Medicare enrollment feels overwhelming because there’s no single right answer for everyone. Your health needs, income, and family situation demand a strategy built specifically for you, not generic advice that works for nobody.

At Dave Silver Insurance, we’ve seen thousands of people choose the wrong plans and pay thousands more than necessary. Personalized Medicare guidance cuts through the confusion and puts real money back in your pocket.

Why Your Medicare Situation Differs From Everyone Else’s

Generic Medicare advice fails because it ignores what actually matters: your specific doctors, medications, income level, and health outlook. We at Dave Silver Insurance have worked with thousands of people over our 17 years in this field, and we’ve watched the same pattern repeat. Someone follows advice from a friend, a website, or a generic article, enrolls in a plan that sounds reasonable, and then discovers six months later that their specialist isn’t covered or their medications cost far more than expected. That person then faces a year of higher out-of-pocket costs because they can’t switch plans until the next enrollment period arrives.

The Real Cost of Wrong Plan Choices

The financial damage from a wrong choice typically ranges from $2,000 to $8,000 annually, depending on your health needs and prescription drug costs. Medicare Advantage plans advertise zero premiums and include dental or vision benefits, which appeals to many people. But if your preferred cardiologist or oncologist isn’t in that plan’s network, you either pay out-of-network rates or change doctors entirely. Original Medicare with a Medigap supplement might cost more monthly but keeps every doctor in the country available to you. Neither option is universally better-the right choice depends entirely on your situation.

Income Level Shapes What You Actually Pay

Your income determines eligibility for programs that cut costs dramatically. If you earn between $1,468 and $1,966 monthly as a single person, you likely qualify for a Medicare Savings Program that covers your Part B premiums, deductibles, and copays. That’s potentially $500 to $1,500 in annual savings you’d miss without personalized review. Extra Help with prescription drug costs provides another layer of support for those under certain income thresholds, reducing your Part D costs to minimal copayments. Yet most people don’t know these programs exist, and they certainly don’t know if they qualify.

Your financial picture also determines whether a Medicare Advantage plan’s annual out-of-pocket maximum ($7,050 in 2025 for most plans) protects you better than Original Medicare with Medigap, which offers predictable copays but higher monthly costs. Working through these numbers requires looking at your actual medications, your expected doctor visits, and your cash flow-not assumptions.

Medications and Specialists Demand a Close Look

Your prescription drugs must appear on a plan’s formulary at a cost tier you can afford, or you’ll face hundreds of dollars in unexpected expenses. A standalone Part D plan might cover your specific medications cheaply, while a Medicare Advantage plan bundling drug coverage leaves you paying more for those same drugs. Similarly, if you need regular care from specialists, their participation in a plan’s network isn’t guaranteed year to year. Plans change their networks annually, and a doctor who was in-network last year might drop out this year.

Reviewing your actual medication list and your preferred providers against specific plan details takes time and attention. This is the only way to avoid surprises. When you work with someone who understands your complete health picture and financial situation, they spot gaps that generic advice misses entirely. That’s what separates a plan that works from one that costs you thousands.

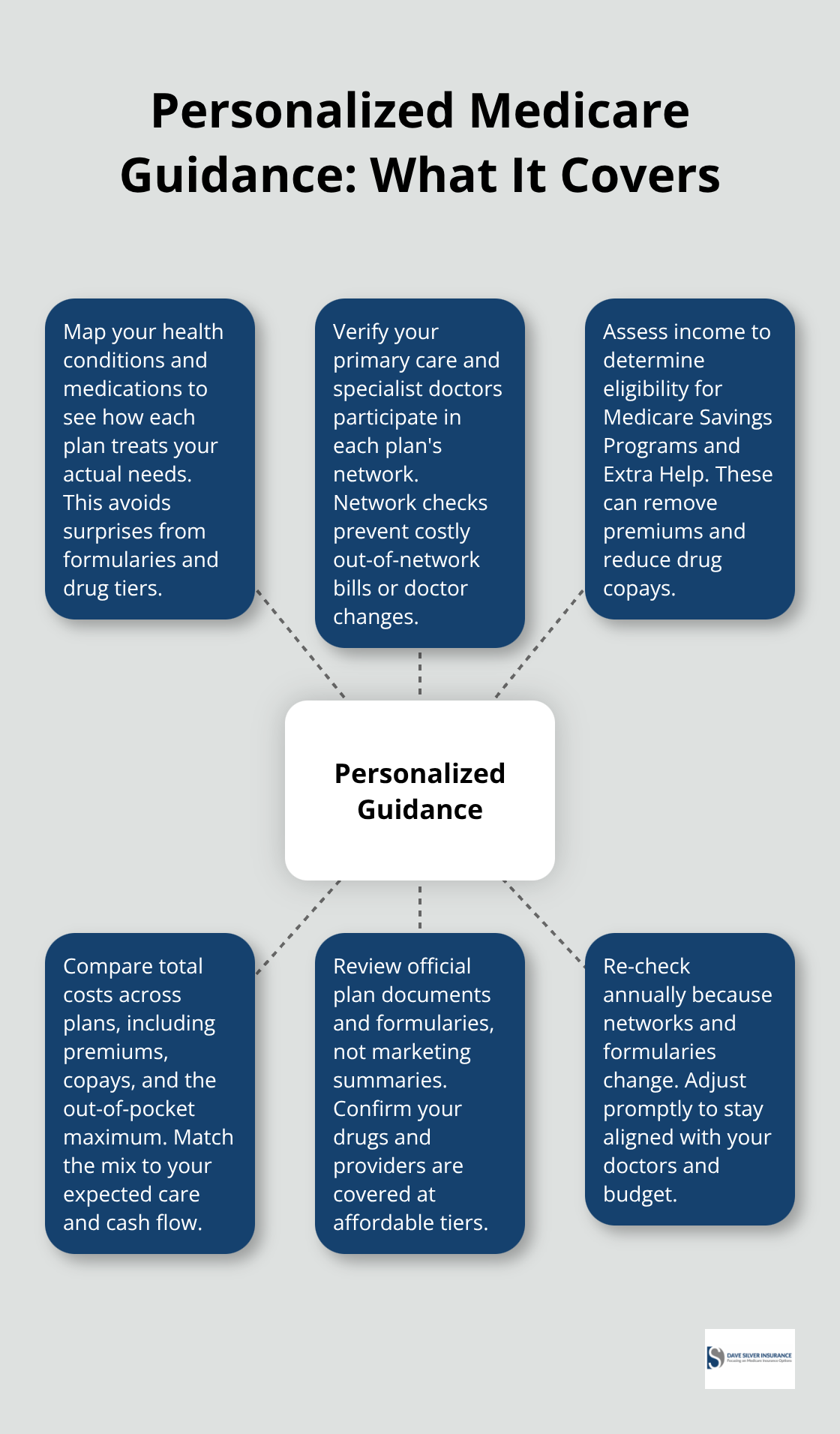

How Personalized Medicare Guidance Works

Map Your Health and Medications First

The process starts with a straightforward conversation about your actual situation, not assumptions. A Medicare specialist will ask you to map out your health conditions, current medications, and the doctors you see regularly. This isn’t theoretical-you’ll need your prescription bottles or a list showing drug names and dosages, because formulary coverage varies dramatically between plans. A medication that costs $15 monthly under one plan’s Part D might cost $200 under another, and generic substitutes often aren’t available for certain conditions.

Your specialist will cross-reference your exact medications against current formularies from multiple plans to identify which options keep your costs low. They’ll also verify whether your preferred doctors-your primary care physician, cardiologist, dermatologist, or any other specialist-actually participate in each plan’s network. Medicare Advantage networks change annually, so last year’s participation means nothing for 2026.

Assess Your Income for Hidden Savings Programs

Income assessment happens next, because it unlocks programs most people don’t realize exist. If your household income falls below specific thresholds set by Medicare, you may qualify for assistance programs that slash your costs. The Medicare Savings Program covers your Part B premium if you earn between $1,468 and $1,966 monthly as a single person, removing that monthly payment entirely. Extra Help reduces Part D copayments to $1 or $2 per prescription for those who qualify. State Pharmaceutical Assistance Programs offer additional drug cost relief depending on where you live.

A personalized review calculates whether your income qualifies you for any of these programs and estimates your actual annual savings. This step alone often reveals $500 to $1,500 in annual assistance that most people miss entirely.

Compare Plan Costs Against Your Health Needs

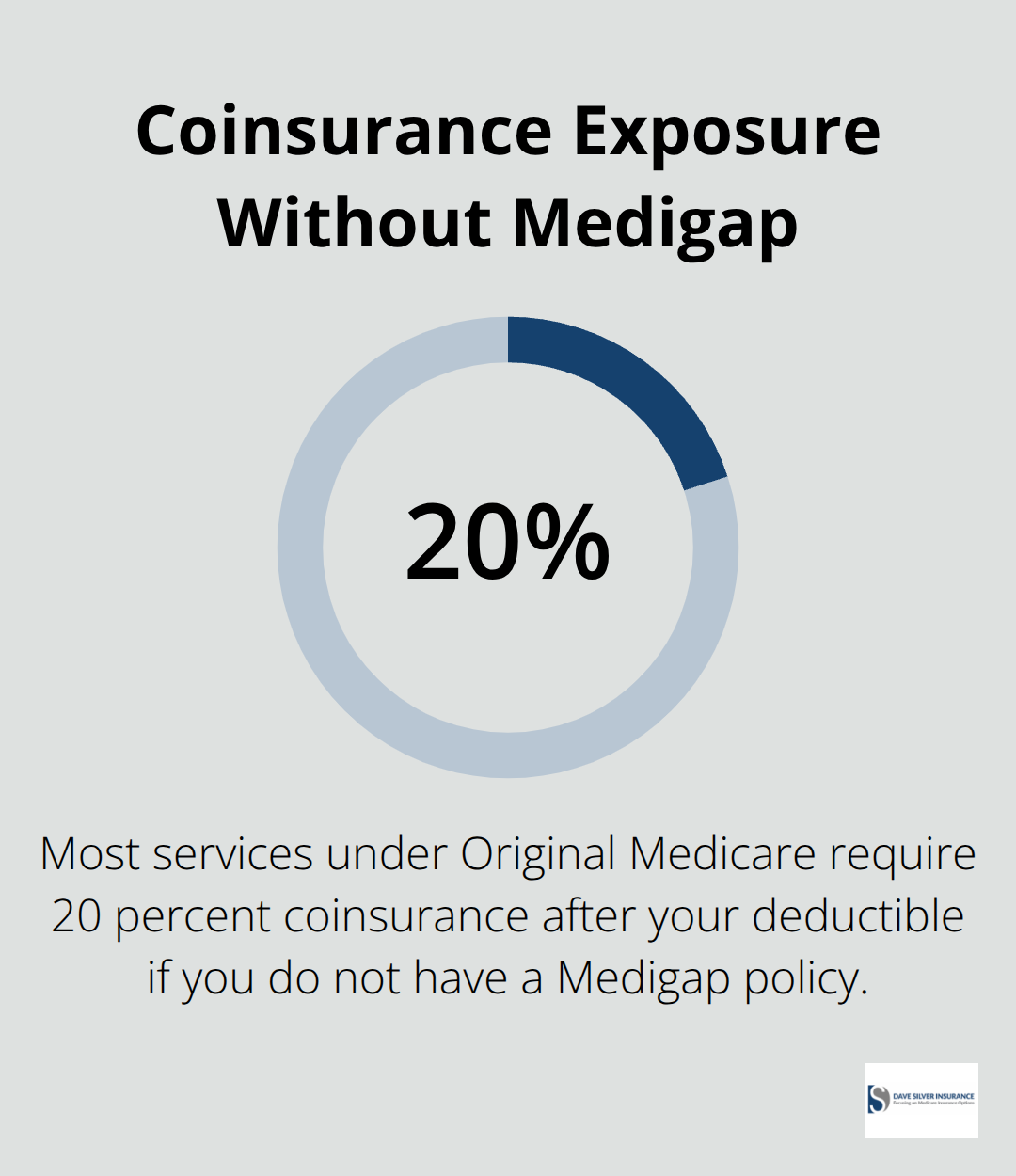

Your financial assessment also determines whether a Medicare Advantage plan’s $7,050 annual out-of-pocket maximum for 2025 protects you better than Original Medicare paired with a Medigap policy. If you have significant health costs or take multiple medications, the out-of-pocket maximum provides predictable budgeting. Original Medicare without a Medigap supplement leaves you exposed to unpredictable coinsurance costs-20 percent of most services after your deductible.

Medigap plans eliminate this uncertainty by covering gaps Original Medicare leaves behind, though you’ll pay higher monthly premiums. The calculation depends on your expected healthcare usage, not general recommendations. Someone with stable health and few medications might prefer Original Medicare with minimal Medigap coverage, while someone managing multiple chronic conditions benefits from comprehensive Medigap or a Medicare Advantage plan with a defined spending cap.

Review Actual Plan Documents and Formularies

Your specialist examines your medical history, prescription list, and anticipated doctor visits to project realistic annual costs under each scenario. They’ll show you actual plan documents and formularies rather than marketing materials, highlighting specifics like whether your diabetes medication appears on a plan’s drug list and what that costs you monthly. This detailed review reveals which plans align with your doctors, medications, and budget-and which ones would drain thousands from your pocket.

Once you understand your options and their true costs, the next step involves selecting the plan that fits your life and preparing for enrollment.

What Medicare Experts Actually Deliver

Plain Language Explanations That Make Sense

Working with a Medicare specialist means you stop decoding confusing documents and start understanding your actual options in clear terms. Medicare experts explain how Part A covers inpatient hospital care, how Part B pays for doctor visits and outpatient services, how Part C bundles everything together through Medicare Advantage plans, and how Part D handles prescription drugs-without the insurance terminology that makes your eyes glaze over. You’ll learn why a plan’s formulary matters to your specific medications, what an out-of-pocket maximum actually protects you from, and whether your preferred cardiologist participates in a particular network. This clarity matters because Medicare enrollment decisions lock you in for a full year. A wrong choice means twelve months of either overpaying for coverage you don’t need or underpaying only to discover gaps in what you thought was included.

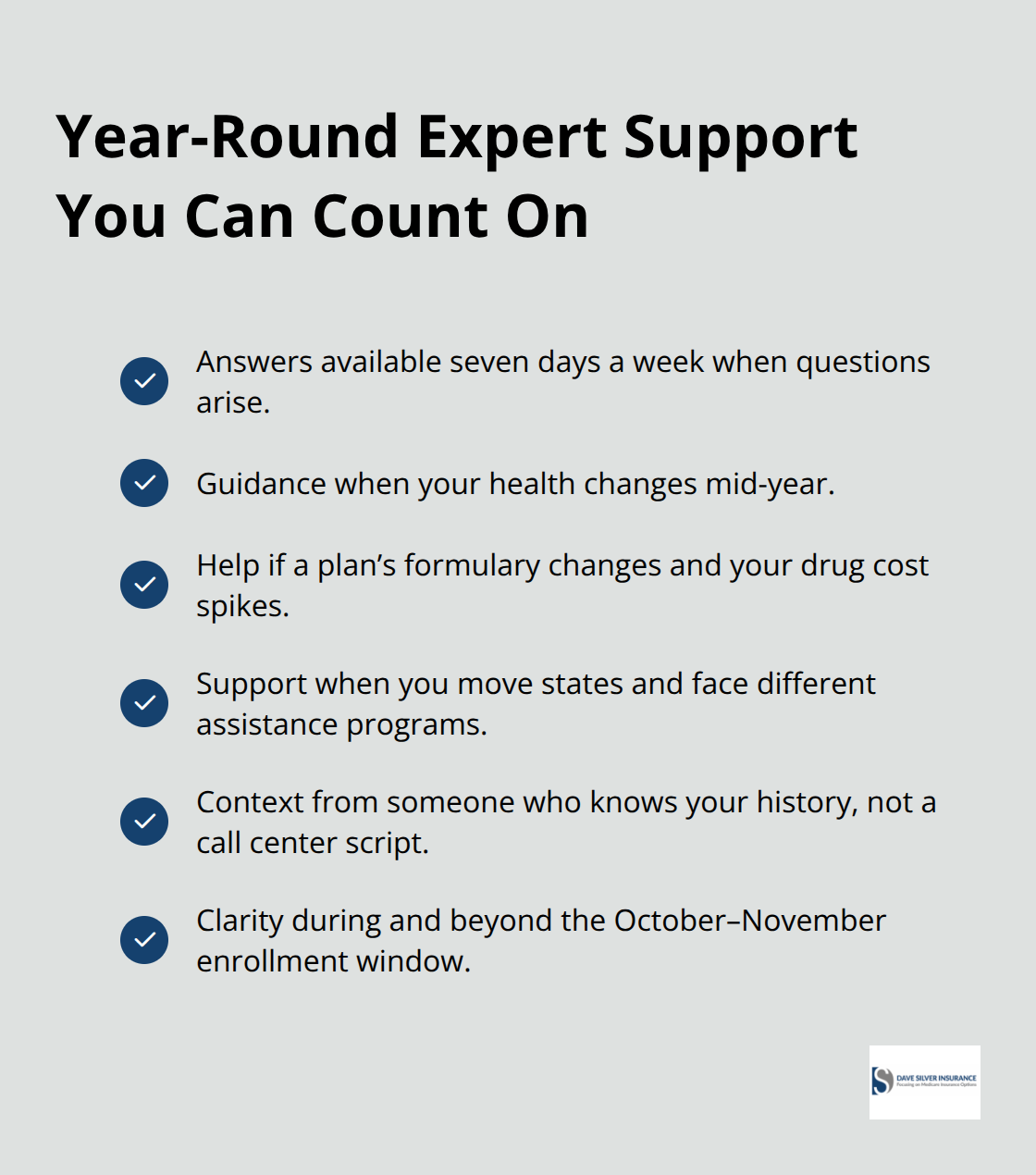

Support That Extends Beyond Enrollment Season

Your specialist provides ongoing access throughout the year, not just during the frantic enrollment window in October and November. If your health changes in March and you need to understand your options, they remain available. If your insurance company changes a formulary in June and your medication suddenly costs more, you can call for guidance on solutions.

If you move to a new state in September, they help you navigate different Medicare Savings Programs and state-specific assistance available in your new location.

Seven-Day-a-Week Availability When You Need It

Medicare questions don’t respect business hours, and neither should expert support. Accessible seven days a week, specialists remain ready to answer your concerns whenever they arise. When you reach out with a problem, you talk to someone who understands your complete situation from your previous conversations, not a call center representative reading from a script. That continuity transforms Medicare management from a stressful annual event into an ongoing partnership where your needs shape the guidance you receive.

Final Thoughts

Personalized Medicare guidance transforms enrollment from a source of stress into a straightforward process where your actual health needs and financial situation drive every decision. The thousands of dollars you save by choosing the right plan justify the time spent understanding your options. Generic advice fails because Medicare has no universal solution-what works for your neighbor creates gaps and overpayment for you.

We at Dave Silver Insurance have spent 17 years helping people navigate this complexity. Our specialists review your medications against current formularies, verify your doctors participate in specific networks, and calculate whether you qualify for assistance programs that cut your costs dramatically. We explain everything in plain language and answer questions seven days a week.

Your next step is straightforward: contact Dave Silver Insurance to discuss your health conditions, medications, and financial situation with a specialist who can show you exactly which plans align with your life. You’ll walk away with clarity about your options and confidence in your enrollment decision.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation