Medicare can feel overwhelming when you’re trying to figure out which parts you need and how they work together. At Dave Silver Insurance, we’ve helped thousands of people navigate Medicare Parts A, B, C, and D without confusion or costly mistakes.

This guide breaks down each part in plain language, shows you exactly what’s covered, and reveals how to cut your out-of-pocket costs. You’ll walk away knowing exactly which coverage options fit your situation.

Understanding Medicare Part A: Hospital Insurance

Medicare Part A is hospital insurance, and it covers inpatient hospital stays, skilled nursing facility care, hospice services, and some home health care. According to Medicare.gov, Part A is free for most people who worked and paid Medicare taxes for at least ten years. This forms the foundation of Original Medicare, and most people pay no monthly premium for it. If you didn’t work long enough to qualify for premium-free Part A, you can still enroll and pay a monthly premium ranging from $278 to $557 in 2026, depending on your work history. The critical distinction is that Part A covers only hospital-related services. It doesn’t cover doctor visits, outpatient care, or prescription drugs. Many people mistakenly assume Part A covers all hospital expenses, but that’s inaccurate. Part A covers the hospital facility itself, not the doctor’s fees inside the hospital. That’s where Part B comes in.

When Your Part A Coverage Starts

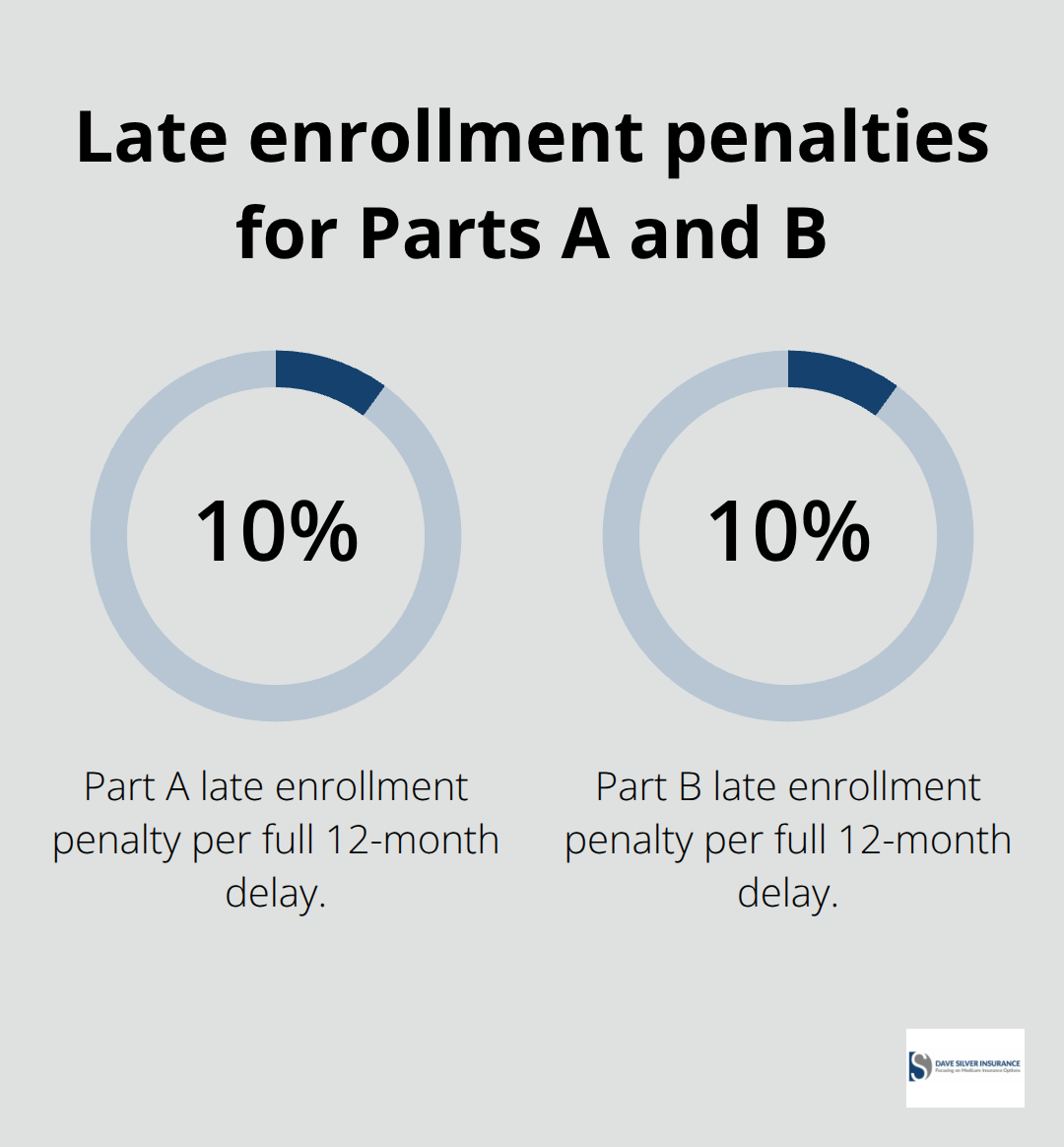

Enrollment timing determines when your coverage starts and whether you face penalties. According to Social Security Administration guidelines, your Initial Enrollment Period lasts seven months: three months before your 65th birthday, the month you turn 65, and three months after. If your birthday falls on the first of the month, premium-free Part A coverage starts the month before you turn 65. Otherwise, it starts the month you turn 65. If you miss this window and sign up later during the General Enrollment Period (January 1 through March 31 each year), your coverage doesn’t start immediately. Coverage begins the month after you enroll, which means you could face a gap in protection. The real problem surfaces if you delay enrollment without qualifying for a Special Enrollment Period. Medicare imposes a 10% lifetime penalty on your Part A premium for each full 12-month period you delayed enrollment after becoming eligible. That penalty sticks with you permanently, even if you eventually enroll.

Hospital Stay Costs You Must Know

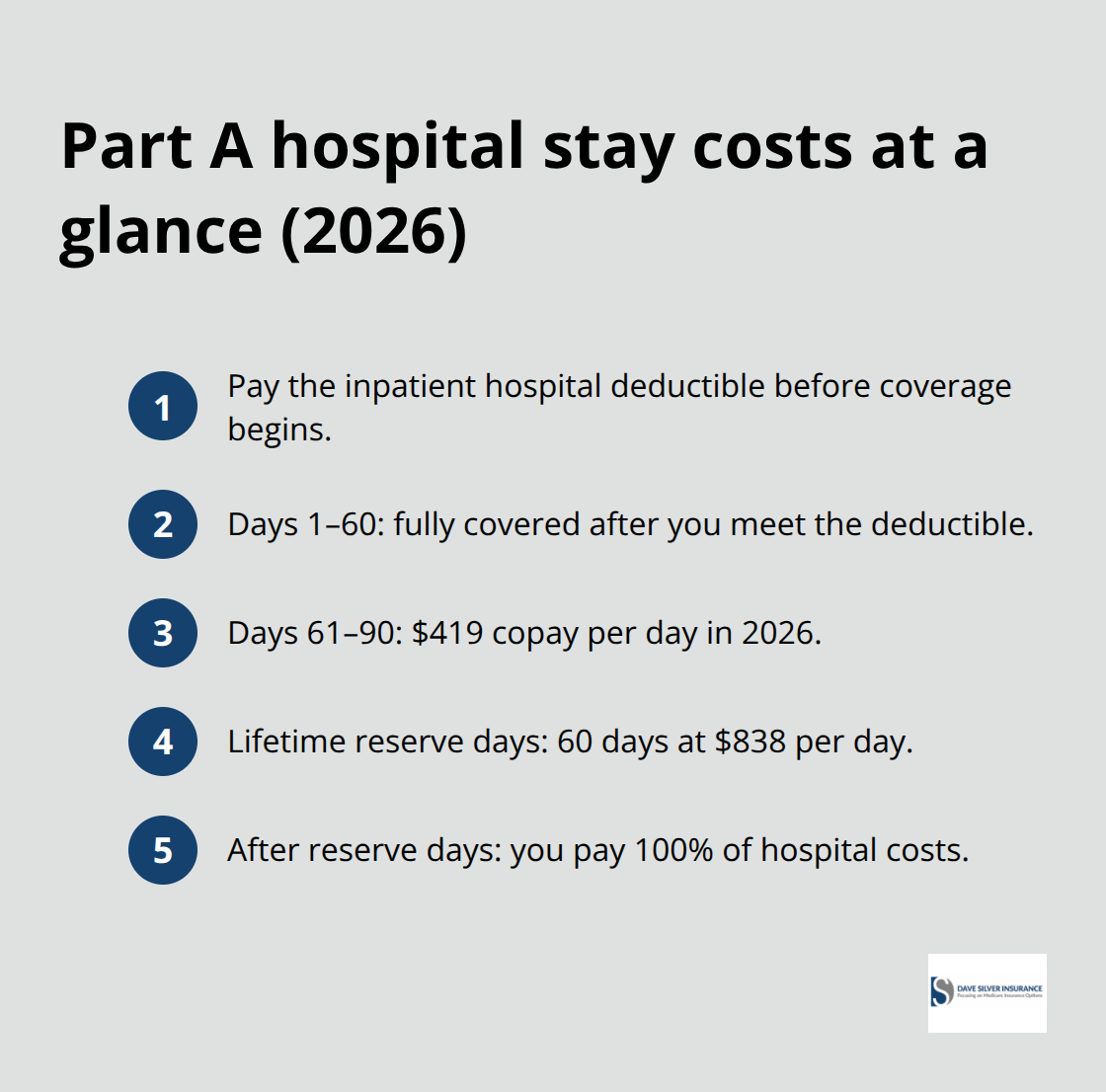

Most people focus on the monthly premium, but Part A carries significant out-of-pocket costs that actually matter more for your budget. In 2026, the Part A inpatient hospital deductible covers beneficiaries’ share of costs for the first 60 days of Medicare-covered inpatient hospital care. You pay this amount out of pocket before Part A starts covering anything for a hospital stay. If you’re hospitalized twice in the same benefit period, you only pay the deductible once. Days 1 through 60 of a hospital stay are fully covered after you meet the deductible. Days 61 through 90 require a daily copayment of $419 per day. If you need more than 90 days, costs escalate rapidly. You have 60 lifetime reserve days available, and using them costs $838 per day.

After those reserve days run out, you pay 100% of hospital costs.

Skilled Nursing and Extended Care Expenses

Skilled nursing facility care follows a different cost structure than hospital stays. You pay nothing for days 1 through 20, then $209.50 per day for days 21 through 100. Many people don’t realize these daily copayments exist because they assume Part A covers everything after the deductible. These costs add up quickly during extended stays, which is why supplemental coverage becomes valuable for reducing out-of-pocket expenses. Understanding these specific costs helps you plan for potential healthcare needs and identify gaps in your coverage. Part B coverage works alongside Part A to address some of these gaps, but it introduces its own set of costs and coverage rules that you need to understand.

Part B, C, and D: Understanding Your Coverage Options

Part B: Doctor Visits and Outpatient Services

Part B covers doctor visits, outpatient services, preventive care, and durable medical equipment-the services Part A explicitly doesn’t touch. According to Medicare.gov, Part B includes services from doctors and other healthcare providers, outpatient care, home health care, durable medical equipment, and most preventive services like screenings, shots, and yearly wellness visits. Unlike Part A, Part B requires a monthly premium that varies based on your income. In 2026, standard Part B premiums start at $185 per month for individuals earning up to $97,000 annually, but higher earners pay significantly more through Income-Related Monthly Adjustment Amounts.

Beyond the premium, you face a $240 annual deductible before Part B starts paying for most services. After meeting the deductible, you typically pay 20% coinsurance for doctor visits and outpatient services, meaning you split costs with Medicare. This structure matters because many people focus only on the monthly premium and ignore the deductible and coinsurance, which often exceed the annual premium cost. Preventive services like colonoscopies, mammograms, and flu shots are fully covered with no copay or coinsurance after you meet the Part B deductible, so scheduling these services during your coverage year makes financial sense.

Part B enrollment follows the same timeline as Part A, but the penalty structure differs. You face a 10% premium penalty for each full 12-month period you delay enrollment after becoming eligible, and this penalty sticks permanently.

Part C: Medicare Advantage as an Alternative

Medicare Advantage, also called Part C, represents an entirely different path from Original Medicare. Private insurance companies offer Part C plans that bundle Parts A, B, and usually Part D prescription drug coverage into one plan. According to Medicare.gov, you must enroll in Part A or Part B before enrolling in a Medicare Advantage plan. The appeal of Part C is simplicity and potential extra benefits-many plans include vision, hearing, and dental coverage that Original Medicare doesn’t provide.

However, Part C comes with significant trade-offs you need to understand before enrolling. Most Part C plans restrict you to a network of doctors and hospitals, meaning you cannot simply see any doctor who accepts Medicare like you can with Original Medicare. Out-of-network care typically costs substantially more or isn’t covered at all. Many Part C plans also charge additional premiums beyond what you pay for Part B, and some plans with lower premiums shift costs to you through higher deductibles and copayments.

The CMS Medicare.gov tool rates Medicare Advantage plans on a five-star scale reflecting overall performance and customer satisfaction, so checking star ratings for plans in your ZIP code provides objective comparison data rather than relying on marketing claims. The annual enrollment period runs October 16 through December 7, and missing this window locks you into your current plan or forces you to wait until the next year to make changes.

Part D: Prescription Drug Coverage

Part D prescription drug coverage operates separately from Parts A, B, and C. Private insurers offer Part D plans under Medicare rules, and you must have Part A or Part B to enroll in a standalone Part D plan. If you choose a Medicare Advantage plan with drug coverage included, you don’t need a separate Part D plan. The critical step with Part D involves reviewing the plan’s formulary-the list of covered medications-because formularies vary significantly between plans. Your current medications might carry a $5 copay under one plan and a $50 copay under another, making formulary review essential before enrollment.

The Part D coverage gap, sometimes called the donut hole, affects beneficiaries spending more than $5,850 on covered drugs in 2026. Once you hit that threshold, you pay a higher percentage of drug costs until you reach the catastrophic coverage level at $7,050 in out-of-pocket spending. Understanding whether your medications trigger this gap helps you anticipate yearly costs accurately. Extra Help, a federal program available through Medicare.gov, reduces or eliminates Part D premiums and cost-sharing for eligible low-income beneficiaries, yet many people who qualify don’t apply because they’re unaware the program exists.

These three parts (B, C, and D) work together or separately depending on which Medicare path you choose, and your decisions about each part directly impact your annual healthcare costs and access to providers. The next section explores how supplemental coverage fills the gaps that Original Medicare leaves behind.

How Medigap Fills the Gaps Original Medicare Leaves Behind

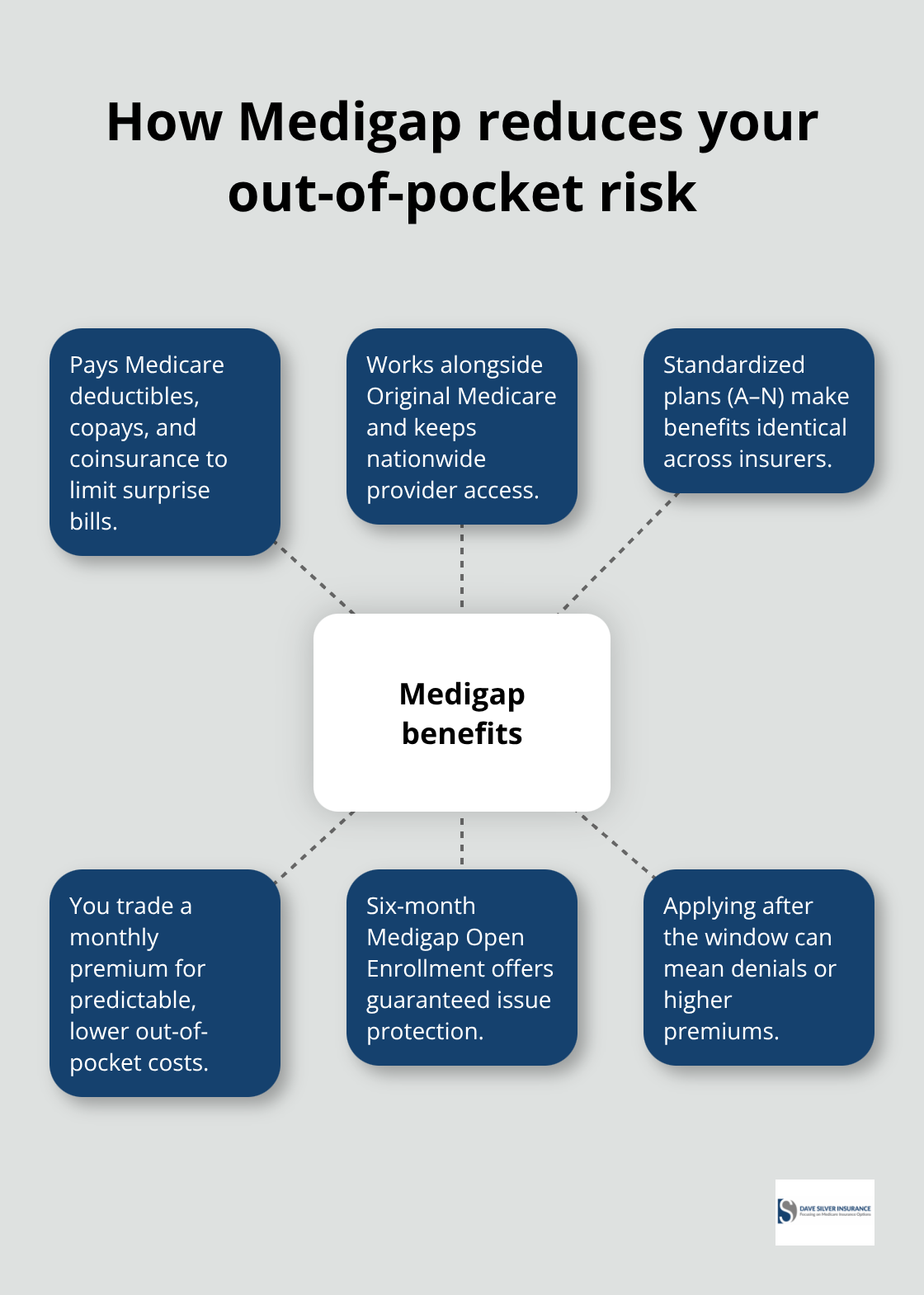

Original Medicare covers substantial services, but it leaves you responsible for significant out-of-pocket costs that most people underestimate. Part A requires you to pay a deductible before hospital coverage activates, then charges daily copayments for extended stays. Part B demands a $283 annual deductible and 20% coinsurance on most services after that threshold. These costs accumulate rapidly, especially for people with chronic conditions who need frequent doctor visits or those facing unexpected hospitalizations. Medigap insurance, also called Medicare Supplement Insurance, fills these gaps by paying the costs that Original Medicare doesn’t cover. Unlike Medicare Advantage plans that restrict your doctor choices, Medigap policies work alongside Original Medicare and preserve your nationwide provider access.

What Medigap Covers and How It Works

Medigap policies pay your deductibles, copayments, and coinsurance that Original Medicare leaves unpaid. The trade-off is straightforward: you pay a separate monthly premium to the Medigap insurer, but you eliminate the out-of-pocket expenses that would otherwise drain your bank account. For someone on a fixed income, this predictability matters tremendously because you know exactly what you’ll pay instead of facing surprise bills from healthcare providers. According to Medicare.gov, Medigap plans come in standardized packages named with letters like Plan G, Plan K, and Plan N. Each lettered plan offers identical benefits regardless of which insurance company sells it, so Plan G from one insurer covers the same services as Plan G from another. This standardization removes the guesswork from comparison shopping because you’re really just comparing premiums between insurers rather than deciphering different benefit structures.

Comparing Medigap Plans to Match Your Needs

Plan G represents the most comprehensive option for new enrollees, covering your Part A deductible, Part B deductible, Part B coinsurance, and excess charges that doctors sometimes bill above Medicare’s approved amounts. Plan K and Plan L offer less comprehensive coverage with higher out-of-pocket costs but lower premiums, making them attractive for healthier individuals who don’t anticipate frequent medical services. Plan N covers most costs but leaves you paying copayments for some doctor visits and emergency room visits, which appeals to people prioritizing lower premiums. Your actual healthcare patterns should drive your plan selection. Someone with multiple chronic conditions and frequent doctor visits benefits more from Plan G’s comprehensive coverage, while a relatively healthy person might save money overall with Plan N’s lower premium despite occasional copayments.

Enrollment Timing and Your Protection Window

Your enrollment window determines whether insurers can deny you coverage or charge higher premiums based on your health status. During the Medigap Open Enrollment Period, which runs for six months starting the first month you have Medicare Part B and you’re 65 or older, insurers cannot deny you coverage or charge higher premiums based on pre-existing conditions. If you miss this window and apply later, insurers can reject your application entirely or charge substantially higher premiums to compensate for your health status. This makes timing your Medigap enrollment critical because waiting even a few months past your enrollment window can cost you thousands in higher premiums or leave you uninsurable. The financial impact of missing this deadline cannot be overstated-a delay past your enrollment period could result in permanent premium increases that persist for the rest of your life.

Taking Action on Your Medigap Decision

Selecting the right Medigap plan requires honest assessment of your healthcare needs and budget constraints. Start by reviewing your current medical conditions, medications, and how frequently you visit doctors or specialists. Compare the premiums for different plans in your area, then calculate which plan actually costs less when you factor in both premiums and expected out-of-pocket expenses. If you have significant healthcare needs, the higher premium for Plan G often costs less overall than the lower premium of Plan N when you account for copayments and coinsurance. Contact multiple Medigap insurers directly to request quotes for the specific plan you’re considering, since premiums vary substantially between companies even for identical coverage.

Final Thoughts

You now understand how Medicare Parts A, B, C, and D work together to form your coverage foundation. Part A covers hospital care, Part B covers doctor visits and outpatient services, Part C offers an alternative bundled approach through Medicare Advantage, and Part D handles prescription drugs. Medigap fills the gaps that Original Medicare leaves behind, reducing your out-of-pocket costs significantly, while enrollment windows matter tremendously because missing them triggers permanent penalties and limits your coverage options.

The real challenge isn’t understanding these parts in isolation-it’s figuring out which combination actually works best for your specific situation. Someone with multiple chronic conditions and preferred doctors faces entirely different considerations than a relatively healthy person willing to accept network restrictions for lower premiums. Your medications, anticipated healthcare needs, and financial constraints all factor into the right decision for how to navigate Medicare Parts effectively.

We at Dave Silver Insurance help people navigate Medicare Parts and avoid costly mistakes through personalized guidance based on your actual health and financial situation. Contact Dave Silver Insurance to review your specific circumstances and receive tailored recommendations that fit your needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation