting it right matters more than most people realize.

We at Dave Silver Insurance know that Medigap enrollment tips can be confusing, especially when you’re juggling deadlines and plan options. This guide walks you through what you need to know to lock in the right coverage at the right time.

Medigap Coverage Explained

What Medigap Actually Covers

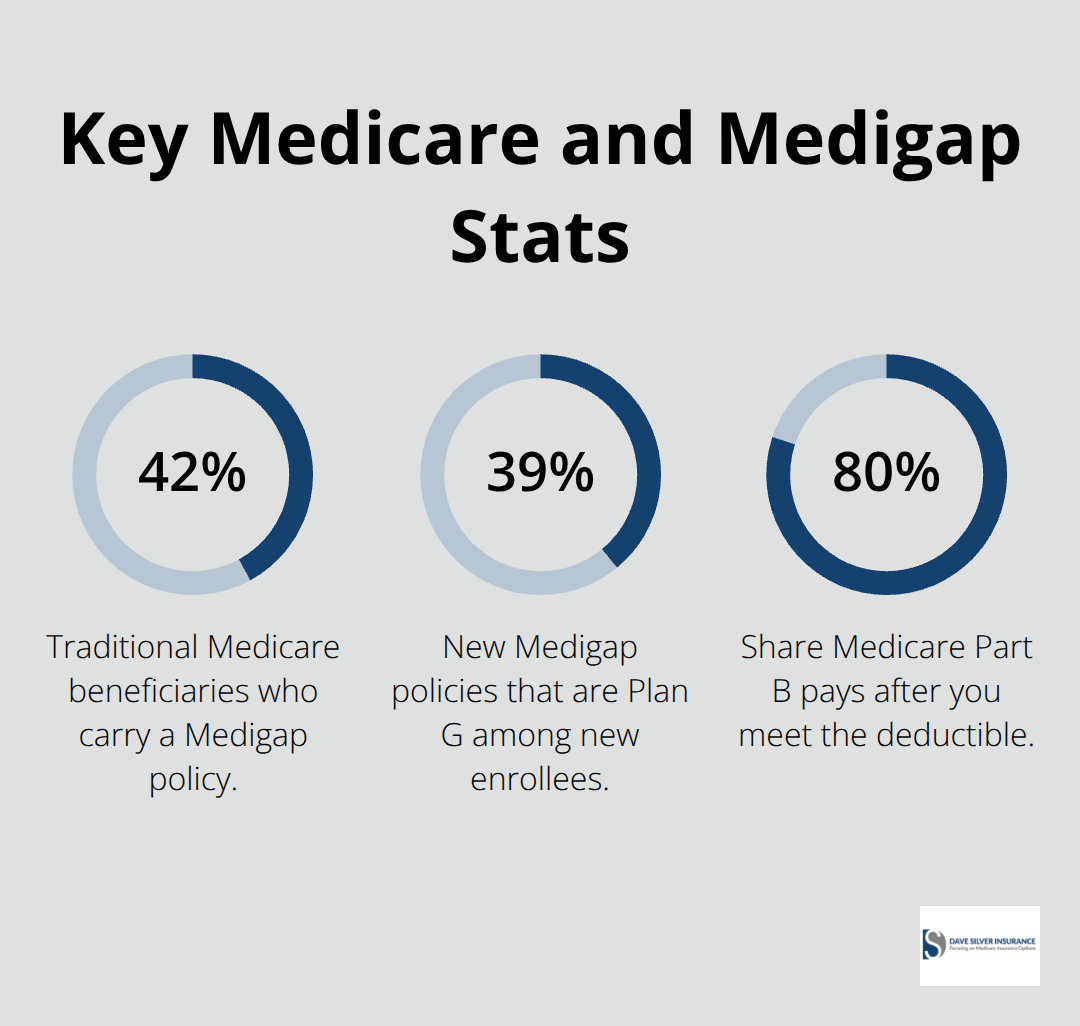

Medigap fills the gaps that Original Medicare leaves behind. After Medicare pays its share of your medical bills, you owe the rest-copayments, coinsurance, and deductibles. According to data from the Kaiser Family Foundation, about 42% of traditional Medicare beneficiaries have purchased a Medigap policy, and for good reason. The Part B deductible alone sits at $240 in 2026, and that’s just the beginning.

If you need hospitalization, you could face a Part A deductible of $1,556.

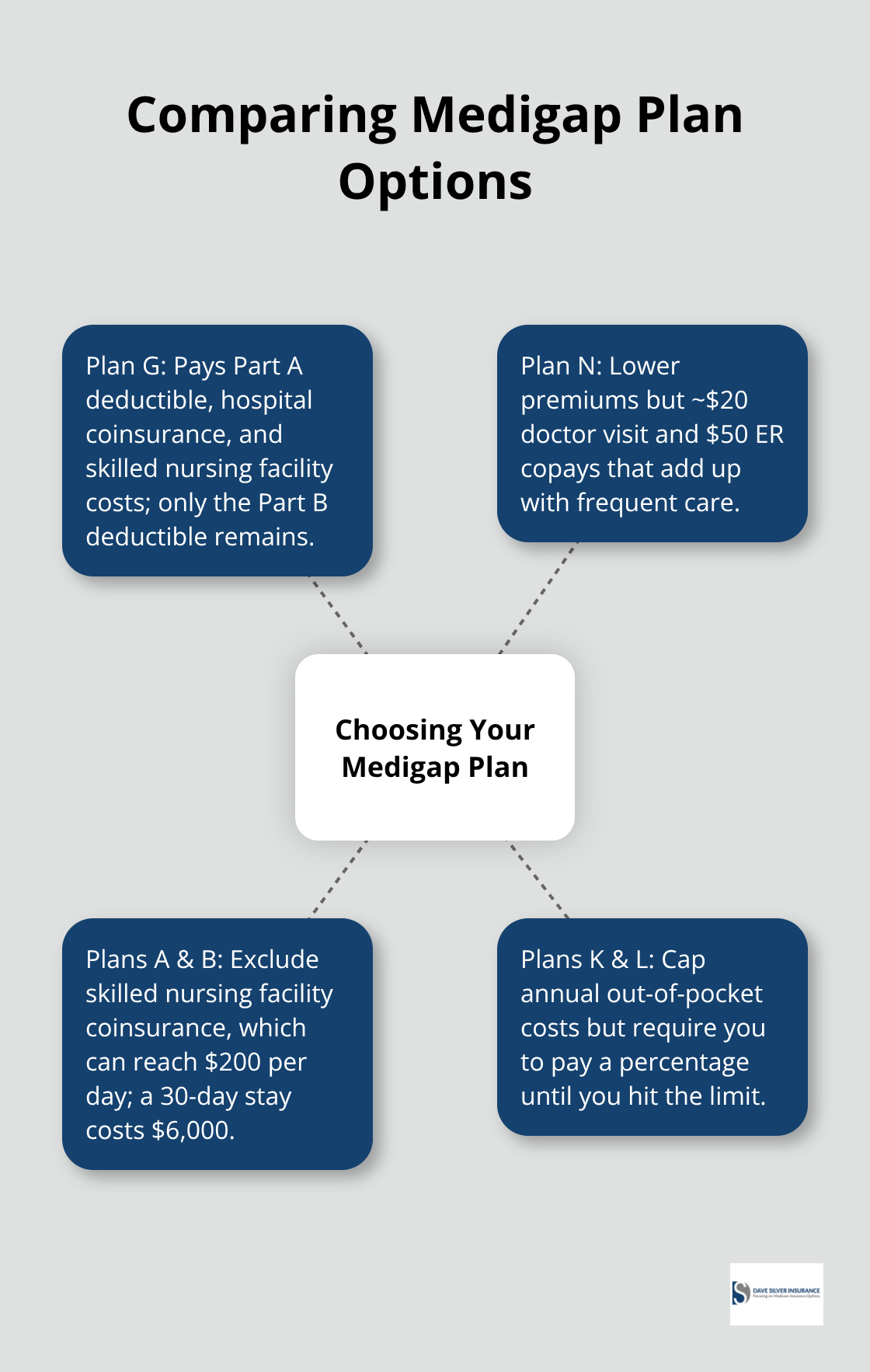

Medigap policies are standardized by plan letter, meaning Plan G from one insurer covers identical benefits to Plan G from another insurer in your state. This standardization makes comparison straightforward-the only real difference between insurers offering the same plan letter is price. Plan G has emerged as the most popular choice for new enrollees, covering approximately 39% of new Medigap policies according to the Kaiser Family Foundation. It pays your Part A deductible, hospital coinsurance, and skilled nursing facility costs, though it doesn’t cover the Part B deductible.

Plan N offers lower monthly premiums but requires you to pay small copayments-typically around $20 for most doctor visits and $50 for emergency room care. The average monthly premium for Plan G across the country was $164 in 2023, ranging from $140 in areas like Washington D.C. and Hawaii to $236 in New York. This variation matters significantly when you shop for coverage.

How Medigap Works With Your Medicare

You must have both Medicare Part A and Part B before you buy any Medigap policy. Medigap doesn’t replace Original Medicare; it works alongside it. When you visit a doctor, Medicare Part B pays its 80% after you meet the deductible, and your Medigap policy then covers what Medicare doesn’t-the coinsurance, copayments, and potentially the deductible itself depending on your plan.

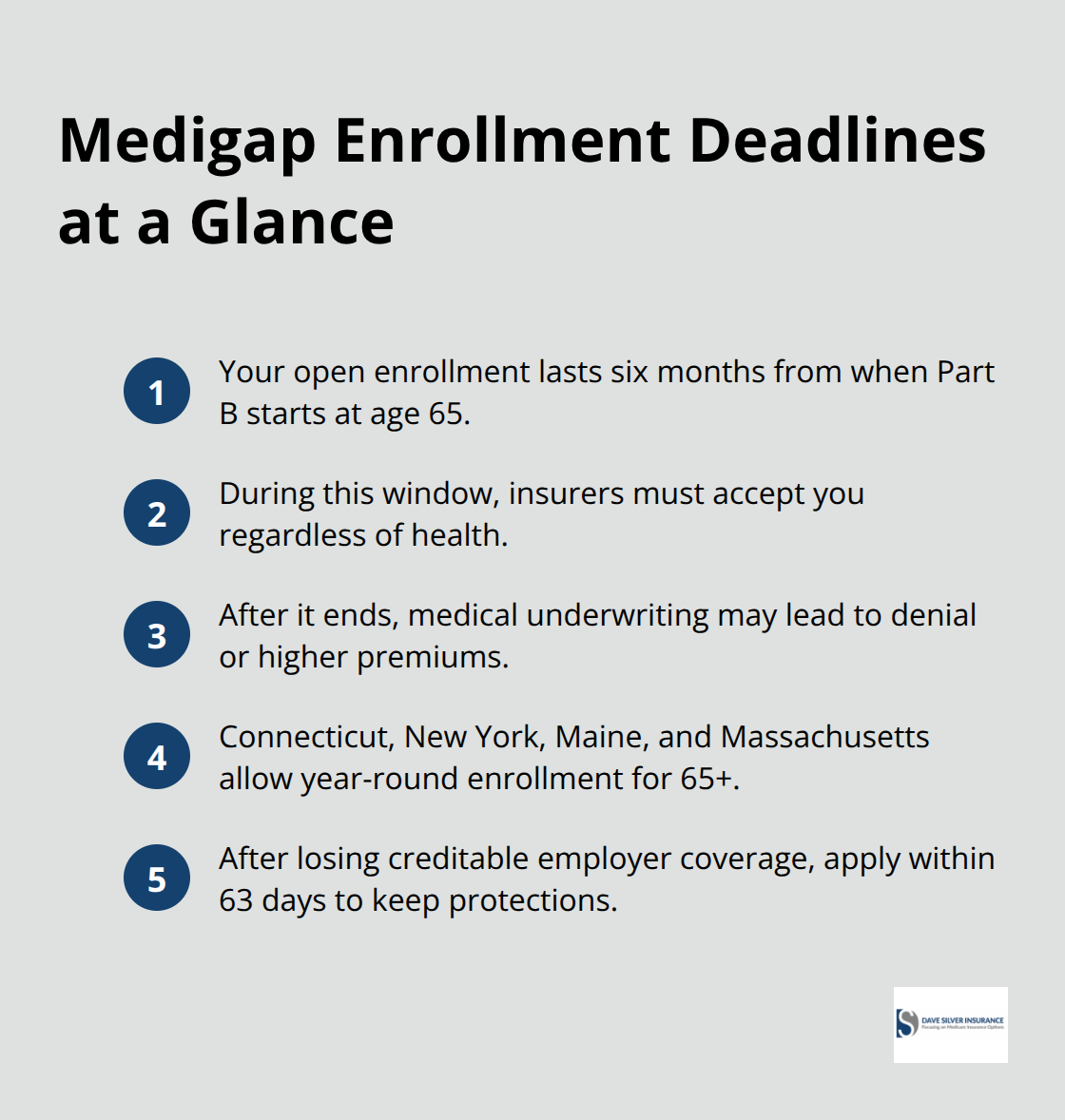

You cannot hold a Medigap policy and a Medicare Advantage plan simultaneously. This is a critical distinction that many people misunderstand. If you’re in Original Medicare and want Medigap, you’re protected during your six-month open enrollment period starting the month you turn 65 and enroll in Part B. During this window, insurers must accept your application regardless of health status and cannot charge you higher premiums based on pre-existing conditions. After this window closes, you may face medical underwriting, which means insurers can deny your application or charge significantly more.

The Misconceptions That Cost Money

Many people believe Medigap covers everything Medicare doesn’t, but that’s not accurate. Medigap doesn’t cover dental, vision, hearing aids, or long-term care. These gaps leave you exposed to substantial out-of-pocket expenses that a Medigap policy won’t touch.

Another common misconception is that all Medigap plans are equally good-they’re not. Plan A and Plan B don’t cover skilled nursing facility coinsurance, which can reach $200 per day. If you need extended skilled nursing care, this gap becomes devastating. Some people wait to enroll in Medigap, thinking they can pick it up anytime. That assumption is expensive. According to Medicare.gov guidance, waiting until after your open enrollment period means you may face medical underwriting and higher premiums, with no guarantee that an insurer will even accept your application.

The timing of your enrollment decision shapes your financial protection for years to come. Your six-month open enrollment window (starting when you turn 65 and enroll in Part B) offers protections that disappear once it closes. Understanding when you can enroll and what happens if you miss that window determines whether you secure affordable coverage or pay penalties for years. This is why the next section focuses on the specific enrollment deadlines and periods that protect your access to Medigap.

Best Time to Enroll in Medigap

Your Six-Month Open Enrollment Window

Your six-month open enrollment period represents the single most important deadline in your Medigap journey, and it expires whether you’re ready or not. This window starts the first month you have Medicare Part B and you’re 65 or older. During these six months, insurers must accept your application regardless of your health status, and they cannot charge you higher premiums based on pre-existing conditions. Medicare.gov confirms that this guaranteed issue protection applies to all Medigap plans sold in your state, meaning you have genuine choice during this window. After these six months close, the rules change dramatically. Insurers may conduct medical underwriting, which gives them the right to deny your application or charge substantially higher premiums. Some states offer extended protections-Connecticut, New York, Maine, and Massachusetts allow year-round enrollment for people 65 and older-but most states do not.

If you live outside these protected states and miss your window, you could spend decades paying more for the same coverage that cost less during open enrollment.

How Age Affects Your Premiums

Age affects your premium calculation in most states through what’s called attained-age rating, where your premium increases as you get older. The Kaiser Family Foundation reported that the average monthly Medigap premium across all plans was $217 in 2023, but Plan G specifically averaged $164 monthly. Delaying enrollment by even one year can mean paying higher premiums indefinitely because the rating system locks in age-based increases. Nine states use community rating instead, meaning age doesn’t affect your premium, but this is the exception, not the rule. Your state’s rating system determines whether waiting costs you money or leaves your premiums stable.

Employer Coverage and Your Enrollment Timeline

If you’re still working at 65 and covered by employer group health insurance, your enrollment timeline shifts significantly. You can delay Part B without penalty while you have creditable employer coverage, which also delays your open enrollment period. Once your employer coverage ends, your six-month window begins then, not when you turned 65. This matters because some people work past 65 and assume they’ve lost their open enrollment window-they haven’t. Document when your employer coverage ends because you’ll need proof when applying for Medigap. The guaranteed issue rights that protect you during open enrollment also apply when you lose other creditable coverage, but you must apply within 63 days of losing that coverage to maintain these protections.

Guaranteed Issue Rights Beyond Open Enrollment

Losing creditable coverage triggers guaranteed issue rights that function similarly to your initial open enrollment period. You gain the ability to enroll in Medigap plans A, B, K, and L without medical underwriting or higher premiums based on health status. The 63-day window following the loss of coverage is tight, so act quickly once your employer plan ends. Some qualifying events (such as moving to a new state or losing Medicare Advantage coverage) also activate guaranteed issue rights, though the specific plans available and timeframes vary by situation. Understanding which events trigger these protections prevents you from accidentally losing your enrollment rights.

Planning Your Enrollment Strategy

Your health status and financial situation should guide when you enroll, but your open enrollment window should never be your backup plan-it should be your primary target. If you anticipate needing significant medical services in the coming years, enrolling during open enrollment locks in affordable rates regardless of any health conditions you develop later. Waiting until after your window closes and then facing medical underwriting could result in denial or premiums so high that coverage becomes unaffordable. The next section walks you through selecting the specific plan that matches your health needs and budget, ensuring your enrollment decision protects both your health and your finances.

Choosing the Right Medigap Plan for Your Needs

Plan G vs. Plan N: Coverage and Cost Trade-offs

Plan selection hinges on two factors: how much medical care you anticipate and how much you’re willing to pay monthly. Plan G dominates the market for new enrollees because it offers comprehensive coverage at a reasonable price point. According to the Kaiser Family Foundation, Plan G covered approximately 39% of new Medigap policies in 2023. It pays your Part A deductible, hospital coinsurance, and skilled nursing facility costs, leaving you exposed only to the Part B deductible (currently $240). If you expect frequent doctor visits, hospitalizations, or extended skilled nursing care, Plan G’s coverage justifies its cost.

Plan N costs less upfront but requires you to pay copayments of around $20 per doctor visit and $50 for emergency room care. These copayments add up quickly if you’re chronically ill or see specialists regularly. For someone with diabetes, arthritis, or heart disease, Plan G eliminates the financial surprises that Plan N introduces.

Conversely, if you’re healthy and rarely visit doctors, Plan N’s lower monthly premium might outweigh the occasional copayment.

Limited-Coverage Plans: When Budget Constraints Matter

Plans A and B offer the cheapest premiums but exclude coverage for skilled nursing facility coinsurance, which reaches $200 per day. A 30-day skilled nursing stay costs $6,000 out-of-pocket under these plans. Plans K and L cap your annual out-of-pocket expenses but require you to pay a percentage of costs until you hit that limit. Unless you have an unusually tight budget, these limited-coverage plans create uncertainty that comprehensive plans eliminate.

Your state’s average premiums matter significantly. Shopping across multiple insurers in your state is non-negotiable because the same plan letter varies substantially in price between carriers. A $50 monthly difference between insurers compounds to $600 annually and $6,000 over a decade.

Assessing Your Health Needs Honestly

Assessing your actual health needs requires honesty about your medical history and family patterns. If your parents or siblings developed serious illnesses in their 70s or 80s, you’re statistically more likely to follow a similar path. Plan for the medical care you expect to need, not the care you hope you won’t.

The Medicare Plan Benefits Comparison tool on Medicare.gov lets you enter your specific medications and doctors to see which plans cover them, but interpreting that data correctly requires experience. State Insurance Assistance Programs (SHIP) offer free, unbiased counseling through shiphelp.org, connecting you with local advisors who understand your state’s specific plan availability and pricing. These conversations take time but save money by preventing expensive enrollment mistakes.

Getting Expert Guidance for Your Situation

Personalized guidance matters when selecting a plan. A consultation identifies gaps in your thinking that you might miss alone. For example, many people underestimate how often they’ll see specialists or how much hospitalization costs. An expert review of your prescriptions, doctor visits, and anticipated procedures reveals which plan genuinely fits your life. Dave Silver Insurance provides individualized recommendations based on your specific health conditions and financial situation, ensuring you select a plan that protects both your health and your savings account.

Final Thoughts

Your Medigap enrollment decision shapes your financial security for years to come. Act during your six-month open enrollment window starting when you turn 65 and enroll in Part B, because insurers cannot deny you coverage or charge higher premiums based on health status during this period. This protection disappears after six months, potentially costing you thousands in higher premiums or leaving you uninsured if medical underwriting results in denial.

Plan G offers comprehensive coverage for most people, while Plan N works for those prioritizing lower monthly costs over copayment certainty. Document your current medications, list your doctors and specialists, and honestly assess your anticipated medical needs over the next five to ten years. Use the Medicare Plan Benefits Comparison tool to see which plans cover your specific prescriptions and providers, then contact your State Insurance Assistance Program through shiphelp.org for free, unbiased guidance tailored to your state’s options.

We at Dave Silver Insurance simplify Medigap enrollment tips with personalized guidance backed by over 17 years of Medicare expertise. Our team reviews your health situation and financial constraints to recommend the specific plan that protects both, handles your enrollment paperwork, and answers your questions before coverage starts. Schedule a consultation with us to discuss your options and secure the right coverage without confusion or delay.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation