Hip replacement surgery can be life-changing, but the cost is a real concern for many people. Medicare covers this procedure, but understanding exactly what’s included requires navigating several moving parts.

We at Dave Silver Insurance help Medicare beneficiaries understand their coverage options every day. This guide walks you through Medicare coverage for hip replacement, the approval process, and practical ways to minimize your out-of-pocket expenses.

What Does Medicare Actually Cover for Hip Replacement

Breaking Down Coverage by Facility Type

Medicare covers hip replacement surgery through Part A and Part B benefits, but your out-of-pocket costs shift dramatically based on where you have the procedure performed. An ambulatory surgical center costs $10,708 total-Medicare pays $8,566, leaving you responsible for approximately $2,142. A hospital outpatient department costs $14,125 total-Medicare covers roughly $12,197, reducing your share to about $1,928. Hospital outpatient procedures cost more upfront but actually result in lower out-of-pocket expenses for you. Part A covers inpatient hip replacement if you’re admitted to the hospital for at least one night, while Part B handles outpatient procedures at surgical centers or hospital outpatient departments. If you’re admitted as an inpatient, you’ll pay the Part A deductible of $1,676 for the first 60 days of your hospital stay, plus any additional inpatient costs beyond that deductible.

Medical Necessity Documentation Determines Approval

Your surgeon must document that hip replacement is medically necessary for Medicare to approve coverage. This means your doctor needs to show that conservative treatments have failed or that your condition warrants immediate surgery. Medicare won’t cover the procedure if your medical records don’t demonstrate genuine medical need rather than elective preference. The surgeon evaluates your condition, reviews imaging results, and documents why the surgery is necessary before submitting this information to Medicare. Without solid documentation, your claim faces denial, and you could end up paying the full cost yourself. Talk with your surgeon before scheduling to confirm they’ll document medical necessity properly and that they accept Medicare assignment (meaning they agree to accept Medicare’s approved amount as full payment for their services).

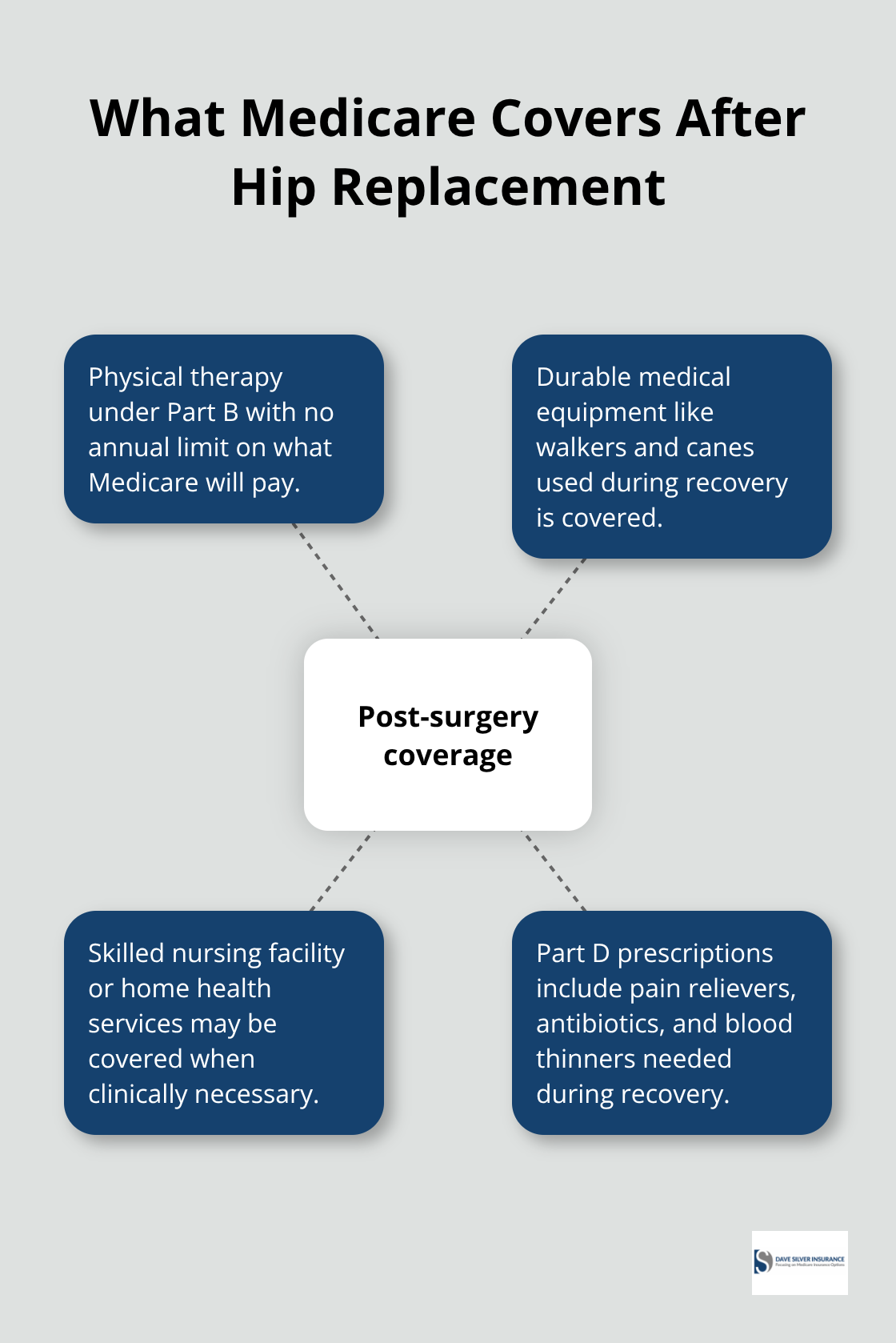

Post-Surgery Care That Medicare Covers

Many people focus only on the surgery cost and overlook that Medicare covers extensive follow-up care. Physical therapy after hip replacement is covered under Part B with no annual limit on what Medicare will pay. Durable medical equipment like walkers and canes used during recovery is also covered. If you need skilled nursing facility care or home health services after discharge, Medicare may cover those costs if clinically necessary. Part D prescription coverage applies to pain medications, antibiotics, and blood thinners you’ll need during recovery. This comprehensive coverage means your total out-of-pocket expenses for the entire hip replacement episode are often lower than the surgery cost alone suggests.

Understanding these coverage details helps you prepare financially, but the approval process itself requires specific steps to move forward. The next section walks you through exactly how to get Medicare’s approval before your surgery date.

Getting Medicare’s Approval Before Your Surgery

Start with Your Primary Care Doctor

Your primary care doctor serves as your entry point, yet this step often gets overlooked or rushed. Schedule an appointment specifically to discuss hip replacement and request a referral to an orthopedic surgeon who accepts Medicare assignment. Surgeons who accept Medicare assignment bill Medicare directly and accept the approved amount as full payment, which protects you from balance billing. Your primary care doctor’s referral signals to Medicare that conservative treatments have been tried and documented.

During this visit, ask your doctor to record in your medical records exactly why you need the surgery: failed physical therapy, imaging showing severe joint damage, pain limiting daily function, or other specific medical reasons. This documentation becomes critical when Medicare reviews your case. Confirm before leaving that your doctor will send the referral electronically to the surgeon’s office. Electronic submission takes 24 to 48 hours and creates a trackable record, whereas paper referrals often get lost.

Gather and Submit Your Medical Records

Once your surgeon’s office receives the referral, they request your medical records and imaging results from your primary care doctor. This typically includes X-rays or MRI scans, blood work results, and your complete medical history. Call the surgeon’s office within three business days to confirm they’ve received everything. Incomplete records may cause Medicare to delay approval or request additional tests, extending your timeline by weeks. The surgeon’s medical team reviews all documentation and determines whether your condition meets Medicare’s definition of medical necessity.

Obtain Pre-Authorization from Medicare

Your surgeon’s office submits a pre-authorization request to Medicare before your scheduled surgery date. While Medicare doesn’t technically require pre-authorization for coverage, hospitals and surgical centers strongly prefer having it on file to avoid claim denials after the procedure. The pre-authorization process typically takes 5 to 10 business days. Your surgeon’s billing department contacts you with an approval number once Medicare approves the request. Write this number down and bring it to your surgery date. If Medicare denies the pre-authorization, your surgeon can appeal or request additional medical documentation within 30 days (though this delay can push back your surgery date significantly).

Understand Your Financial Responsibility Before Surgery

Your surgeon’s office provides an estimate of your out-of-pocket costs based on your specific Medicare plan and the facility type where you’ll have surgery. This estimate accounts for your deductible, coinsurance, and any copays your plan requires. Ask the billing department to explain exactly what you’ll owe at each stage: before surgery, at discharge, and after recovery. Some facilities require a deposit before your procedure; others bill you afterward. Knowing these numbers in advance prevents surprises and allows you to plan financially. If the costs seem high, explore whether Medigap insurance or other coverage options could reduce your expenses-a topic the next section addresses in detail.

How to Minimize Your Out-of-Pocket Hip Replacement Costs

Understanding Your True Financial Responsibility

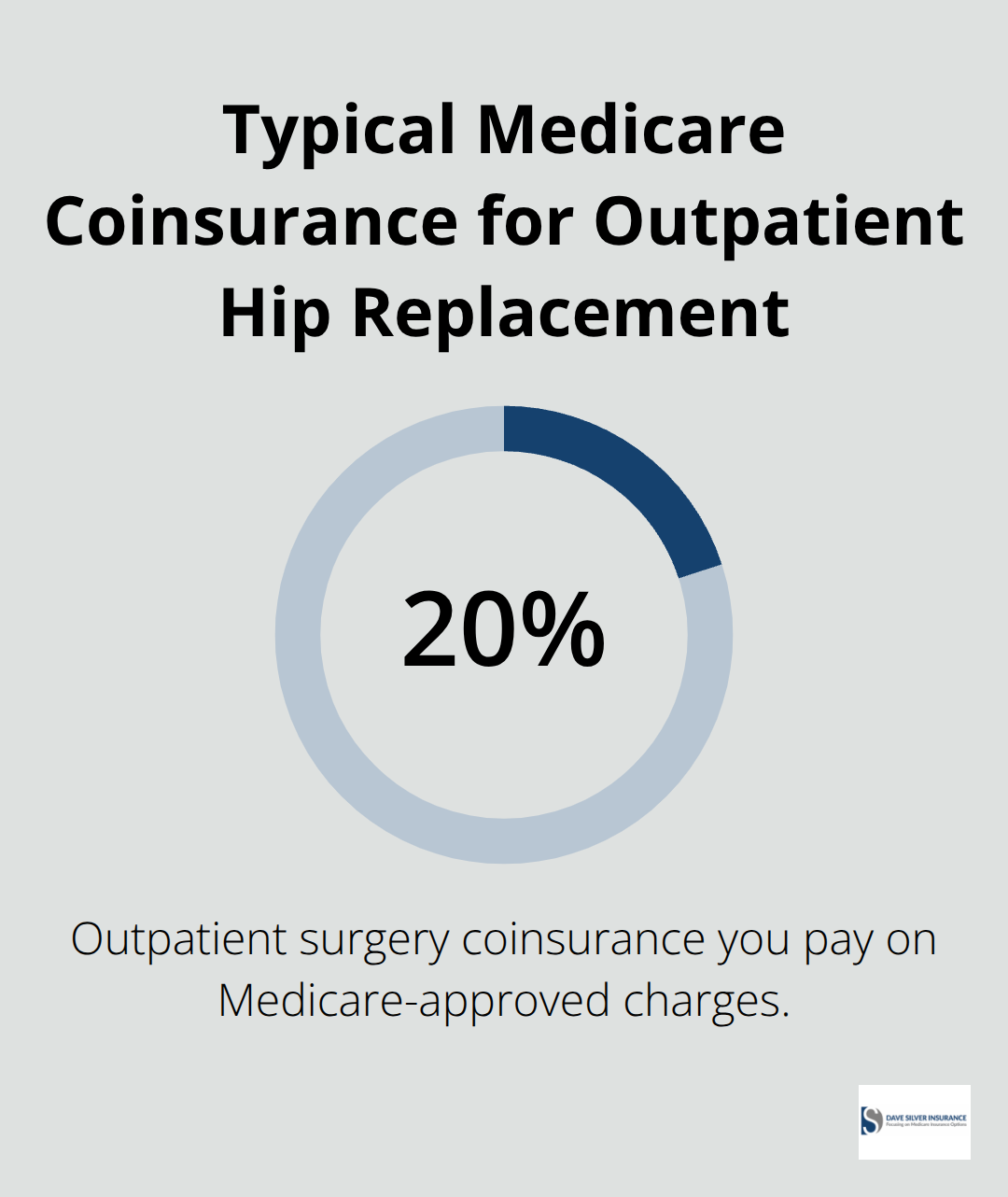

Your Part A deductible of $1,676 for inpatient hip replacement or your Part B coinsurance for outpatient procedures represents just the beginning of what you’ll owe. Medicare covers the approved amount for surgery, but you’re responsible for coinsurance, which typically runs 20 percent of the approved charges for outpatient procedures. If your surgeon’s office estimates $12,197 in Medicare-approved costs for a hospital outpatient procedure, you’ll pay roughly $2,439 in coinsurance alone, plus any applicable deductible.

This is where most Medicare beneficiaries get blindsided.

The surgeon’s billing department should provide a detailed cost breakdown before surgery, but many don’t volunteer this information unless you specifically request it. Demand a written estimate that shows the approved amount, your deductible status, coinsurance percentage, and total out-of-pocket responsibility. If the numbers shock you, the next section explains how Medigap insurance can substantially reduce what comes out of your pocket.

How Medigap Plans Slash Your Coinsurance and Deductible

Medigap insurance covers most or all of your coinsurance and deductible, transforming a $2,400 bill into a few hundred dollars or nothing at all. Plans like Medigap F or Plan G provide comprehensive protection against these costs. The Medigap premium typically costs $100 to $300 monthly depending on your age and location, but for hip replacement alone, the coverage pays for itself.

You must enroll in Medigap within six months of turning 65 or enrolling in Medicare Part B to avoid paying higher premiums due to medical underwriting. Waiting even one month longer can cost you thousands in excess premiums over your lifetime. If you already have Medigap coverage, verify that your plan covers coinsurance and deductibles before your surgery date so you know exactly what to expect.

Part D Coverage Protects You from Prescription Shocks

Part D prescription coverage deserves equal attention because post-surgery medications are not optional expenses. You’ll need pain relievers, antibiotics to prevent infection, and blood thinners to prevent clots, with some patients requiring these medications for weeks or months. A single prescription for a blood thinner like warfarin can cost $300 to $500 monthly without coverage.

Your Part D plan covers these medications, but only if you’ve enrolled before your surgery date. If you haven’t selected Part D coverage, you cannot retroactively enroll for the surgery period, and you’ll pay the full pharmacy price. Many beneficiaries skip Part D thinking they won’t need prescriptions, then face unexpected bills during recovery. The enrollment deadline to avoid penalties is the end of the calendar year, so enroll now even if your surgery is months away.

Comparing Plans to Match Your Medications

Compare Part D plans using Medicare’s plan finder tool, which shows each plan’s formulary coverage for specific medications your surgeon will prescribe. Some plans charge $0 copays for antibiotics during certain tiers, while others charge $50 or more. A ten-minute comparison can save you hundreds during recovery.

If your current Part D plan doesn’t cover a medication your surgeon prescribes, contact the plan’s customer service immediately to request a formulary exception, which often gets approved within 24 to 48 hours. This proactive step prevents gaps in your medication coverage and keeps your recovery on track without unexpected out-of-pocket costs derailing your financial plan.

Final Thoughts

Medicare coverage for hip replacement surgery becomes manageable once you understand facility costs, medical necessity documentation, and how supplemental plans reduce your expenses. Start conversations with your primary care doctor months before your surgery date, request written cost estimates from your surgeon’s billing department, and verify that your Medigap plan covers coinsurance and deductibles. Confirm your Part D enrollment includes the medications you’ll need during recovery, and you’ll transform what feels overwhelming into a clear financial plan.

The difference between beneficiaries who pay thousands out-of-pocket and those who pay hundreds comes down to preparation and knowledge of your options. Hospital outpatient procedures result in lower out-of-pocket costs than ambulatory surgical centers, Medigap insurance eliminates most coinsurance charges, and Part D coverage prevents prescription shock during recovery. Medicare covers not just the surgery itself but also physical therapy, durable medical equipment, and post-acute care services that extend far beyond the operating room.

We at Dave Silver Insurance work with Medicare beneficiaries navigating Medicare coverage for hip replacement decisions every day, and our specialists review your individual circumstances to recommend the plan combination that minimizes your expenses. Our team brings expertise in Medicare Part A, B, C, and D enrollment plus personalized guidance on Medigap insurance options tailored to your specific health and financial situation. Visit Dave Silver Insurance to schedule your free consultation and get clarity on your coverage before your surgery date arrives.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation