Picking the right Medicare plan shouldn’t feel like a guessing game. The choices are real, the costs vary significantly, and one wrong move can cost you thousands annually.

We at Dave Silver Insurance help people navigate these decisions every day. This guide walks you through concrete Medicare plan comparison tips so you can match your coverage to your actual healthcare needs.

What’s the Difference Between Medicare Parts A, B, C, and D?

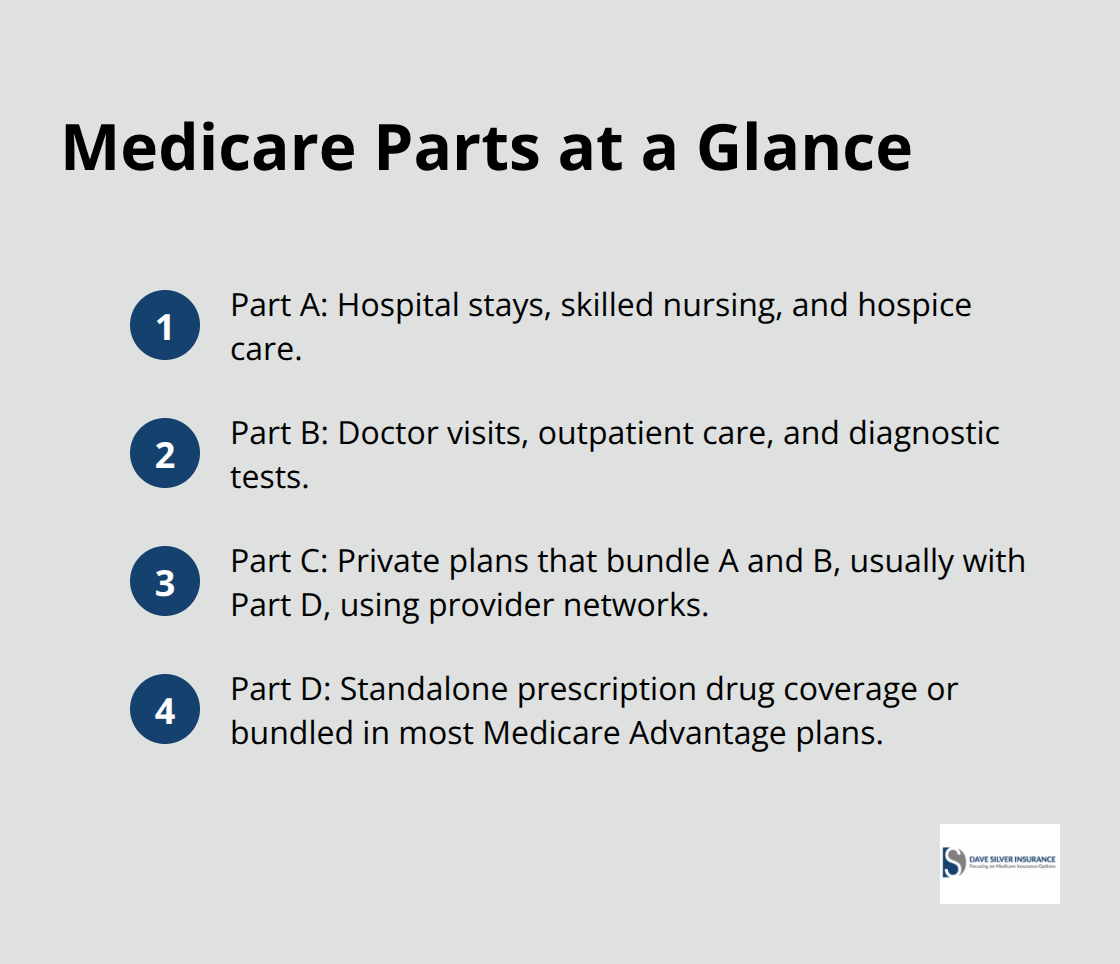

Medicare has four main parts, and understanding what each covers forms the foundation of smart shopping. Part A covers hospital stays, skilled nursing care, and hospice services. Part B covers doctor visits, outpatient care, and diagnostic tests. These two together make up Original Medicare, the traditional government program. Part C, also called Medicare Advantage, is where private insurers step in and bundle Parts A, B, and usually Part D prescription drug coverage into one plan. Part D is standalone prescription drug coverage you add to Original Medicare, or it comes bundled in most Medicare Advantage plans. The key distinction is this: Original Medicare (Parts A and B) gives you access to any doctor or hospital that accepts Medicare, but you pay out-of-pocket costs until you hit your deductible. Medicare Advantage plans use networks, meaning you typically pay less upfront but must see in-network doctors except in emergencies.

About 34 million Americans are enrolled in Medicare Advantage, according to eHealth analysis, so the network trade-off clearly appeals to many beneficiaries.

Original Medicare Means Freedom, Not Predictability

Part A and Part B together offer unlimited access to providers nationwide, but costs remain unpredictable. You pay a Part B deductible each year (currently around $240), then 20 percent coinsurance on most services after that. Hospital stays under Part A carry different cost-sharing rules depending on length of stay. This flexibility attracts people with serious health conditions or those who travel frequently and want to see specialists without referrals. However, costs can spike if you experience multiple hospitalizations or use expensive services. That’s why 42 percent of traditional Medicare beneficiaries-roughly 12.5 million people-pair Original Medicare with a Medigap policy to cover those out-of-pocket costs and create predictability.

Medicare Advantage Caps Your Risk but Limits Choices

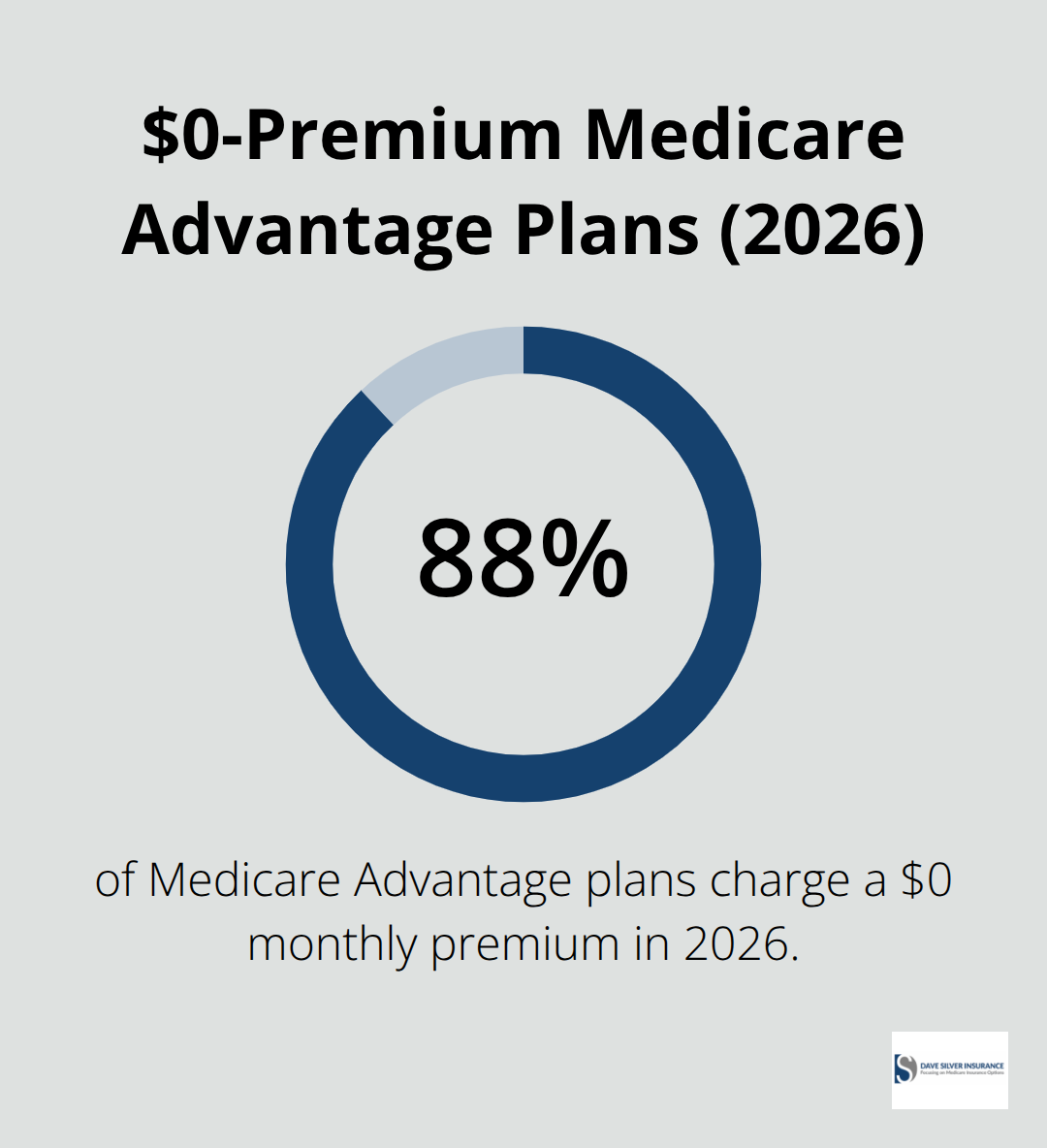

Medicare Advantage plans cap your annual out-of-pocket spending. This ceiling provides financial protection if you experience serious health events. The trade-off involves network restrictions and the need for referrals in HMO plans. About 88 percent of 2026 Medicare Advantage plans charge zero monthly premium, with an average of $4 per month across all plans, making them attractive for cost-conscious shoppers.

Beneficiaries who compared 2025 coverage to 2026 options saved an average of $1,676 annually in out-of-pocket costs, per eHealth, so shopping matters enormously.

Part D Drug Coverage Demands Careful Review

Prescription drug coverage is not optional if you take medications regularly. Skipping Part D when you first qualify triggers a permanent late enrollment penalty added to your premiums for life. Part D plans vary dramatically by location and formulary, the list of covered drugs. Using Medicare Plan Finder on Medicare.gov lets you enter your specific medications and dosages to compare actual costs across plans in your area, sometimes showing 20 or more options. Some plans charge deductibles before coverage kicks in, while others cover common drugs immediately. The donut hole, or coverage gap, occurs after you and your plan spend $3,310 on covered drugs, at which point you pay more until hitting catastrophic coverage around $4,850 in total spending. Understanding your drugs’ tier level and whether your plan covers them during the coverage gap separates smart shopping from expensive surprises.

How These Parts Work Together in Your Decision

The four parts interact in two main pathways. Original Medicare (Parts A and B) works with standalone Part D for drug coverage, and you can add Medigap to reduce out-of-pocket costs. Medicare Advantage (Part C) bundles A, B, and usually D into one plan with network restrictions. Your choice between these pathways depends on whether you value provider flexibility or lower upfront costs. Next, we examine the specific factors you should compare when evaluating plans in your area.

What Numbers Should You Actually Compare

The Three Cost Layers Most People Ignore

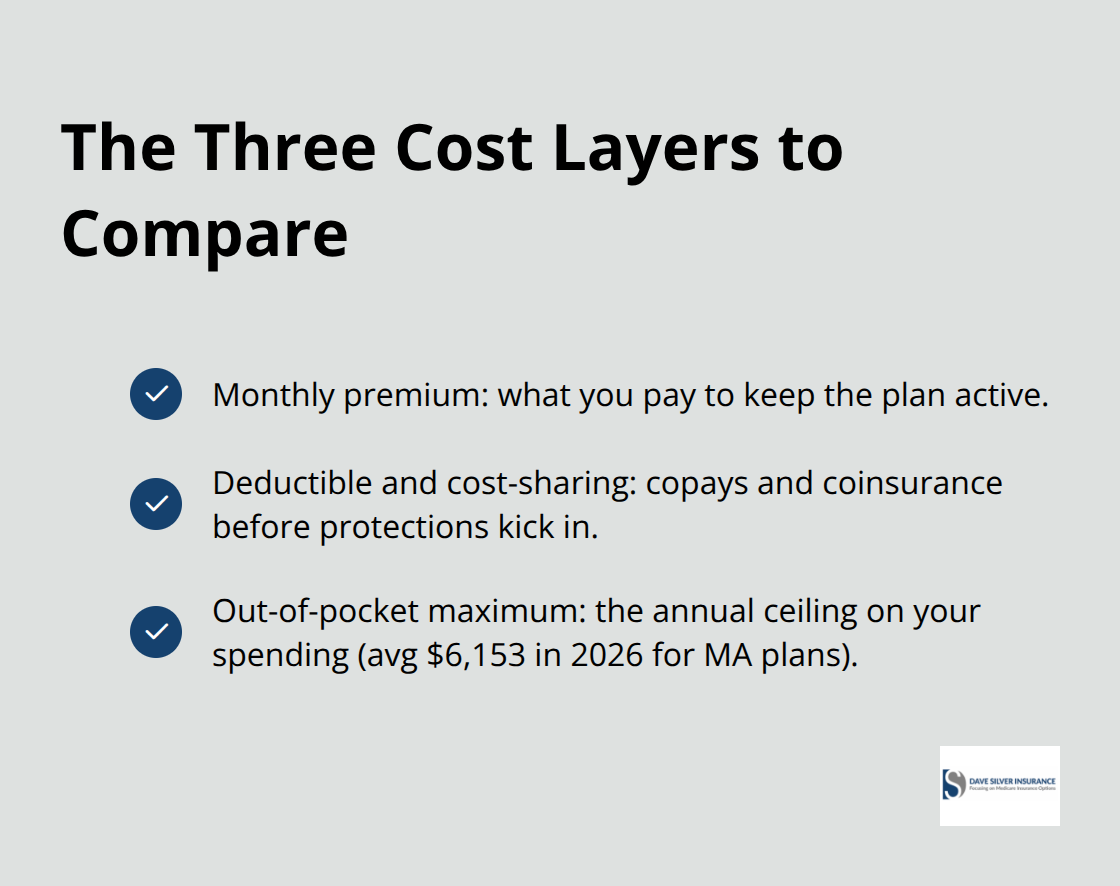

Comparing plans requires looking at three cost layers that most people ignore until they face a surprise bill. The first layer is your monthly premium-eHealth data shows this averaged just $4 across all 2026 Medicare Advantage plans, but this low number masks the real expense: what you pay when you actually use healthcare. The second layer is your deductible and cost-sharing, meaning copays and coinsurance that apply before your plan’s annual out-of-pocket maximum kicks in.

The third layer is that maximum itself, which jumped to an average of $6,153 for 2026 Medicare Advantage plans according to CMS, up from $5,749 the year before. A plan with zero premium but a $6,153 out-of-pocket limit could cost you far more than a plan with a $50 monthly premium and a $3,000 limit, depending on your actual healthcare use.

Calculate Total Annual Cost, Not Just the Premium

The only way to know which plan wins for your situation is to calculate total annual cost. Start by listing your expected doctor visits, medications, and any planned procedures. Then use Medicare Plan Finder to run actual numbers for two or three plans in your area, entering your specific drugs and dosages so the tool shows real costs, not estimates. A beneficiary comparing 2025 coverage to 2026 options saved an average of $1,676 annually by doing this homework, according to eHealth analysis.

Verify Your Doctors Stay In-Network

Your provider network directly determines whether your actual doctors stay affordable or become out-of-network surprises. Medicare Advantage plans, whether HMO or PPO, restrict which doctors you can see at standard costs; seeing an out-of-network provider triggers higher copays and coinsurance that count toward your out-of-pocket maximum. Before enrolling in any plan, verify that your current primary care doctor, specialists, and preferred hospitals are in-network, because switching doctors mid-year creates continuity gaps and delays in care.

Check Your Medications Against the Formulary

For prescription drugs, the formulary-the plan’s official list of covered medications-determines whether your medications are covered at all and at what cost tier. Some plans cover common drugs immediately with no deductible, while others make you wait until you’ve spent money out-of-pocket before coverage begins. The Part D donut hole, where coverage temporarily becomes thinner after $3,310 in covered drug spending, affects different people differently depending on their formulary. If your medications are high-tier drugs or not covered at preferred cost-sharing levels, you could spend significantly more during the gap phase. Using Medicare Plan Finder lets you compare drug coverage side-by-side for your exact prescriptions, showing the actual out-of-pocket costs you’ll face at each pharmacy for each plan.

Network Restrictions and Drug Coverage Shape Your Real Costs

These two factors-network access and drug formulary coverage-work together to determine your actual healthcare expenses. A plan that covers your medications at low cost but excludes your preferred cardiologist forces you to choose between switching doctors or paying out-of-network rates. Conversely, a plan with your doctor in-network but limited drug coverage could leave you paying full price for essential medications. The interaction between these two elements means you cannot evaluate either one in isolation. Your next step involves identifying which common mistakes trap Medicare shoppers into plans that don’t match their real needs.

Common Medicare Shopping Mistakes That Cost Thousands

Most Medicare shoppers fixate on the monthly premium and ignore everything else. A plan advertising zero dollars per month feels like a win until you face a $50 copay at every doctor visit, a $500 deductible before prescriptions are covered, or discover your specialist is out-of-network. The math becomes brutal quickly. An eHealth survey found that 48 percent of Medicare Advantage enrollees were completely unaware they had an annual window to change coverage, meaning thousands of people remain locked in the wrong plan year after year simply because they didn’t know Open Enrollment existed.

The Annual Enrollment Window Most People Miss

People treat Medicare shopping as a one-time event rather than an annual checkup. Plan networks change, drug formularies shift, and costs increase. A doctor who was in-network in 2025 might have left the network by 2026. A medication your plan covered last year could move to a higher tier or disappear entirely from the formulary. The average out-of-pocket maximum for Medicare Advantage plans jumped seven percent to $6,153 in 2026 from $5,749 the prior year, according to CMS data, yet most beneficiaries never recalculate whether their current plan still makes sense.

From January 1 to March 31 each year, you can switch plans or return to Original Medicare without penalty. Skipping this window locks you in for another twelve months. Treat Open Enrollment like a calendar event you cannot miss.

Overlooking Prescription Drug Tier Levels and Deductibles

Another widespread mistake involves underestimating prescription drug costs because people only glance at whether their drugs appear on the formulary, without checking the tier level or deductible structure. An eHealth survey revealed that 69 percent of Medicare beneficiaries want access to GLP-1 drugs for weight management in 2026, yet these medications often carry high out-of-pocket costs depending on the plan’s formulary tier and whether they fall within the Part D donut hole.

The Part D donut hole creates a coverage gap after you and your plan spend $3,310 on covered drugs. During this gap, you pay more until hitting catastrophic coverage around $4,850 in total spending. High-tier medications hit this gap harder than standard drugs, making the formulary tier level as important as whether your drug appears on the list at all.

Projecting Static Healthcare Needs Into a Changing Year

Equally damaging is assuming your healthcare needs will stay static. Someone with stable diabetes and two doctor visits annually makes very different plan calculations than someone facing knee surgery or starting a new expensive medication. Many shoppers project last year’s healthcare use onto the coming year without accounting for age-related changes, new diagnoses, or planned procedures.

Your health situation evolves, and your plan choices must evolve with it. A plan that worked perfectly last year may cost thousands more this year if your medical needs shift.

Skipping the Numbers and Relying on Impressions

The third major mistake involves never actually sitting down with the numbers. Using Medicare Plan Finder takes fifteen minutes and shows exact costs for your specific drugs and doctors in your area, yet most people rely on vague impressions or outdated information. Beneficiaries who actually compared their 2025 coverage to 2026 options saved an average of $1,676 annually, per eHealth analysis, proving that specific calculations beat assumptions every single time.

Enter your actual medications and dosages into Plan Finder. Verify that your current doctors appear in-network for the plans you’re considering. Calculate total annual cost (premium plus deductible plus expected copays) rather than focusing on the monthly premium alone. These concrete steps separate smart shoppers from those who pay thousands extra unnecessarily.

Your current plan almost certainly changed in ways that affect your costs, and your healthcare needs probably evolved since last year.

Final Thoughts

Smart Medicare plan comparison tips require three concrete actions that take minimal time but yield substantial savings. Visit Medicare Plan Finder on Medicare.gov and enter your specific medications, dosages, and current doctors for two or three plans in your area. Calculate your total annual cost across all three layers (premium, deductible, and out-of-pocket maximum) rather than fixating on the monthly premium alone, then cross-reference your preferred doctors against each plan’s network to confirm they stay in-network. Beneficiaries who ran these numbers saved an average of $1,676 annually compared to those who skipped this homework.

Your situation changes every year, your plan’s network shifts, and drug formularies evolve, which means you cannot treat Medicare shopping as a one-time decision. Open Enrollment runs from January 1 to March 31 each year, and treating this window as a mandatory annual event prevents you from overpaying for coverage that no longer matches your needs. A doctor who was in-network last year might have left the network by now, or a medication your plan covered could move to a higher tier or disappear entirely from the formulary.

If the process feels overwhelming or you want personalized guidance tailored to your health and financial situation, we at Dave Silver Insurance can help you navigate these decisions with clarity and confidence. Our team understands the nuances between plan types, knows how to match coverage to your actual healthcare needs, and walks you through the numbers so you understand exactly what you’re paying for. Contact Dave Silver Insurance to get personalized Medicare plan comparison guidance and eliminate the guesswork from your decision.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation